Construction Accounting Explained

/What is Construction Accounting?

Construction accounting is a form of project accounting in which costs are assigned to specific contracts. A separate job is set up in the accounting system for each construction project, and costs are assigned to the project by coding costs to the unique job number as the costs are incurred. These costs are primarily comprised of materials and labor, with additional charges for such items as consulting and architectural fees. A number of indirect costs are also charged to construction projects, including the costs of supervision, equipment rentals, support costs, and insurance. Administrative costs are not charged to a construction project unless this is allowed by the customer.

Construction Accounting vs. Regular Accounting: The Key Differences

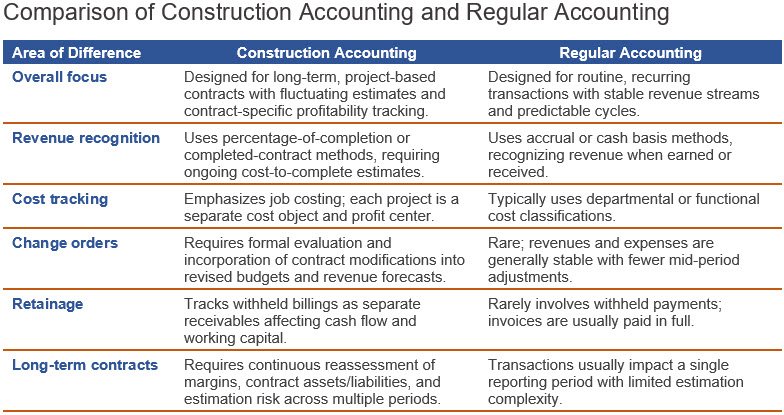

Construction accounting departs significantly from traditional accounting because it is structured around long-term, project-based work rather than routine, recurring transactions. While regular accounting emphasizes stable revenue streams, departmental expense classifications, and relatively predictable billing cycles, construction accounting must accommodate multi-year contracts, fluctuating cost estimates, and contract-specific profitability analysis. It requires the ongoing measurement of project progress, separate tracking of job-level costs, and specialized treatment of contractual provisions that affect cash flow and reported income. As a result, construction accounting incorporates unique revenue recognition models, detailed job costing systems, change order adjustments, retainage tracking, and the continuous reassessment of long-term contract performance. The key differences between these accounting concepts are noted below.

Revenue Recognition Methods

Construction accounting uses revenue recognition methods designed for long-term contracts with fluctuating estimates. The percentage-of-completion method recognizes revenue over time based on progress toward completion, often measured by costs incurred relative to total estimated costs. Alternatively, the completed-contract method defers all revenue and profit recognition until the project is substantially finished. These approaches align reported income with project performance and risk, requiring continual reassessment of cost-to-complete estimates and contract profitability throughout the construction cycle.

Job Costing

Construction accounting relies heavily on job costing, where each project is treated as a distinct cost object and profit center. Direct costs such as labor, materials, and subcontractor fees are assigned to specific jobs, along with allocated indirect costs. This structure enables detailed tracking of budget-to-actual performance, gross margin by project, and cost-to-complete estimates. Accurate job costing supports bidding decisions, progress billings, and profitability analysis across multiple concurrent contracts.

Change Orders

Change orders are formal modifications to the original construction contract that alter project scope, pricing, or timelines. In construction accounting, they must be evaluated, approved, and incorporated into revised contract values and cost estimates. Approved change orders adjust revenue projections and budgeted costs, while pending changes may require separate tracking. Because they can significantly affect profitability and percentage-of-completion calculations, change orders demand careful documentation, updated forecasts, and continuous monitoring throughout the life of the project.

Retainage Accounting

Retainage accounting addresses the practice of withholding a percentage of each progress billing until a construction project is substantially complete. The retained amount serves as assurance of performance and quality. Contractors must record retainage as a separate receivable, since it has been earned but not yet collected. This practice affects cash flow management, working capital, and contract asset balances, requiring detailed tracking and reconciliation throughout the project lifecycle.

Long-Term Contract Considerations

Long-term construction contracts require continuous financial oversight throughout the project lifecycle. Accountants must regularly update cost-to-complete estimates, reassess projected margins, and adjust revenue recognition based on revised forecasts. Contract assets and liabilities, including overbillings and underbillings, must be closely monitored to ensure accurate financial reporting. Because projects extend over multiple reporting periods, profitability and cash flow are subject to estimation risk. This contrasts with shorter-term transactions, where financial effects are typically recognized within a single period.

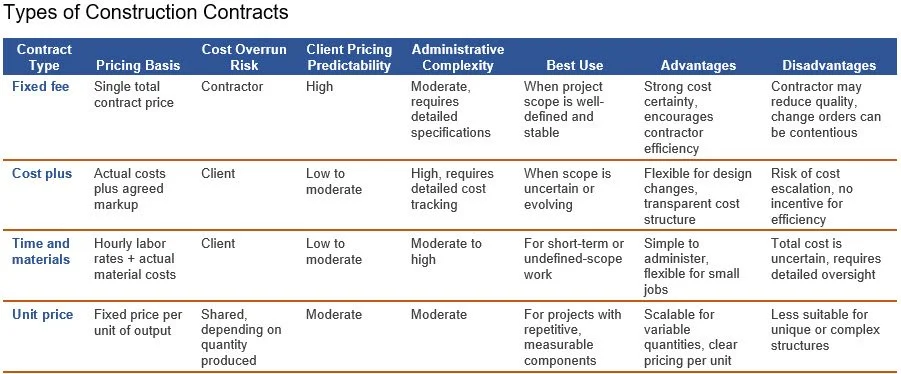

Types of Construction Contracts

There are several types of contracts than a contractor can enter into with a client. Each type has specific characteristics that tend to favor one party or the other, depending on the circumstances. We explain each one below.

Fixed Fee Contract

A fixed fee contract is used when the contractor commits to being paid a fixed amount by the client. In this situation, the costs incurred by the contractor have no impact on the price paid. This arrangement would appear to strongly favor the client, since there is no risk of paying more than the contract price. In fact, this arrangement is most common in a multi-party bidding scenario where a number of potential contractors are forced to bid against each other. It is best from the perspectives of both the client and contractor to create quite detailed specifications for a fixed fee contract, so there is little question about what is expected of the contractor and what constitutes an acceptable final outcome.

Cost Plus Contract

A cost plus contract is a cost-based method for setting the price of a construction project under a contractual arrangement. The contractor adds together the direct material cost, direct labor cost, and overhead costs for a project and adds to it a markup percentage in order to derive the price to be billed. From the client’s perspective, this can be an expensive pricing system, since costs may spiral well above initial expectations. However, it is an ideal system when there is a high degree of uncertainty regarding the design specifications of the final product.

Time-and-Materials Contract

A time-and-materials contract is a variation on the preceding cost plus contract. Customers are billed a standard hourly rate per hour worked, plus the actual cost of materials used. The standard labor rate per hour being billed does not necessarily relate to the underlying cost of the labor; instead, it may be based on the market rate for the services of someone having a certain skill set, or the cost of labor plus a designated profit percentage.

Unit-Price Contract

A unit-price contract is an arrangement in which the client pays a specific price for each unit of output. This arrangement is rarely used in a large, complex construction project where there are few units of output that are easily replicated. For example, a client is unlikely to demand a unit-price contract for each of a cluster of apartment buildings. However, the general contractor may use this type of contract with its subcontractors for selected work arrangements. For example, a general contractor for the construction of a road could enter into a unit-price contract that pays a certain amount per square foot of sidewalk installed.

A comparison table that notes the key aspects of each of these contract types appears below.

Related AccountingTools Courses

Auditing Construction Contractors

Contract Revenue Recognition

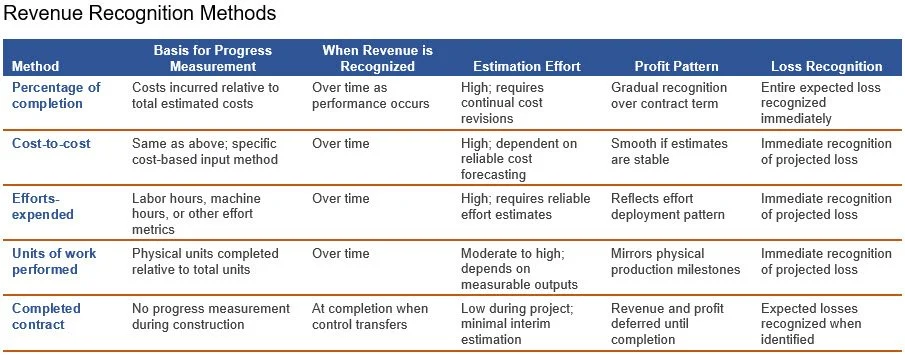

Construction contractors recognize revenue under the long-term contract guidance in Financial Accounting Standards Board (FASB) ASC 606, typically using a cost-to-cost input method to measure progress toward the satisfaction of a performance obligation over time. Revenue is recognized as performance occurs when the contractor has an enforceable right to payment and the asset being constructed has no alternative use, resulting in the recognition of contract assets and liabilities based on billings versus costs incurred. This approach requires continuous estimates of total contract costs, revisions for change orders and claims, and the immediate recognition of expected losses when a contract becomes onerous. Within this general framework there are several approaches to recognizing contract revenue, which are described below.

Percentage of Completion Method

The percentage of completion method allows a construction contractor to recognize revenue in proportion to the progress made on a long-term contract. Under guidance issued by the FASB in ASC 606, revenue is recognized over time when performance obligations are satisfied as work progresses. Contractors commonly apply a cost-to-cost input method to measure progress, as shown below.

Percentage of completion = Costs incurred to date ÷ Total estimated contract

The resulting percentage is multiplied by the total contract price to determine cumulative revenue, from which prior recognized revenue is subtracted to derive current-period revenue. This method requires continual updates of estimated total costs, careful evaluation of change orders, and immediate recognition of anticipated contract losses.

Cost-to-Cost Method

You can apply the cost-to-cost method to recognize revenue over time when performance obligations are satisfied. This approach measures progress toward completion by comparing costs incurred to date with total estimated contract costs. The recognition formula is:

Progress toward completion = Costs incurred to date ÷ Total estimated contract costs

The resulting percentage is applied to the transaction price to determine cumulative revenue recognized, and previously recognized amounts are deducted to derive current-period revenue. The method requires reliable cost estimation, continuous updates for revisions, and careful treatment of change orders and claims. If revised estimates indicate an overall contract loss, the contractor recognizes the entire expected loss immediately.

Efforts-Expended Method

You may measure progress toward completion using an efforts expended input method when it faithfully depicts performance. Instead of focusing strictly on costs incurred, this approach measures progress based on labor hours, machine hours, or other direct effort metrics relative to total expected efforts. The recognition formula is:

Progress toward completion = Efforts expended to date ÷ Total estimated efforts

The resulting percentage is applied to the transaction price to determine cumulative revenue recognized. This method is appropriate when labor or other measurable efforts best represent value transferred to the customer. Contractors must reliably estimate total efforts, update those estimates as conditions change, and recognize expected contract losses immediately if projected total costs exceed the transaction price.

Units of Work Performed Method

You may apply a units-of-work performed output method when it best reflects the transfer of control to the customer. This approach measures progress based on objectively verifiable units completed, such as miles of pipeline laid, floors constructed, or cubic yards excavated, relative to total contracted units. The recognition formula is:

Progress toward completion = Units completed to date ÷ Total contracted units

The resulting percentage is applied to the transaction price to determine cumulative revenue recognized. This method is appropriate when distinct physical outputs can be measured reliably and correspond directly to value delivered. Contractors must ensure that unit measures faithfully depict performance and must revise estimates and recognize expected losses promptly if total projected costs exceed the contract price.

Completed Contract Method

The completed contract method is applied when a contractor does not meet the criteria for recognizing revenue over time. In this situation, revenue is recognized at a point in time, typically when a project is substantially complete and control of the asset transfers to the customer. Throughout the construction period, the contractor accumulates costs in construction in progress and records billings separately, but does not recognize revenue or gross profit. Once the performance obligation is fully satisfied, the contractor recognizes the entire contract revenue and the related costs in the same reporting period. This method reduces reliance on estimates during construction, but it can create significant fluctuations in reported revenue and profit, since results are deferred until completion.

The differences between these recognition methods are noted in the following table.

Construction Accounting Concepts

As construction projects evolve, contractors must address unpriced change orders, disputed contract claims, overbilling liabilities, and retainage provisions that materially affect their reported revenue, gross margin, and cash flow. Each of these elements introduces estimation risk, documentation requirements, and potential balance sheet volatility. Any failure to account for them properly can distort work-in-progress schedules, misstate contract assets and liabilities, and trigger disputes with owners, lenders, or sureties. The following subtopics examine the technical accounting treatment, recognition thresholds, measurement considerations, and disclosure implications associated with these complex contract components.

Unpriced Change Orders

A construction company is dealing with an unpriced change order when the parties cannot initially agree on the price to be charged by the company to the client for a modification of the underlying construction contract. The recovery of funds from an unpriced change order is considered probable when the client has approved of the scope change in writing, and the contractor has documented the related costs of the change, and the contractor has a favorable history of settling change orders. There are three variations on how to deal with an unpriced change order. They are as follows:

When it is not probable that the costs associated with an unpriced change order will be paid back to the contractor through a price increase, the costs are added to the total estimated cost of the project; the result is a decline in the estimated amount of profit that the job will generate.

When it is probable that an upward adjustment to the contract price will be forthcoming, defer the recognition of any costs incurred under the change order until the price has been settled.

When it is probable that the prospective upward adjustment to the contract price will exceed the costs associated with the contract and the amount of the price can be reliably estimated, adjust the contract price to reflect the amount of the increase in costs. Do not recognize revenue exceeding the amount of costs incurred for the change order unless receipt of the estimated revenue amount is assured beyond a reasonable doubt.

When a change order is in dispute, it should be evaluated as a claim rather than a change order (as noted next).

Contract Claims

A construction company is generally prohibited from recognizing revenue related to contract claims because of the significant uncertainty surrounding client approval and payment. Revenue may be recorded only when it is probable that additional consideration will be received and the amount can be reliably estimated. To reach this threshold, management must rely on objective, verifiable evidence supporting the claim and demonstrate a sound legal basis, either inherent in the contract or confirmed by legal counsel. The additional costs must arise from unforeseen circumstances rather than the contractor’s deficient performance. In addition, the related costs must be specifically identifiable and reasonable in light of the work performed. Even when these criteria are met, recognized revenue is capped at the associated contract costs.

Overbilling Liabilities

When the amount billed on a construction project exceeds the costs incurred to date, the excess represents a billing in advance of performance. Under the percentage-of-completion method, this situation reflects that the contractor has invoiced the client for work not yet performed, creating a temporary overstatement of revenue relative to the actual progress of the project. To ensure accurate financial reporting, this difference is recorded as a liability on the balance sheet, typically labeled “Billings in Excess of Costs and Estimated Earnings.” This liability indicates an obligation to perform future work or, in some cases, the potential need to refund unearned amounts. As the contractor incurs additional costs and progresses on the project, the liability is gradually reduced, aligning revenue recognition with actual performance. This treatment ensures compliance with the matching principle and prevents premature revenue recognition.

Contract Retainage

A customer may withhold a specified amount from the contract price until satisfied with the completed work. Doing so gives the customer some leverage over the contractor to complete the work in a satisfactory manner. These retainage amounts may still be recorded as receivables, but could be classified as long-term receivables if the customer has the right to hold these amounts for more than a year. In addition, the IRS allows a company to exclude retainages from the recognition of income until there is an unconditional right to receive them.

Construction Accounting Reports

Effective construction accounting depends on disciplined cost tracking and transparent project reporting. Three core tools support this framework: the job cost sheet, which captures detailed cost accumulation by contract; the construction-in-progress report, which summarizes project-level financial status in the general ledger; and the work-in-progress schedule, which reconciles costs, billings, and estimated profitability across all active jobs. Together, these reports provide management, lenders, and sureties with a structured view of performance, margin trends, and contract asset or liability positions.

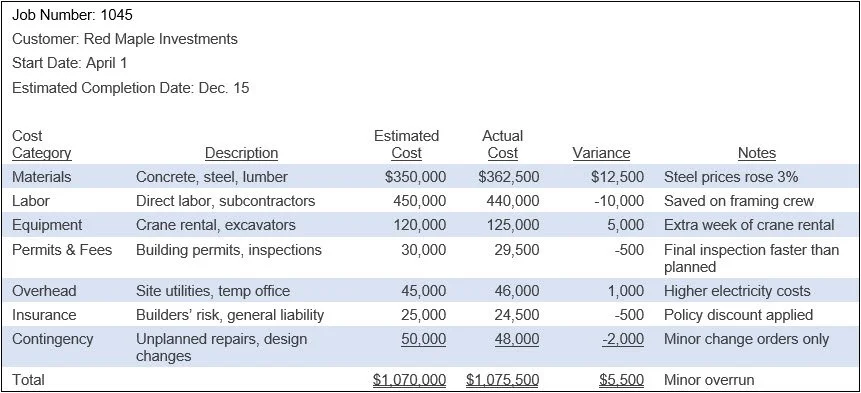

Job Cost Sheet

A job cost sheet is a compilation of the actual costs of a job. The report is compiled by the accounting department and distributed to the management team, to see if a job was correctly bid. The sheet is usually completed after a job has been closed, though it can be compiled on a concurrent basis. A job cost sheet can be quite complex to create, since it may involve different labor rates for dozens of people, as well as a labor allocation for the payroll taxes and benefits incurred by those people, and overtime, plus potentially hundreds of components that should include the cost of shipping and handling. Depending upon the format of the job cost sheet, it may also include subtotals of costs for materials, labor, and overhead. A sample job cost sheet appears in the following exhibit.

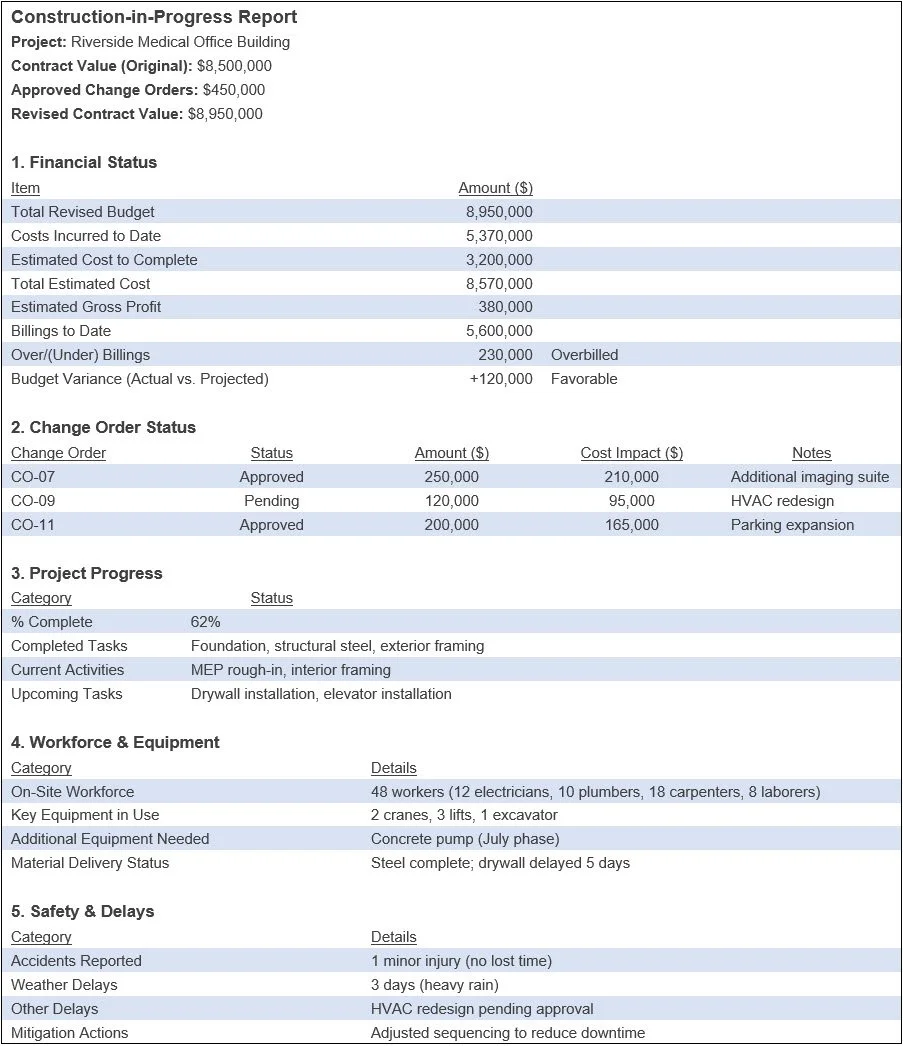

Construction-in-Progress Report

A construction-in-progress report provides a snapshot of the current status of a construction project. It lists the total project budget, funds used to date, and remaining funds, as well as the details on any approved or pending changes that impact costs. The report also notes discrepancies between projected and actual expenses. In addition to these financial issues, the report also notes which tasks have been completed, highlights current work activities, and provides an overview of upcoming tasks. In addition, the report summarizes the number and type of workers on-site, the equipment being used or which is needed, and the status of material deliveries. Further, the report itemizes any accidents that have occurred, delays and the reasons for them, and any issues impacting the progress or quality of the work. Finally, the report lists all completed quality checks, pending inspections, and any non-conformance issues found. In short, this report helps maintain transparency and ensures that all parties are informed about a project's current state, potential challenges, and future direction. A sample construction-in-progress report appears in the following exhibit.

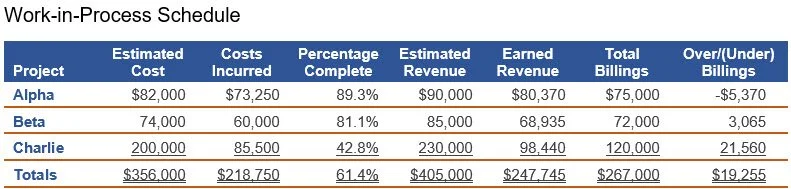

Work-in-Progress Schedule

A useful tool for keeping track of the percentage of completion is the work-in-progress schedule. It tracks a project’s ongoing profitability by monitoring three measurements, which are the percentage of completion, amount of revenue earned to date, and the amount of any any over/under billings. The schedule is useful for revealing negative trends early in a project, before they can blow up into larger issues. It also shows the extent to which a project has been either overbilled or underbilled, by calculating the difference between actual billings and recognized revenues.

An example of a work-in-progress schedule appears in the next exhibit, where earned revenue is calculated as the total estimated revenue for a project, multiplied by the percentage complete. This number is compared to total billings to date to arrive at the over/(under) billing for a project.

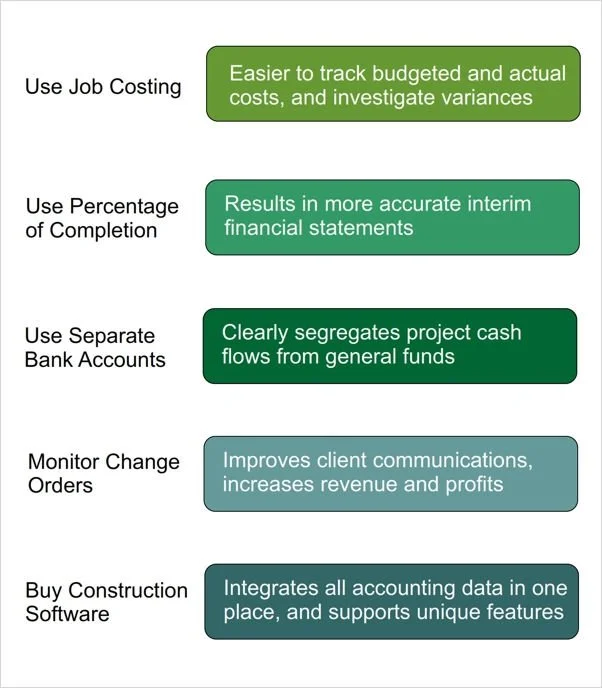

Top 5 Construction Accounting Best Practices

Effective construction financial management requires disciplined cost tracking, structured revenue recognition, cash segregation, and technology built for project environments. The following subtopics outline practical accounting and control strategies that strengthen margin oversight, improve reporting reliability, protect cash flow, and support lender and surety expectations across complex, long-term construction contracts.

Use Job Costing for Project Tracking

Use job costing as the primary mechanism for monitoring project performance at a granular level. A properly designed job cost system assigns all direct materials, direct labor, subcontractor charges, equipment usage, and allocated overhead to individual contracts or cost codes. This structure enables management to compare actual costs to budgeted amounts in real time and evaluate percentage of completion using reliable data. As variances emerge, project managers can investigate root causes such as labor inefficiency, material waste, or scope creep before margins deteriorate further. Detailed cost histories also create a valuable database for future estimating, allowing the company to refine its unit pricing, contingency assumptions, and bid strategies based on documented historical performance rather than unsupported assumptions.

Implement Percentage-of-Completion Revenue Recognition

Use the percentage-of-completion method to recognize revenue as performance obligations are satisfied over time, typically measured using a cost-to-cost input approach. By matching recognized revenue to the proportion of work completed, contractors align their income recognition with underlying project economics rather than deferring results until final delivery. This approach enhances the relevance of interim financial statements by reflecting current estimates of total contract costs, gross profit, and remaining obligations. It also improves the trend analysis of margins and backlog performance. From a financing perspective, percentage-of-completion reporting supports lender and surety evaluations by presenting timely, credible measures of contract assets, liabilities, and overall project profitability, thereby strengthening access to credit and bonding capacity.

Maintain Separate Bank Accounts for Large Projects

Establishing dedicated bank accounts for significant construction contracts creates a clear segregation of project cash flows from general operating funds. All contract receipts, progress billings, retainage collections, and project-specific disbursements flow through a controlled account structure, thereby reducing the risk of commingling or inadvertent misallocation. This segregation strengthens internal controls over cash, simplifies bank reconciliations, and improves the accuracy of project-level cash reporting. It also provides transparent audit trails that support lender, surety, and owner oversight.

Monitor Change Orders Closely

Track change orders meticulously to ensure each modification to scope, pricing, or schedule is properly initiated, documented, priced, reviewed, and formally approved before work proceeds. Every approved change should be incorporated into the revised contract value, updated job cost budget, and forecasted gross margin. Failure to control change orders can distort percentage-of-completion calculations, delay progress billings, create disputes over entitlement, and gradually erode profit margins through unpriced or underpriced work. A disciplined change order workflow establishes clear authorization thresholds, preserves supporting documentation, and links field directives to accounting updates. This structure improves internal project control, enhances communication with clients and subcontractors, and protects both revenue recognition and cash flow predictability.

Invest in Construction-Specific Accounting Software

Construction entities should deploy accounting systems specifically engineered for project-based environments. These platforms integrate job cost ledgers, cost codes, committed cost tracking, subcontract management, certified payroll reporting, progress billing under percentage-of-completion methods, and automated retainage calculations. They also support change order management, real-time cost-to-complete forecasting, and work-in-progress schedule generation. In contrast, generic accounting software typically emphasizes transactional bookkeeping and lacks the dimensional reporting and contract-level controls required for long-term construction projects. Industry-specific systems enhance internal control over costs, reduce revenue recognition errors, improve visibility into margin fade or gain, and streamline compliance with lender, surety, and regulatory reporting requirements, thereby strengthening both financial accuracy and operational decision-making.

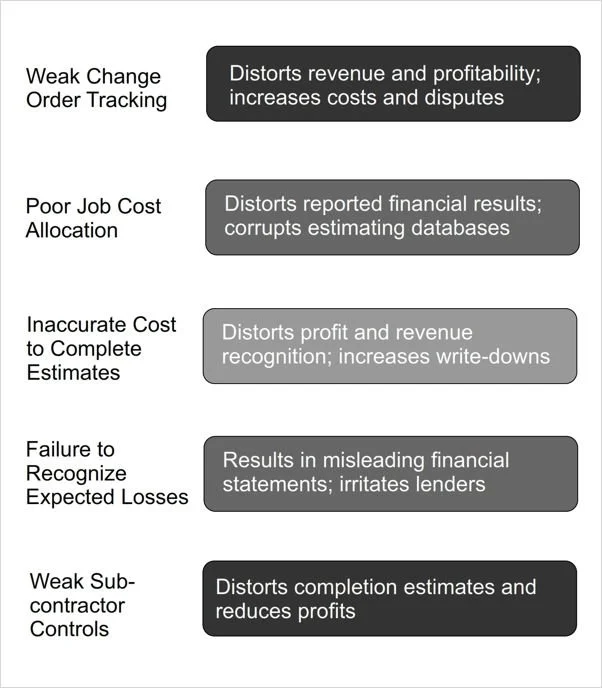

Top 5 Construction Accounting Errors

Construction accounting demands disciplined cost tracking, accurate forecasting, and strict adherence to revenue recognition principles. When internal controls weaken in these areas, financial statements become unreliable and project profitability becomes distorted. The following errors represent recurring breakdowns that materially affect margins, cash flow, bonding capacity, and the credibility of reported results.

Weak Change Order Tracking

Weak change order tracking distorts revenue recognition, cost control, and contract profitability analysis. Construction projects routinely evolve through scope modifications, design revisions, and unforeseen site conditions. If change orders are not documented, priced, and approved in a timely manner, contractors may incur costs without and corresponding revenue adjustments. This results in understated contract assets, margin erosion, and inaccurate percentage-of-completion calculations. Poor tracking also weakens internal controls, increases dispute risk, and impairs cash flow forecasting. Over time, unmanaged change orders can convert profitable contracts into loss positions and undermine the reliability of a contractor’s financial statements.

Poor Job Cost Allocation

Poor job cost allocation distorts project profitability, financial reporting accuracy, and management decision-making. When labor, materials, equipment usage, subcontractor charges, or overhead are misallocated, individual job margins become unreliable. Management may believe a project is profitable when it is actually generating losses, or vice versa. Inaccurate allocations also impair percentage-of-completion calculations, leading to misstated revenue, contract assets, and gross profit. Over time, flawed job histories corrupt estimating databases, resulting in systematically underpriced bids. Poor allocation further weakens internal controls, obscures cost overruns, and increases the risk of disputes with owners, lenders, and auditors.

Inaccurate Cost-to-Complete Estimates

Inaccurate cost-to-complete estimates distort revenue recognition, gross profit, and contract asset or liability balances under percentage-of-completion accounting. When total estimated costs are understated, the calculated percentage of completion is overstated, accelerating revenue and profit recognition. Conversely, overstated cost projections defer earnings and may mask operational performance. Because construction accounting relies on continuous revisions of expected costs, flawed estimates undermine financial statement reliability and can trigger material misstatements. Ultimately, weak estimating controls increase the risk of earnings reversals, write-downs, and unexpected contract losses.

Failure to Recognize Expected Losses

The failure to recognize expected losses is a major accounting error, because long-term contracts require continuous re-estimation of total costs and profitability. Under ASC 606, when updated forecasts indicate that total contract costs will exceed total contract revenue, the entire anticipated loss must be recognized immediately. Delaying recognition overstates assets, understates liabilities, and inflates current earnings, creating materially misleading financial statements. It also distorts work-in-process schedules, bonding capacity calculations, and bank covenant compliance metrics. Since contractors rely heavily on external financing and surety relationships, misstated results can damage credibility and restrict access to capital.

Weak Subcontractor Controls

Weak control over subcontractor costs is a major concern, because subcontractor charges often represent a substantial portion of total contract costs. Without rigorous review of subcontract agreements, change orders, pay applications, and lien waivers, contractors risk overbilling, duplicate payments, or unauthorized scope expansions. Inaccurate coding of subcontractor invoices to job cost ledgers distorts percentage-of-completion calculations and gross profit estimates. Poor monitoring also impairs cost-to-complete forecasts, leading to understated loss provisions or reduced margins. Weak controls over retainage, insurance compliance, and back charges further expose the contractor to financial misstatements, cash flow strain, and disputes across multiple reporting periods.