Unclassified balance sheet definition

/What is an Unclassified Balance Sheet?

An unclassified balance sheet does not provide any sub-classifications of assets, liabilities, or equity. Instead, this reporting format simply lists all normal line items found in a balance sheet in their order of liquidity, and then presents totals for all assets, liabilities, and equity. This approach does not include subtotals for any of the following classifications:

A balance sheet that includes these subtotals is called a classified balance sheet, and is the most common form of presentation. This presentation is needed in order to derive liquidity ratios, such as the current ratio, that depend on the presentation of current asset and current liability subtotals.

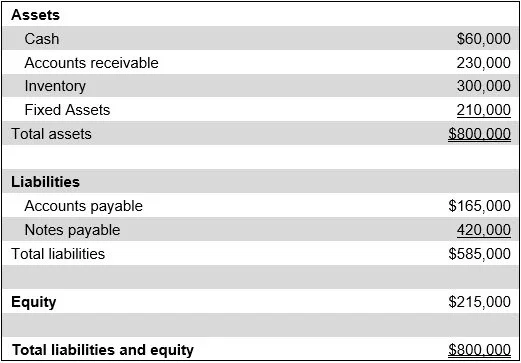

Example of an Unclassified Balance Sheet

The following exhibit contains an example of an unclassified balance sheet, where no subtotals are listed.

When to Use an Unclassified Balance Sheet

An unclassified balance sheet can be appropriate when there are few line items to report, as may be the case for a shell company or a small business that has very few assets or liabilities. It may also be used for internal reporting purposes, where managers have less need for subtotals. If this approach is used, assets are presented in order of liquidity, so that cash is presented first and fixed assets are presented last. Similarly, liabilities are presented in order of when they are due, so that accounts payable are listed first and long-term debt is listed last.

Classified vs. Unclassified Balance Sheets

The key differences between classified and unclassified balance sheets are as follows:

Organization of information. A classified balance sheet separates assets and liabilities into current and non-current categories, while an unclassified balance sheet presents assets, liabilities, and equity in a single list without classification.

Detail level. A classified balance sheet provides more detailed insights into liquidity and solvency by breaking items into subcategories, while an unclassified balance sheet offers a summarized view without detailed categorization.

Usefulness to users. A classified balance sheet. is more useful for external stakeholders (e.g., investors, creditors) due to its clarity, while an unclassified balance sheet is less informative and typically used for internal or simplified reporting.

Compliance with accounting standards. A classified balance sheet is required or preferred under GAAP and IFRS for external reporting, while an unclassified balance sheet is generally not compliant with formal financial reporting standards for public companies.

Liquidity assessments. A classified balance sheet facilitates easy analysis of a company’s liquidity through current vs. non-current distinctions, while an unclassified balance sheet makes liquidity assessment more difficult due to lack of segmentation.

Common usage. A classified balance sheet is the standard format for audited financial statements, while an unclassified balance sheet is more commonly found in interim, internal, or simplified reports.