Governmental Accounting Explained

/What is Governmental Accounting?

Government accounting is the system used by public sector entities to record, report, and control financial activities in accordance with statutory, budgetary, and accountability requirements. Unlike for-profit accounting, its primary objective is stewardship of public resources rather than profit measurement. It emphasizes fund accounting, legal compliance, budgetary control, and transparency. Governments prepare financial statements that distinguish between governmental activities, business-type activities, and fiduciary activities. Measurement focuses on both current financial resources and long-term economic resources, depending on the reporting level. Standards are typically established by bodies such as the Governmental Accounting Standards Board in the United States.

What is Fund Accounting?

A fund is an accounting entity with a self-balancing set of accounts that is used to record financial resources and liabilities, as well as operating activities, and which is segregated in order to carry on certain activities or attain targeted objectives. A fund is not a separate legal entity. Funds are used by governments because they need to maintain very tight control over their resources, and funds are designed to monitor resource inflows and outflows, with particular attention to the remaining amount of funds available. By segregating resources into multiple funds, a government can more closely monitor resource usage, thereby minimizing the risk of overspending or of spending in areas not authorized by a government budget.

Some types of funds use a different basis of accounting and measurement focus. To clarify the difference between these concepts, the basis of accounting governs when transactions will be recorded, while the measurement focus governs what transactions will be recorded.

What are the Main Types of Governmental Fund Accounting?

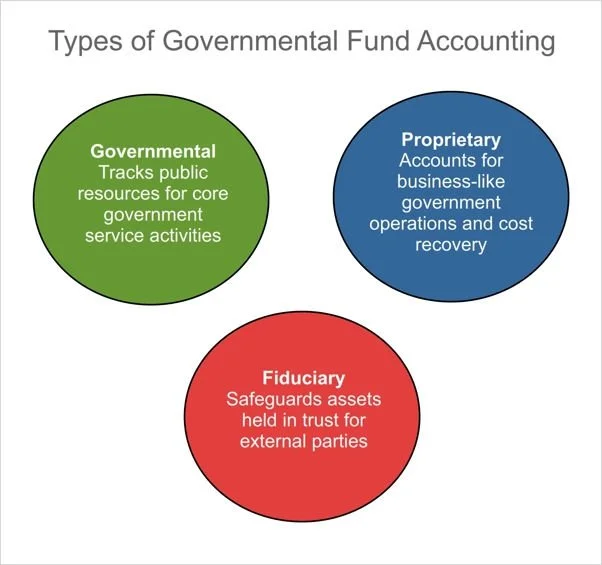

Government accounting is organized into three primary fund categories, each reflecting a distinct measurement focus and accountability objective. They are noted below.

1. Governmental Fund Accounting

Governmental funds are used to account for core public services financed primarily through taxes and intergovernmental revenues. These funds follow the modified accrual basis of accounting and the current financial resources measurement focus. Revenues are recognized when they are measurable and available, while expenditures are recognized when a liability is incurred. Capital assets and long-term debt are not reported within governmental funds themselves but appear in the government-wide statements. Common governmental funds include the general fund, special revenue funds, capital projects funds, debt service funds, and permanent funds. The emphasis is on budgetary compliance and short-term fiscal accountability.

2. Proprietary Fund Accounting

Proprietary funds account for activities that operate in a manner similar to private businesses. They use the accrual basis of accounting and the economic resources measurement focus. Revenues are recognized when earned and expenses when incurred, with full reporting of capital assets and long-term liabilities. There are two types: enterprise funds, which serve external customers such as utilities or transit systems, and internal service funds, which provide goods or services to other governmental departments. The emphasis is on cost recovery, operational efficiency, and long-term financial sustainability.

3. Fiduciary Fund Accounting

Fiduciary funds are used when a government holds assets in a trustee or agency capacity for others. These resources cannot be used to support the government’s own programs. Fiduciary funds use the accrual basis and focus on safeguarding assets and ensuring proper distribution. Examples include pension trust funds, investment trust funds, and custodial funds.

When combined, these three forms of fund accounting give government managers a clear view of the financial situation of all aspects of government operations. A summary of the three types of fund accounting appears in the following graphic.

The Basis of Accounting

The basis of accounting governs when transactions will be recorded. This concept applies to the recognition and reporting of revenues, expenditures, expenses, and transfers. For governmental accounting purposes, the cash basis, accrual basis, and modified accrual basis may apply. Summaries of these three variations on the basis of accounting are as follows:

Cash basis of accounting. Under the cash basis of accounting, the receipt of cash triggers the recognition of revenue and expenses, while the disbursement of cash triggers the recognition of expenditures, expenses, and transfers out. For example, a government receives an invoice from a supplier for supplies. The terms of the invoice state that the government does not have to pay the invoice for 60 days. Under the cash basis, the government does not recognize the expense related to the supplies until payment is made, which is 60 days after the supplies were received.

Accrual basis of accounting. Under the accrual basis of accounting, the occurrence of a business event triggers the recognition of most transactions, irrespective of the underlying movement of cash. This basis of accounting is generally better than the cash basis, since transactions are recorded immediately, without the time delay associated with cash-basis transactions.

Modified accrual basis of accounting. Under the modified accrual basis of accounting, revenue and governmental fund resources (such as the proceeds from a debt issuance) are recognized when they become susceptible to accrual. This means that these items are not only available to finance the expenditures of the period, but are also measurable. The “available” concept means that the revenue and other fund resources are collectible within the current period or sufficiently soon thereafter to be available to pay for the current period’s liabilities. The “measurable” concept allows a government to not know the exact amount of revenue in order to accrue it.

A summary of the triggering event for each basis of accounting appears in the following exhibit.

The Focus of Governmental Financial Reporting

The key measurement focus in a government fund’s financial statements is on expenditures, which are decreases in the net financial resources of a fund. Most expenditures should be reported when a related liability is incurred. This means that a governmental fund liability and expenditure is accrued in the period in which the fund incurs the liability.

The focus of governmental funds is on current financial resources, which means assets that can be converted into cash and liabilities that will be paid for with that cash. Stated differently, the balance sheets of governmental funds do not include long-term assets or any assets that will not be converted into cash in order to settle current liabilities. Similarly, these balance sheets will not contain any long-term liabilities, since they do not require the use of current financial resources for their settlement. This measurement focus is only used in governmental accounting.

The Comprehensive Annual Financial Report

The comprehensive annual financial report is a detailed presentation of a government’s financial condition over a fiscal year. It includes three main sections: introductory, financial, and statistical, offering insights into operations, financial position, and long-term trends. The financial section contains audited financial statements prepared in accordance with GASB standards. This report enhances transparency and accountability, providing stakeholders with a complete view of how public resources are managed and spent.

Governmental Accounting FAQs

What do governmental accountants do?

Governmental accountants record, classify, and report the financial activities of public sector entities. They prepare fund-based financial statements, ensure compliance with budgetary and legal requirements, implement internal controls, support audits, and apply governmental accounting standards. Their work emphasizes accountability, transparency, and proper stewardship of taxpayer resources rather than profitability.

What skills do you need to be a government accountant?

Government accountants need strong knowledge of governmental accounting standards, fund accounting, and budgetary compliance. Analytical skills are essential for interpreting financial data and monitoring expenditures. Attention to detail supports accurate reporting and internal controls. They also require proficiency in accounting systems, communication skills for stakeholder reporting, and ethical judgment.

What are the differences between financial accounting and governmental accounting?

Financial accounting focuses on profitability, investor reporting, and accrual-based financial statements under GAAP or IFRS. Governmental accounting emphasizes accountability, budgetary compliance, and stewardship of public resources. It relies heavily on fund accounting and modified accrual for governmental funds, highlighting legal restrictions rather than earnings and shareholder value.

Who sets the accounting standards for government entities?

In the United States, the Governmental Accounting Standards Board sets accounting standards for state and local governments. For the federal government, standards are issued by the Federal Accounting Standards Advisory Board. These bodies establish authoritative guidance to ensure consistency, transparency, and accountability in governmental financial reporting.