Fixed Asset Accounting Explained

/What is a Fixed Asset?

A fixed asset is property that can be used for an extended period of time in business operations. Common examples include buildings, machinery, vehicles, and equipment. It has a useful life that spans multiple reporting periods, and whose cost exceeds a certain minimum limit (called the capitalization limit). After recognition, the cost of a fixed asset is systematically allocated to expense through depreciation over its useful life. It is classified as a long-term asset, since it will remain on your books for an extended period of time. In a capital-intensive business, fixed assets may very well be the largest asset class on an organization’s balance sheet.

Examples of Fixed Assets

In an organization’s accounting records, there is a separate account for each general type of fixed asset. When a newly-acquired fixed asset is recognized, it is stored in one of these accounts. The more common fixed asset accounts are noted below:

Buildings. Includes all facilities owned by the entity. This account also includes buildings constructed by the organization.

Computer equipment. Includes all types of computer equipment, such as servers, desktop computers, and laptops.

Computer software. Usually only includes the most expensive types of software; all others are charged to expense as incurred.

Construction in progress. This is an accumulation account in which are recorded the costs of construction. Once an asset (usually a building) is completed, the balance is moved to the relevant fixed asset account.

Furniture and fixtures. Includes tables, chairs, filing cabinets, cubicle walls, and so forth.

Intangible assets. Includes all nontangible assets, such as the costs of patents, radio licenses, and copyrights.

Land. Includes the purchased cost of land, and may also include the cost of land improvements (which are otherwise recorded in a separate account).

Leasehold improvements. Includes the costs incurred to renovate leased space.

Machinery. Typically refers to production machinery.

Office equipment. Includes copiers and similar administrative equipment, but not computers (for which there is a separate account).

Tools. A production business might elect to record the cost of its tools within a separate classification, though only if there is a substantial investment in tools. Lower-cost tools may be charged to expense as incurred.

Vehicles. Can include company cars, trucks, and more specialized moving equipment, such as fork lifts.

Warehouses. A business that owns a number of warehouses may elect to record these structures within a separate classification.

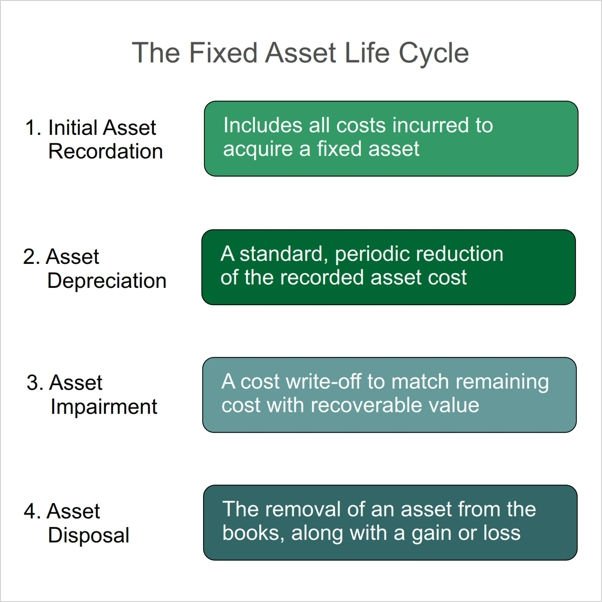

The Fixed Asset Life Cycle

The typical fixed asset is subject to a standard set of accounting activities over the course of its life. These activities can result in a large number of accounting transactions, depending on the lifespan of an asset and whether its value changes over time. The key events in this fixed asset life cycle are as follows:

Initial asset recordation. This is the initial entry of the cost of a newly-acquired assets into the books of the organization.

Asset depreciation. This is a pre-calculated, periodic reduction in the cost of the asset over its useful life, to reflect the expected amount of wear and tear that it will undergo.

Asset impairment. This is a reduction in the remaining cost of the asset, which occurs whenever the net cost of the asset declines below its current market value.

Asset disposal. This is the removal of the remaining cost of the asset from the organization’s accounting records, either because it has been sold, scrapped, or otherwise disposed of.

Step 1: Accounting for the Initial Acquisition of a Fixed Asset

You should initially record a fixed asset at the historical cost of acquiring it, which includes the costs to bring it to the condition and location necessary for its intended use. These costs include the physical construction of the asset, the demolition of any preexisting structures, freight charges, sales taxes, installation fees, and testing fees. If these preparatory activities will occupy a period of time, you can also include in the cost of the asset the interest costs related to the cost of the asset during the preparation period.

On the assumption that the asset was purchased on credit, the initial entry is a credit to accounts payable and a debit to the applicable fixed asset account for the cost of the asset. Here is an example of an initial acquisition entry for manufacturing equipment with a initial cost of $50,000:

What if a fixed asset is acquired through an exchange of assets? If so, measure the asset acquired at the fair value of the asset surrendered to the other party. If the fair value of the asset received is more clearly evident than the fair value of the asset surrendered, measure the acquired asset at its own fair value. In either case, recognize a gain or loss on the difference between the recorded cost of the asset transferred to the other party and the recorded cost of the asset that has been acquired.

As an example, ABC company exchanges a color copier with a carrying amount of $18,000 with another business for a print-on-demand publishing station. The color copier had an original cost of $30,000, and had incurred $12,000 of accumulated depreciation as of the transaction date. No cash is transferred as part of the exchange, and ABC cannot determine the fair value of the color copier. The fair value of the publishing station is $20,000. The company can record a gain of $2,000 on the exchange, which is derived from the fair value of the publishing station that it acquired, less the carrying amount of the color copier that it gave up. The related journal entry is:

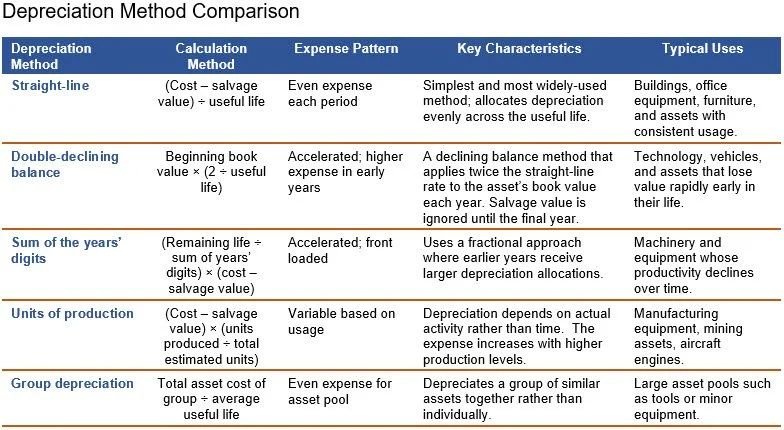

Step 2: Accounting for the Depreciation of a Fixed Asset

The amount of the asset is gradually reduced over subsequent periods with ongoing depreciation entries, on the theory that an asset’s value will decline over an extended period of time. There are several variations on the depreciation calculation, including the straight-line, double-declining balance, and units of production methods. The characteristics and calculation methods for the most common depreciation methods are noted in the following table.

No matter which depreciation method is used, there will be a monthly depreciation charge, for which the entry is a debit to depreciation expense and a credit to accumulated depreciation. The balance in the accumulated depreciation account is paired with the amount in the fixed asset account, resulting in a reduced asset balance.

For example, a company controller calculates that the total depreciation for the month of May for all assets is $25,000. This results in the following entry, where the company charges $25,000 to depreciation expense and places the offsetting credit in the accumulated depreciation account (which is a contra asset account that offsets the fixed assets line item on the balance sheet):

In the following month, the controller decides to show a higher level of precision at the expense account level, and instead elects to apportion the $25,000 of depreciation among different expense accounts, so that each class of asset has a separate depreciation charge. The entry is:

The journal entry to record the amortization of intangible assets is fundamentally the same as the entry for depreciation, except that the accounts used substitute the word “amortization” for depreciation. An example follows, where $4,000 is being charged to amortization expense:

Step 3: Accounting for the Impairment of a Fixed Asset

You should periodically test all major fixed assets for impairment. Impairment is present when an asset’s carrying amount is greater than its undiscounted future cash flows. When this is the case, record a loss in the amount of the difference, which reduces the carrying amount of the asset. If there is still some carrying value left, then this amount will still need to be depreciated, though probably at a much lower monthly rate than had previously been the case. Asset impairments are less likely towards the end of an asset’s useful life, because ongoing depreciation has reduced its carrying amount to a great extent.

As an example of a fixed asset impairment journal entry, the following example shows the recognition of a $50,000 impairment charge against an asset. The impairment loss is an expense in the current period, while the offsetting accumulated impairment loss is a contra asset that is offset against and reduces the remaining asset balance.

Step 4: Accounting for the Disposal of a Fixed Asset

At the end of a fixed asset's useful life, it is sold off or scrapped. This situation arises when the asset is of no further value to the organization. The related accounting entry in this situation is to remove the asset and all related accumulated depreciation from the entity’s accounting records.

There are several scenarios under which you may dispose of a fixed asset. The first situation arises when you are eliminating a fixed asset without receiving any payment in return. This is a common situation when a fixed asset is being scrapped because it is obsolete or no longer in use, and there is no resale market for it. In this case, reverse any accumulated depreciation and reverse the original asset cost. If the asset is fully depreciated, that is the extent of the entry. A sample entry follows, where a fully-depreciated asset that originally cost $100,000 is removed from the books:

A variation on this situation is to write off a fixed asset that has not yet been completely depreciated. In this case, write off the remaining undepreciated amount of the asset to a loss account. In the following entry, an asset that originally cost $100,000 is being eliminated before $20,000 of depreciation has been recognized.

Alternatively, you may sell an asset, so that you receive cash (or some other asset) in exchange for the fixed asset being sold. Depending upon the price paid and the remaining amount of depreciation that has not yet been charged to expense, this can result in either a gain or a loss on sale of the asset. In the following sample entry, a business sells a machine that cost it $100,000, receiving $35,000 from the buyer. The seller has already recorded $70,000 of depreciation expense.

What if the business had sold the machine for $25,000 instead of $35,000? Then there would be a loss of $5,000 on the sale. The entry would be:

In all four of the preceding entries, the main point was to flush the asset out of the accounting system, so that no asset or accumulated depreciation balance is left on the books.

What is the Accounting Treatment for the Revaluation of Fixed Assets?

A company that is using the IFRS accounting framework can elect to measure its fixed assets under the revaluation model. Under this approach, you can carry a fixed asset at its fair value, less any subsequent accumulated depreciation and accumulated impairment losses. You can only use it if it is possible to reliably measure the fair value of an asset. You must also make revaluations with sufficient regularity to ensure that the amount at which an asset is carried in the company’s records does not vary materially from its fair value. The revaluation method is unique to IFRS; you cannot use it if you are using the GAAP framework.

For example, Nautilus Tours elects to revalue one of its tourism submarines, which originally cost $12 million and has since accumulated $3 million of depreciation. It is unlikely that the fair value of the submarine will vary substantially over time, so Nautilus adopts a policy to conduct revaluations for all of its submarines once every three years. An appraiser assigns a value of $9.2 million to the submarine. Nautilus creates the following entry to eliminate all accumulated depreciation associated with the submarine:

At this point, the net cost of the submarine in Nautilus’ accounting records is $9 million. Nautilus also creates the following entry to increase the carrying amount of the submarine to its fair value of $9.2 million:

Three years later, on the next scheduled revaluation date, the appraiser reviews the fair value of the submarine, and determines that its fair value has declined by $350,000. Nautilus uses the following journal entry to record the change:

This final entry eliminates all of the revaluation gain that had been recorded in other comprehensive income, and also recognizes a loss on the residual portion of the revaluation loss.

Fixed Asset Accounting Best Practices

There are a number of enhancements that can be made to your fixed asset recordkeeping practices. Consider the following options:

Establish a clear capitalization policy. Define capitalization thresholds, useful life guidelines, and asset categories so that staff consistently determine which expenditures qualify as fixed assets.

Maintain a detailed fixed asset register. Record each asset’s description, acquisition date, cost, location, responsible department, and accumulated depreciation to create a complete audit trail.

Use standardized asset categories. Classify assets into consistent groups such as buildings, machinery, vehicles, and IT equipment to simplify depreciation calculations and reporting.

Assign unique asset identification numbers. Tag each asset with a barcode or identification number that links to the fixed asset register, improving tracking and inventory control.

Document acquisition costs thoroughly. Include purchase price, freight, installation, testing, and other directly attributable costs to ensure that the asset’s recorded value is complete.

Record assets promptly upon acquisition. Enter assets into the accounting system as soon as they are placed in service to ensure that depreciation begins in the correct reporting period.

Standardize depreciation methods and useful lives. Use consistent depreciation policies across similar asset classes to maintain comparability in the financial statements.

Review useful lives periodically. Reassess depreciation estimates when operational conditions change or when assets are used differently than originally expected.

Conduct regular physical inventories of assets. Perform periodic counts and inspections to verify that recorded assets still exist and are in usable condition.

Investigate and resolve asset discrepancies. Promptly review differences between the physical inventory and the fixed asset register to identify theft, loss, or recordkeeping errors.

Track asset locations and custodians. Assign responsibility for major assets to departments or individuals so that equipment can be easily located and monitored.

Reconcile the fixed asset subledger to the general ledger. Perform regular reconciliations to confirm that asset balances in the detailed register agree with the general ledger totals.

Monitor construction-in-progress accounts. Track capital projects carefully and transfer costs to the appropriate asset category once the asset is placed into service.

Review impairment indicators regularly. Evaluate whether changes in market conditions, technology, or usage suggest that an asset’s carrying amount may not be recoverable.

Use automated fixed asset management systems. Implement specialized software that integrates with the general ledger to reduce manual errors and streamline depreciation calculations.

Retain supporting documentation. Maintain invoices, contracts, disposal records, and appraisal reports to support asset valuations and facilitate audits.

These practices help ensure that fixed asset records remain accurate, depreciation is calculated correctly, and organizations maintain strong control over their long-term assets.

Fixed Asset Accounting Special Cases

There are many special accounting scenarios involving an organization’s investment in fixed assets. In the following sub-sections, we have noted the proper accounting treatment for a number of these situations.

When to Capitalize Software

The accounting for software varies depending on the purpose of the software, the stage of development, and the manner in which it is delivered or sold. Based on the document you provided, the primary scenarios in which software accounting differs are as follows:

Internal-use software. This is software developed or acquired solely for a company’s internal operations, such as accounting systems or production automation tools. Costs are capitalized only after management commits funding and it becomes probable that the project will be completed and will function as intended.

Internal-use software accessed through a hosting arrangement. In cloud computing or SaaS arrangements, the software resides on a third party’s servers while the customer accesses it remotely. Implementation costs may be capitalized and amortized over the hosting arrangement term.

Website development costs. Websites are accounted for using guidance similar to internal-use software. Some costs, such as developing site functionality or graphics, may be capitalized, while others, such as content input or search engine registration fees, are expensed.

Software intended for sale or lease. When software will be sold externally, the accounting follows a different model. Research and development costs are expensed until technological feasibility is established, after which certain development costs can be capitalized.

How to Account for a Fixed Asset Insurance Claim

When a fixed asset is damaged, destroyed, or otherwise impaired and an insurance claim is filed, the accounting treatment depends on the relationship between the insurance proceeds, the carrying amount of the asset, and the timing of the recovery. The following scenarios describe the typical accounting outcomes:

Insurance proceeds equal the carrying amount of the asset. If the insurance reimbursement exactly equals the asset’s carrying amount at the time of the loss, the asset is removed from the books and the proceeds are recorded as cash. No gain or loss is recognized because the recovery equals the book value of the asset.

Insurance proceeds exceed the carrying amount of the asset. When the insurance settlement exceeds the asset’s carrying amount, the excess amount is recognized as a gain on the disposal or involuntary conversion of the asset. The gain represents compensation that exceeds the asset’s remaining book value.

Insurance proceeds are less than the carrying amount of the asset. If the insurer reimburses less than the asset’s carrying amount, the difference is recognized as a loss. The asset is removed from the books, the proceeds are recorded, and the unrecovered balance is reported as a loss on disposal or impairment.

The asset is damaged but not destroyed. If the asset remains in service and insurance proceeds are received to cover repair costs, the accounting depends on the nature of the repair. Routine repair costs are expensed as incurred, while proceeds reduce the repair expense or are recognized as a gain if they exceed the related costs.

Insurance proceeds are expected but not yet received. When a loss occurs and recovery from the insurer is probable, a receivable may be recorded for the expected recovery amount. However, recognition of the gain portion of a claim generally occurs only when realization is assured, so any excess recovery over the asset’s carrying value is typically deferred until the claim is settled.

The asset is replaced using insurance proceeds. When proceeds are used to acquire a replacement asset, the accounting for the original loss and the purchase of the new asset are treated as separate transactions. The original asset is removed and the gain or loss is recognized, while the replacement asset is recorded at its acquisition cost.

Fixed Asset Accounting FAQs

The answers to several of the more common frequently asked questions about fixed asset accounting are noted below.

How do companies determine the capitalization threshold for fixed assets?

Companies determine capitalization thresholds by considering materiality, administrative cost, and financial reporting needs. Management evaluates whether tracking smaller assets provides meaningful financial information relative to the cost of recordkeeping. Thresholds often increase as organizations grow. Companies also review thresholds periodically to ensure that they remain appropriate for operational scale and reporting objectives.

How are component assets treated in fixed asset accounting?

Component accounting separates a fixed asset into significant parts with different useful lives. Each component is recorded and depreciated separately to reflect its individual pattern of economic benefit consumption. When a component is replaced, its carrying amount is removed and the new component is capitalized, improving accuracy in depreciation and asset valuation.

How are internally constructed assets accounted for?

Companies capitalize the cost of internally constructed assets, including direct materials, direct labor, and a reasonable allocation of construction-related overhead. Interest incurred during construction may also be capitalized when the asset requires a substantial time to complete. Costs accumulate until the asset is placed in service, after which depreciation begins.

How should companies account for major inspections or overhauls of fixed assets?

Companies capitalize the cost of major inspections or overhauls when the work restores the asset’s service potential or is required for continued operation. The carrying amount of any previous inspection component is removed from the records. The new inspection cost is then depreciated over the period until the next scheduled inspection.

Related Articles

How to Account for Self-Constructed Assets