Securities accounting

/The accounting for securities depends on the classification of each security. We note in the following sections the separate accounting used for available-for-sale, held to maturity, and trading securities.

Available for Sale Securities Accounting

If a business has invested in debt securities or equity securities that are classified as available-for-sale securities, and if the equity securities have fair values that can be readily determined, the company should record their fair values in the accounting records. Further, exclude unrealized holding gains and unrealized holding losses from profit or loss, and instead record them in other comprehensive income until they are realized (that is, by selling the securities).

If a business hedges an available-for-sale security with a fair value hedge, the related holding gain or loss should be recognized in profit or loss during the period when the hedge is active.

For example, Hilltop Corporation buys $35,000 of equity securities, which it then classifies as available-for-sale. After one month, the market price of the securities reduces the investment value to $33,000. In the second month, a change in the market price increases the investment value to $36,000, after which Hilltop sells the securities. Hilltop creates the following journal entry to record the decline in value after one month:

Related AccountingTools Course

Hilltop records the effect of the increase in market value in the second month, plus the sale of the securities, with the following two journal entries:

Held to Maturity Securities Accounting

If a business has invested in debt or equity securities that it classifies as held-to-maturity, then record these investments at their amortized cost. As indicated by the name, a held-to-maturity security is one that an entity has the ability and intention to hold until its maturity date, so there is no point in adjusting its value in the accounting records prior to the maturity date.

Trading Securities Accounting

If a business invests in debt or equity securities that it classifies as trading securities, and if the fair values of the equity securities are readily determinable, then recognize their fair values on an ongoing basis and any unrealized holding gains and losses in earnings. A trading security is considered to be an investment that the holder expects to sell in the near-term for a profit.

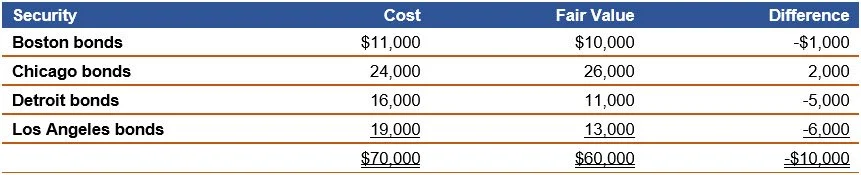

For example, the Puncture Archery Company records the following information about its trading portfolio:

Puncture records a $10,000 journal entry to recognize the reduction in fair value of its trading portfolio:

In the next period, the portfolio’s market value increases by $5,000, which Puncture recognizes with the following entry: