Horizontal analysis definition

/What is Horizontal Analysis?

Horizontal analysis is the comparison of historical financial information over a series of reporting periods. It may also apply to the ratios derived from this information. The analysis is most commonly a simple grouping of information that is sorted by period, but the numbers in each succeeding period can also be expressed as a percentage of the amount in the baseline year, with the baseline amount being listed as 100%.

How to Use Horizontal Analysis

A horizontal analysis is used to see if any numbers are unusually high or low in comparison to the information for bracketing periods, which may then trigger a detailed investigation of the reason for the difference. It can also be used to project the amounts of various line items into the future. For example, a horizontal analysis of employee benefits expense over multiple periods could be used to spot an increase in medical insurance rates, while the same analysis applied to revenues could provide a strong indication of when sales are cresting and beginning to decline.

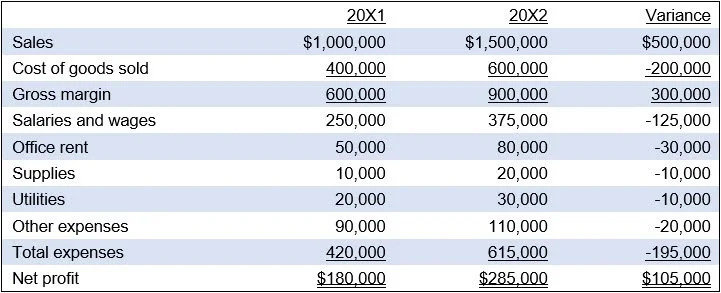

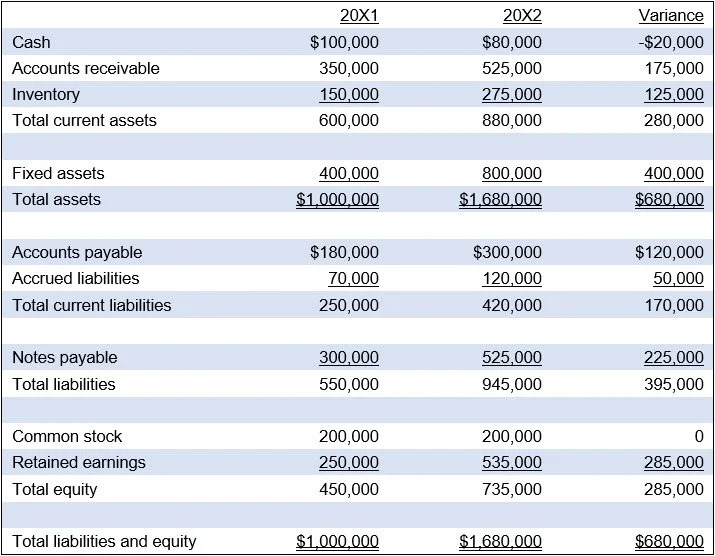

When conducting a horizontal analysis, it is useful to conduct the analysis for all of the financial statements at the same time, so that you can see the complete impact of operational results on a company's financial condition over the review period. For example, in the two examples below, the income statement analysis shows a company having an excellent second year, but the related balance sheet analysis shows that it is having trouble funding growth, given the decline in cash, increase in accounts payable, and increase in debt.

A horizontal analysis can be particularly illuminating when it includes calculations of key ratios or margins, such as the current ratio, interest coverage ratio, gross margin, and/or net profit margin. In particular, take note of any measurements included in a company’s loan covenants, since it makes sense to monitor trends in these measurements that could lead to a covenant breach. This type of presentation makes it easier to spot declining margins and/or liquidity problems early and make corrections before they can become serious concerns.

Advantages of Horizontal Analysis

There are several advantages to using horizontal analysis, which are as follows:

Trend analysis. The key advantage of using horizontal analysis is that it allows for the visual identification of anomalies from long-running trends. By presenting data on a comparative basis, changes in the data are more readily apparent.

Trend projection. The use of horizontal analysis makes it easier to project trends into the future.

Competitor analysis. Trends can be compared to those of competitors or industry averages, to see how well an organization’s performance compares with that of other entities.

Minimal experience requirement. It requires little skill to spot anomalies in a trend, while other forms of analysis may require extensive experience to discern whether the numbers in a presentation are indicative of problems.

Problems with Horizontal Analysis

A common problem with horizontal analysis is that the aggregation of information in the financial statements may have changed over time, due to ongoing changes in the chart of accounts, so that revenues, expenses, assets, or liabilities may shift between different accounts and therefore appear to cause variances when comparing account balances from one period to the next.

Horizontal analysis can be misused to report skewed findings. This can happen when the analyst modifies the number of comparison periods used to make the results appear unusually good or bad. For example, the current period's profits may appear excellent when only compared with those of the previous month, but are actually quite poor when compared to the results for the same month in the preceding year. Consistent use of comparison periods can mitigate this problem. Also, when an analysis is presented on a repetitive basis over many reporting periods, any changes in the comparison periods should be disclosed, to make readers aware of the difference.

Horizontal Analysis of the Income Statement

Horizontal analysis of the income statement is usually in a two-year format, such as the one shown below, with a variance also shown that states the difference between the two years for each line item. An alternative format is to simply add as many years as will fit on the page, without showing a variance, so that you can see general changes by account over multiple years. A third format is to include a vertical analysis of each year in the report, so that each year shows expenses as a percentage of the total revenue in that year.

Horizontal Analysis of the Balance Sheet

Horizontal analysis of the balance sheet is also usually in a two-year format, such as the one shown below, with a variance showing the difference between the two years for each line item. An alternative format is to add as many years as will fit on the page, without showing a variance, so that you can see general changes by account over multiple years. A less-used format is to include a vertical analysis of each year in the report, so that each year shows each line item as a percentage of the total assets in that year.

Impact of Reporting Standards on Horizontal Analysis

A horizontal analysis is most useful when the underlying financial information is consistently reported, based on the applicable financial reporting framework. Examples of these frameworks are generally accepted accounting principles and international financial reporting standards. Ideally, every business within an industry should apply an accounting framework in the same way, so that their reported financial information can be compared. When a business takes an unusual position in regard to reporting standards, its financial statements will not be as readily comparable to those of its competitors. The unusual application of accounting standards may be described in the footnotes that accompany a firm’s financial statements.

Horizontal Analysis FAQs

How does horizontal analysis differ from vertical analysis?

Horizontal analysis compares financial statement amounts across multiple periods to identify dollar and percentage changes over time. Vertical analysis expresses each item as a percentage of a base amount within the same period, such as sales or total assets. Horizontal analysis emphasizes trends, while vertical analysis emphasizes financial statement composition.

Can horizontal analysis be applied to nonfinancial data?

Horizontal analysis can be applied to nonfinancial data because the technique simply compares information across periods to identify trends. Metrics such as units sold, customer visits, or production levels can be analyzed in the same way as financial data. This broader application helps managers spot operational improvements or declines that support more informed decision making.

Terms Similar to Horizontal Analysis

Horizontal analysis is also known as trend analysis.

Related Articles

The Difference Between Vertical Analysis and Horizontal Analysis