Accounts Payable Explained

/What is Accounts Payable?

Accounts payable is the aggregate amount of one's short-term obligations to pay suppliers for products and services that were purchased on credit. If accounts payable are not paid within the payment terms agreed to with the supplier, the payables are considered to be in default, which may trigger a penalty or interest payment, or the revocation or curtailment of additional credit from the supplier. The term can also refer to the department that processes payables.

Accounts payable are considered a source of cash, since they represent funds being borrowed from suppliers. When accounts payable are paid, this is a use of cash. Given these cash flow considerations, suppliers have a natural inclination to push for shorter payment terms, while creditors want to lengthen the payment terms. When a business is short on cash, management frequently mandates that the payment of accounts payable be delayed, since this represents a no-interest loan from suppliers.

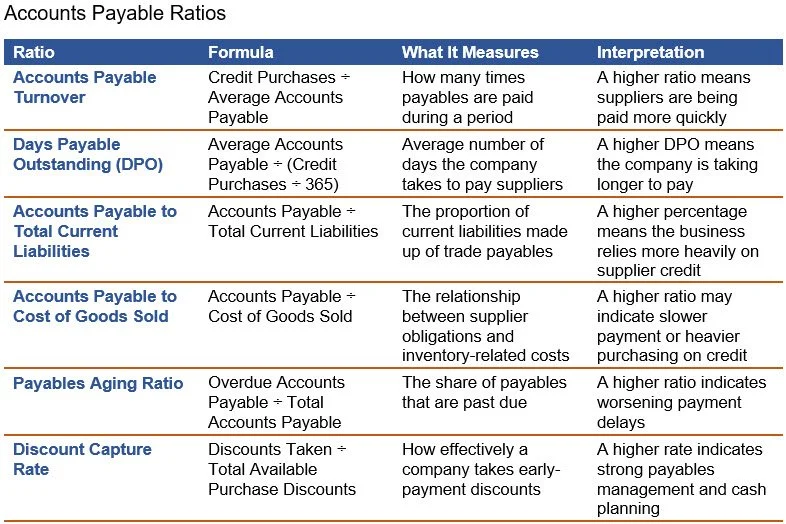

Accounts Payable Ratios

There are several key ratios that can be used to monitor the performance of the accounts payable function. Either the accounts payable turnover or days payable outstanding ratios can be used to determine how long the department is taking to pay suppliers. Either the accounts payable to total current liabilities or the accounts payable to cost of goods sold metrics can be used to measure the relative proportion of payables on the balance sheet. To review departmental performance at a more granular level, the payables aging ratio and the discount capture rate can be used to determine whether invoices are being paid on time, and discounts are being taken, respectively. These ratios are described in the following exhibit.

Accounting for Accounts Payable

The normal accounting for accounts payable is to debit either the expense or asset account associated with a purchase, and credit the accounts payable account (which is a liability account). When the liability is paid, the entry is a debit to the accounts payable account (thereby eliminating the liability) and a credit to the cash account (reducing the balance in that account). This accounting is used in a double-entry bookkeeping system. For example, if a business were to incur a liability for $100 of supplies expense, the initial entry would be as follows:

The payables department later pays the supplier the full amount of the invoice, and records the following entry for the transaction:

If the supplier offers a discount in exchange for the early payment of the invoice, the company is not paying the full amount of the invoice. Instead, that portion of the invoice related to the discount is charged to a separate account. An example of an entry to take a 2% early payment discount is as follows:

When individual accounts payable are recorded, this may be done in a payables subledger, thereby keeping a large number of individual transactions from cluttering up the general ledger. Alternatively, if there are few payables, they may be recorded directly in the general ledger.

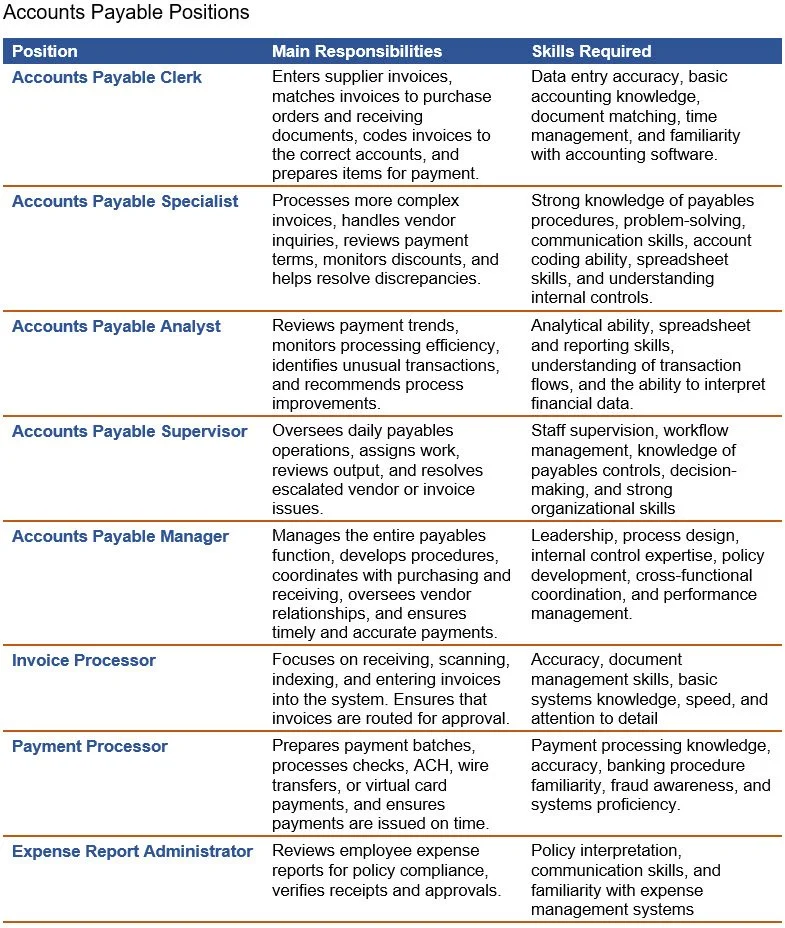

Accounts Payable Positions

There may be just one accounts payable clerk position in a small business. However, as the payables volume rises in a larger business, the department’s staffing requirements can expand substantially. There will likely be senior payables clerk positions, known as accounts payable specialists, as well as analysts to review the process flow, and a supervisor to oversee the entire operation. There may also be specialists who deal with payments to suppliers, as well as specialists to deal solely with incoming employee expense reports. The level of specialization increases with the size of the department. These positions, their main responsibilities, and the skills required for each one are summarized in the following exhibit.

Examples of Accounts Payable

An account payable is generated whenever a supplier renders services or delivers goods for which payment is not immediately made in cash. Some of the more common examples of accounts payable are as follows:

Trade inventory payable. A retailer buys merchandise from a wholesaler on 30-day credit terms. Once the goods are received, the unpaid invoice becomes an account payable until the retailer remits payment. This is one of the most common forms of accounts payable, because it arises directly from normal operating purchases.

Office supplies payable. A company orders paper, toner, folders, and other office materials from a vendor and receives an invoice due in 15 days. The unpaid amount is recorded as an account payable. Even though the items are relatively low cost, they still create a formal short-term liability.

Utility services payable. A business receives monthly electricity, water, or internet service and is billed after the service period ends. Until the bill is paid, the amount due is classified as an account payable. This type of payable reflects routine operating support rather than the purchase of physical goods.

Professional fees payable. A law firm, accounting firm, or IT consultant may complete work for a company and issue an invoice payable within a stated period. The unpaid invoice is recorded as an account payable. These obligations arise from outside services received and are usually cleared within the normal payment cycle.

Equipment repair payable. A maintenance vendor repairs a company’s production equipment and submits an invoice for labor and replacement parts. If the invoice remains unpaid at period-end, it is recorded as an account payable. This payable is tied to preserving operating capacity rather than acquiring new assets.

These examples show that accounts payable can arise from many routine business activities, including inventory purchases, services, utilities, supplies, and repairs.

Accounts Payable Procedure

From a management perspective, it is of some importance to have accurate accounts payable records, so that suppliers are paid on time and liabilities are recorded in full and within the correct time periods. Otherwise, suppliers will be less inclined to grant credit, and the financial results of a business may be incorrect. This means that accounts payable must be processed exactly in accordance with a strict procedure that is followed in exactly the same way, every time. This procedure includes the activities noted below.

Step 1. Receive the Supplier Billing

All supplier invoices are immediately routed to the payables department as soon as they are received. This can be a difficult processing step, since invoices might have been sent to the person authorizing a purchase, or perhaps to a subsidiary. In either case, there must be a firm requirement for the recipient to immediately forward the invoice to the payables department. A particular concern is when invoices are sent to people who no longer work for the company - perhaps by email; if so, it may take repeated inquiries from the supplier before the invoice is found.

Step 2. Review Billing Details

Each received invoice should be examined to verify whether the company actually owes the indicated amount, as well as to determine whether it contains the correct unit quantities, unit prices, and payment date. If not, the payables department must contact the supplier to request that a corrected invoice be sent. The department may also compare the invoice to the authorizing purchase order to ensure that the delivery was authorized, and compare it to receiving documentation to ensure that the billed amounts were actually received. Also, depending on the company’s approval threshold, it may be necessary to obtain a supervisor’s approval before an invoice can be paid.

Step 3. Update Accounting Records

Once the preceding step has been completed, the invoice is recorded in the company’s accounting system, using the invoice date as the entry date. The payment date is based on the invoice date. For example, if an invoice has a date of September 1 and should be paid in 30 days, then it is logged in as of September 1, so that the accounting system will pay it on September 30.

Step 4. Pay Suppliers

On each scheduled payment date, the accountant runs a preliminary check register and reviews it to ensure that all stated payments should be made. If not, they are flagged to be paid at a later date. The remaining payments are made, using either checks or electronic payments. Depending on the controls used, these payments may need to be approved before they are issued.

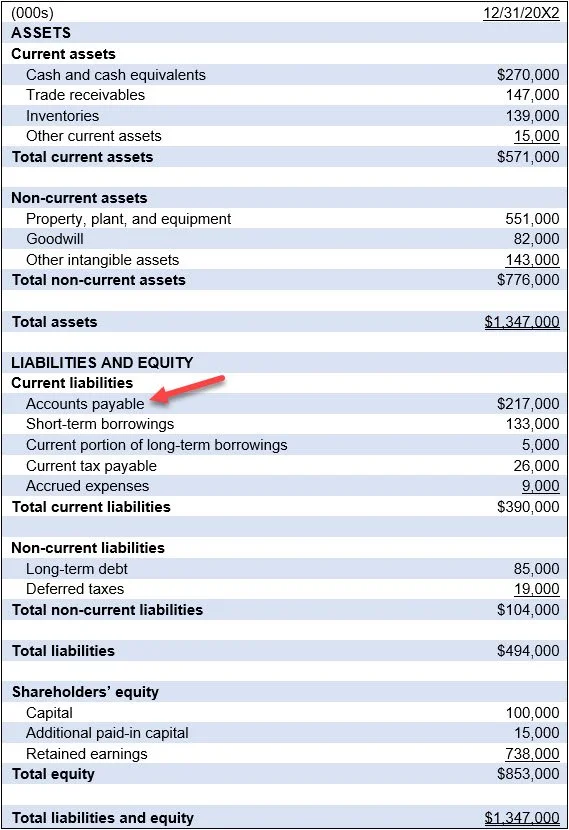

Presentation of Accounts Payable

Accounts payable are nearly always classified as current liabilities. This is because they are generally due for payment within a short period of time, such as 30 days from the invoice date. Consequently, accounts payable normally appears near the top of the liabilities section of the balance sheet, typically as the first line item presented. In those rare cases in which an account payable is not due for payment for more than a year, it is instead classified as a long-term liability, and so is presented lower in the balance sheet, between the current liabilities section and the equity section. A sample presentation of accounts payable appears in the following exhibit, which contains a balance sheet.

Accounts Payable FAQs

What is the difference between trade payables and non-trade payables?

Trade payables arise from purchases of goods and services tied to normal operations, such as inventory or supplies bought on credit. Non-trade payables are other short-term obligations, such as taxes payable, wages payable, interest payable, or dividends payable. The distinction helps classify liabilities and analyze operating versus non-operating obligations.

How are purchase discounts handled in accounts payable?

Purchase discounts are handled by paying supplier invoices within the discount period and recording the reduction in the amount owed. Under the gross method, the discount is recognized only if taken. Under the net method, the liability is recorded net of the discount, with missed discounts recognized separately as financing cost.

How can duplicate payments occur in accounts payable?

Duplicate payments can occur when the same invoice is entered more than once, when both an original and a copy are processed, or when vendor names or invoice numbers are recorded inconsistently. Weak approval controls, manual processing errors, and poor system validation increase the risk of paying the same obligation twice.

Related Articles

Accounting for Accounts Payable

How to Reconcile Accounts Payable