Nonprofit Accounting Explained

/Nonprofit organizations are integral to cultural, educational, religious, humanitarian, and other mission-based efforts within society. Unlike for-profit businesses that generate revenue to provide returns to owners or shareholders, nonprofits depend primarily on donations, grants, and similar support to finance their activities. They have no equity holders and cannot distribute profits; any surplus is retained and used to advance their mission. Due to heightened accountability and disclosure expectations, nonprofits apply a specialized reporting framework called fund accounting to track revenues and expenses. Mastery of these principles helps leaders allocate resources wisely, refine fundraising strategies, evaluate programs, and sustain long-term mission effectiveness.

What is Nonprofit Accounting?

Nonprofit accounting is a specialized discipline designed for charitable and mission-driven entities whose objective is stewardship rather than profit generation. Unlike a retail business that records sales revenue without regard to donor intent, a nonprofit must classify incoming resources according to externally imposed restrictions and report on their use with heightened transparency to donors and boards.

Consider two contrasting scenarios. A community foundation awards a $50,000 grant to expand a literacy program. Because the grant agreement specifies instructional materials and tutor stipends, those resources are restricted and must be tracked separately. By contrast, a long-time supporter contributes $5,000 with no stated purpose. Those funds are unrestricted and may be applied to rent, utilities, or administrative support. Fund accounting requires distinct tracking mechanisms so that restricted funds are not commingled with general operating resources.

In the United States, nonprofit reporting follows Financial Accounting Standards Board guidance under GAAP, ensuring consistent, decision-useful financial statements for stakeholders.

Related AccountingTools Courses

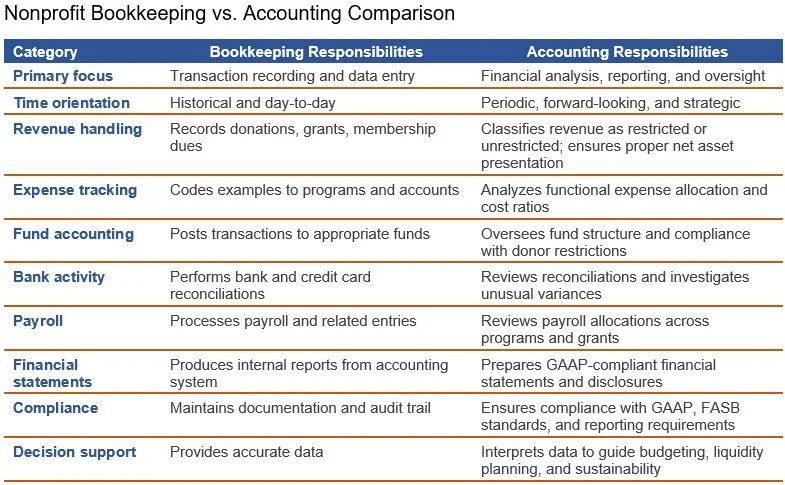

Comparing Bookkeeping and Accounting in a Nonprofit

Confusion frequently arises within nonprofits regarding the distinction between bookkeeping and accounting. Board members and executive directors may assume the terms are interchangeable, particularly in smaller organizations where one individual performs both functions. This misunderstanding can lead to unrealistic expectations, weak internal controls, and gaps in financial oversight. Bookkeeping is transactional and compliance-oriented, while accounting is analytical and strategic. In a mission-driven environment governed by fund accounting, the distinction becomes even more important because resources may be restricted, reporting obligations are heightened, and financial statements must comply with GAAP. The key determining factors are as follows:

Bookkeeping in a nonprofit. Bookkeeping focuses on recording daily financial transactions, including donations, grant receipts, payroll, vendor payments, and bank reconciliations. It ensures that restricted and unrestricted funds are coded properly, accounts are balanced, and documentation is retained. The emphasis is on accuracy, timeliness, and compliance with internal procedures.

Accounting in a nonprofit. Accounting involves interpreting financial data, preparing GAAP-compliant financial statements, managing fund classifications, analyzing program costs, supporting audits, and advising leadership on budgeting, liquidity, and financial sustainability. It translates transactional data into actionable insight.

There is a clear role separation between bookkeeping and accounting. When nonprofits understand the difference, they enhance both compliance and strategic stewardship. The key differences are noted in the following table.

Nonprofit Chart of Accounts

A nonprofit’s chart of accounts, when structured using the Unified Chart of Accounts (UCOA), is designed to support fund accounting, donor transparency, functional expense reporting, and Form 990 alignment. The UCOA framework standardizes account groupings so that internal financial statements, grant reports, and external filings can be generated consistently. The structure typically incorporates both natural classifications, such as salaries or rent, and functional classifications, such as program, management and general, and fundraising. This dual coding facilitates preparation of the statement of activities and statement of functional expenses. The primary categories include the following:

Assets. Includes cash and cash equivalents, receivables, prepaid expenses, investments, and property and equipment. Assets may be tracked by fund or restriction category.

Liabilities. Includes accounts payable, accrued expenses, deferred revenue, refundable advances, and debt obligations.

Net assets. Total assets minus total liabilities, stated with donor restrictions and without donor restrictions.

Revenue and support. Includes contributions, grants, program service revenue, membership dues, special events, and investment income.

Expenses. Includes program services, management and general, and fundraising, further detailed by natural expense classifications.

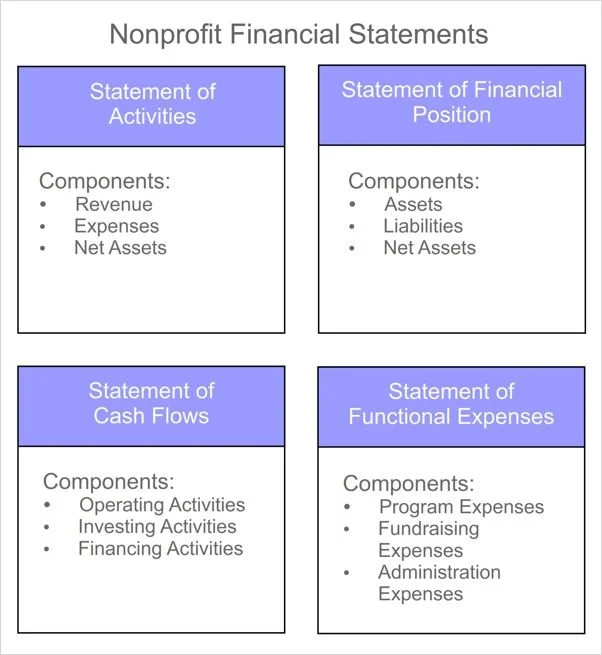

Nonprofit Financial Statements

Nonprofit entities present four core financial statements under U.S. GAAP. While they parallel the statements issued by for-profit organizations, the terminology and presentation reflect the absence of ownership interests and the presence of donor-imposed restrictions. The objective is to communicate liquidity, operating performance, and stewardship over restricted and unrestricted resources. The statements are as follows:

Statement of financial position. This statement is the nonprofit equivalent of a balance sheet. It reports assets, liabilities, and net assets as of a specific date. Net assets are classified into two categories: net assets without donor restrictions and net assets with donor restrictions. The statement highlights liquidity, the composition of investments and receivables, and the extent of donor-imposed limitations on resources. It enables users to assess solvency and financial flexibility.

Statement of activities. This statement replaces the traditional income statement. It reports revenues, support, expenses, gains, and losses for the reporting period, along with changes in net asset classifications. Revenues are presented by restriction category, and expenses are typically shown by functional classification such as program services and supporting services. The statement explains how the organization’s net assets increased or decreased during the period.

Statement of cash flows. This statement reports cash inflows and outflows classified as operating, investing, and financing activities. It provides insight into cash liquidity, capital expenditures, and financing activities such as donor-restricted contributions for long-term purposes.

Statement of functional expenses. Required for voluntary health and welfare organizations and commonly presented by other nonprofits, this statement disaggregates expenses by both natural classification, such as salaries, rent, and supplies, and functional classification, such as program, management and general, and fundraising. It enhances transparency by showing how resources are allocated between mission-related activities and administrative support.

The contents of these statements are summarized in the following graphic:

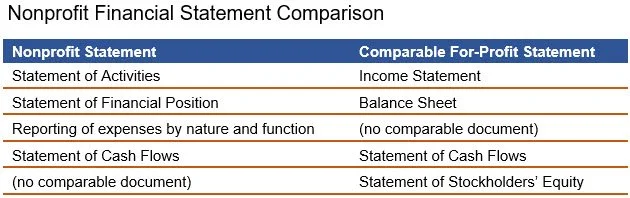

Together, these four statements provide a comprehensive view of financial condition, operating performance, cash management, and stewardship of donor resources. The following exhibit compares the financial statements generated by a nonprofit and for-profit entity.

Nonprofit Tax Forms

Although most nonprofit organizations are exempt from federal income tax under Internal Revenue Code Section 501(c), they remain subject to a range of federal and state filing requirements. Tax compliance is therefore procedural rather than profit-based. The exact forms required depend on the organization’s size, activities, payroll structure, and revenue sources. Any failure to file required forms can result in penalties or the automatic revocation of tax-exempt status. The primary federal filings include the following:

Form 990. The annual information return for tax-exempt organizations. Larger nonprofits file Form 990; smaller organizations may file Form 990-EZ, while very small organizations file Form 990-N (e-Postcard). It reports governance, compensation, program accomplishments, and financial data.

Form 990-T. Filed when a nonprofit earns unrelated business taxable income. Income from activities not substantially related to the exempt purpose may be subject to corporate income tax.

Form 1023. The application used to obtain recognition of exemption under Section 501(c)(3). Smaller organizations may use Form 1023-EZ.

Form 941. Filed quarterly to report payroll taxes withheld and employer payroll tax liabilities.

Form W-2 and Form 1099-NEC. Used to report compensation paid to employees and independent contractors.

Form 990-PF. Required for private foundations, with additional reporting on minimum distribution requirements and excise taxes.

In addition, state filings may include charitable solicitation registrations, state income or franchise tax returns, and sales tax exemption documentation.

Nonprofit Accounting Best Practices

Thus far, we have discussed how nonprofit accounting information is compiled and presented. In addition, you should be familiar with several best practices that can make the difference between a successful nonprofit and a failed one. Each of these recommendations falls within the range of responsibility of the nonprofit accountant.

Categorize Revenue Sources

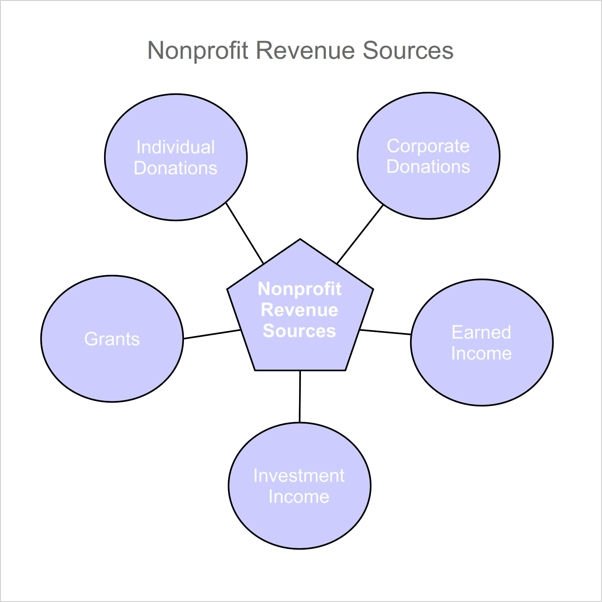

Every nonprofit should diversify its revenue sources. Otherwise, it is at risk of failure if one or two main sources of funds dry up. To make this abundantly clear to management, list in the statement of activities each revenue source. Better yet, list each one on a trend line in a separate report, so that managers can see if the organization is succeeding in diversifying its revenue sources. The main nonprofit revenue sources are noted in the following exhibit.

The components of these revenue sources are as follows:

Individual donations. Contributions from private individuals, which may be unrestricted or donor-restricted, and are typically recognized as contribution revenue when received or unconditionally pledged.

Corporate donations. Voluntary transfers of cash or other assets from businesses, often tied to sponsorships, matching gift programs, or community initiatives, and accounted for as contributions if no commensurate value is exchanged.

Grants. Funding awarded by government agencies, foundations, or other entities, usually subject to specific eligibility requirements or performance conditions that determine the timing of revenue recognition.

Earned income. Revenue generated from providing goods or services related to the nonprofit’s mission, such as program fees, tuition, ticket sales, or membership dues, recognized when the performance obligation is satisfied.

Investment income. Returns generated from the nonprofit’s invested assets, including interest, dividends, and realized or unrealized gains, reported in accordance with donor restrictions and endowment classifications.

Delve into Overhead Costs

In the nonprofit environment, the word “overhead” has long carried an unfavorable implication, as though dollars devoted to administration or fundraising are dollars diverted from mission delivery. That perception is overly simplistic. A certain level of infrastructure spending is essential if an organization expects to function effectively, maintain compliance, and expand its reach over time. Overhead encompasses administrative and fundraising expenses. These costs include executive and support staff compensation, occupancy and utility charges, technology systems, marketing efforts, and donor management platforms. Although these expenditures do not represent direct program services, they create the operational foundation that allows programs to exist and scale. Nonprofits should manage overhead prudently and evaluate reductions before impairing program delivery. This means that the accountant should understand exactly how all significant overhead expenditures support the mission of the organization. Doing so makes it easier to either cut back on non-supportive expenditures, or justify the existence of overhead to donors.

Create and Follow a Budget

A nonprofit budget is a formal financial plan that translates mission objectives into projected revenues and expenditures for a fiscal period. Unlike a purely profit-driven entity, a nonprofit’s budget must align resource allocation with programmatic outcomes, donor restrictions, grant compliance requirements, and liquidity constraints. It is typically prepared on an accrual basis and may incorporate fund-level detail to ensure that restricted and unrestricted resources are properly planned and monitored. The budget functions as both a planning instrument and a control mechanism, guiding management decisions throughout the year. The key reasons a nonprofit uses a budget include the following:

Mission alignment. Ensures that financial resources are directed toward approved programs and strategic priorities.

Financial control. Establishes spending limits and supports variance analysis.

Grant and donor compliance. Demonstrates the responsible stewardship of restricted funds.

Cash flow management. Highlights timing differences between receipts and expenditures.

Board oversight. Provides a framework for governance review and performance monitoring.

Implement Controls

Internal controls are essential in a nonprofit to safeguard assets, ensure reliable financial reporting, promote regulatory compliance, and protect the organization’s reputation with donors, grantors, and oversight bodies. Because nonprofits often rely on contributions and restricted funding, strong controls help ensure that resources are used in accordance with donor intent and board-approved budgets. Effective controls also reduce the risk of fraud and mismanagement, particularly in environments with limited staff. Common controls include the following:

Segregation of duties between authorization, custody, and recordkeeping functions.

Board approval of budgets and periodic review of financial statements.

Dual signatures or approval thresholds for disbursements.

Independent bank reconciliations performed monthly.

Restricted access to accounting systems and donor databases.

Audit the Financial Statements

An annual financial statement audit provides independent assurance that a nonprofit’s financial statements are fairly presented in accordance with the applicable reporting framework, which is typically U.S. GAAP. This external validation enhances credibility with donors, grantors, lenders, and regulators, many of whom require audited statements as a condition of funding. An audit also strengthens governance by giving the board of directors objective insight into the organization’s financial condition, internal controls, and compliance with donor restrictions. Beyond compliance, the audit process can identify control deficiencies, accounting errors, or operational risks that management may not detect internally. Addressing these findings improves financial reporting quality and reduces the risk of fraud.

Nonprofit Accounting FAQs

How does nonprofit accounting differ from for-profit accounting?

Nonprofit accounting differs from for-profit accounting in that its primary objective is stewardship and mission fulfillment rather than profit maximization, so financial reporting emphasizes accountability to donors, grantors, and regulators. Nonprofits use fund accounting and classify net assets as with or without donor restrictions, whereas for-profit entities focus on equity accounts and retained earnings. In addition, nonprofits report expenses by both natural and functional classifications and prepare a statement of activities instead of an income statement that is centered on net income.

What kind of accounting do nonprofits use?

Nonprofits use fund accounting, which is a system designed to track resources by purpose and restriction rather than by profit center. They typically maintain their books on the accrual basis of accounting in accordance with U.S. GAAP, particularly FASB guidance applicable to not-for-profit entities. This structure allows them to segregate net assets with and without donor restrictions while producing financial statements such as the statement of financial position and statement of activities.

How does a nonprofit set up a fund accounting system?

A nonprofit sets up a fund accounting system by first identifying the types of funds required, such as unrestricted operating funds, temporarily restricted program funds, and permanently restricted endowments, based on donor intent and board designations. It then designs a chart of accounts that assigns unique fund codes to revenues, expenses, assets, and liabilities so that transactions can be segregated and reported by restriction and program. Finally, it configures its accounting software to track both natural and functional expense classifications, ensuring compliance with GAAP reporting and facilitating the preparation of the statement of activities and related disclosures.