Petty cash book definition

/What is the Petty Cash Book?

The petty cash book is a recordation of petty cash expenditures, sorted by date. In most cases, the petty cash book is an actual ledger book, rather than a computer record. Thus, the book is part of a manual record-keeping system. The petty cash book has declined in importance, as companies are gradually eliminating all use of petty cash, in favor of using company credit cards.

Accounting for Petty Cash

There are two primary types of entries in the petty cash book, which are a debit to record cash received by the petty cash clerk (usually in a single block of cash at infrequent intervals), and a large number of credits to reflect cash withdrawals from the petty cash fund. These credits can be for such transactions as payments for meals, flowers, office supplies, stamps, and so forth. A sample journal entry format for the recordation of a variety of petty cash fund withdrawals appears next.

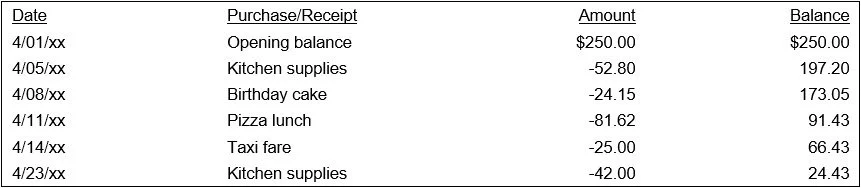

A somewhat more useful format is to record all debits and credits in a single column, with a running cash balance in the column furthest to the right, as shown in the following example. This format is an excellent way to monitor the current amount of petty cash remaining on hand.

Sample Petty Cash Book (Running Balance)

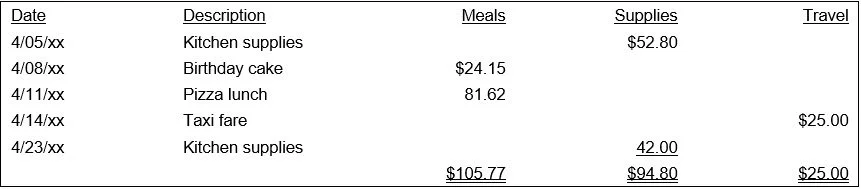

Yet another variation on the petty cash book is to maintain it as a spreadsheet, where each item is recorded in a specific column that is designated for a particular type of receipt or expense. This format makes it easier to record petty cash activity in the general ledger. An example of this format, using the same information as the preceding example, is as follows:

Sample Petty Cash Book (Columnar)

When the amount of petty cash on hand declines to near zero, as is caused by withdrawals for various expenditures, the petty cash clerk then obtains additional cash from the cashier, and records this cash influx as a new debit. The petty cash clerk also turns in a copy of his or her petty cash book to the general ledger accountant or cashier, who creates a journal entry to record how the cash in the petty cash drawer was used.

Advantages of a Petty Cash Book

The petty cash book is a useful control over petty cash expenditures, since it forces the petty cash clerk to formally record all cash inflows and cash outflows. To ensure that this is an effective control, the petty cash book should be reviewed periodically by an internal auditor to see if the net total amount of cash available as per the book matches the actual amount of cash on hand in the petty cash drawer. If not, the petty cash clerk may require additional training.

FAQs

How long should petty cash books be retained?

Petty cash books should be retained in accordance with the organization’s formal document retention policy. In practice, this period often aligns with the retention requirements for other accounting records, commonly several years. Retention supports audit, regulatory, and internal review needs.