Accounting for joint ventures

/How to Account for Joint Ventures

The accounting for a joint venture depends upon the level of control exercised over the venture. If a significant amount of control is exercised, the equity method of accounting must be used. In this article, we address the concept of significant influence, as well as how to account for an investment in a joint venture using the equity method.

The Impact of Significant Influence

The key element in determining whether to use the equity method is the extent of the influence exercised by an investor over a joint venture. The essential rules governing the existence of significant influence are noted below. These rules should be followed unless there is clear evidence that significant influence is not present. Conversely, significant influence can be present when voting power is lower than 20 percent, but only if it can be clearly demonstrated.

Voting power. Significant influence is presumed to be present if an investor and its subsidiaries hold at least 20 percent of the voting power of a joint venture. When reviewing this item, consider the impact of potential voting rights that are currently exercisable, such as warrants, stock options, and convertible debt. This is the overriding rule governing the existence of significant influence.

Board seat. The investor controls a seat on the joint venture’s board of directors.

Personnel. Managerial personnel are shared between the entities.

Policy making. The investor participates in the policy making processes of the joint venture. For example, the investor can affect decisions concerning distributions to shareholders.

Technical information. Essential technical information is provided by one party to the other.

Transactions. There are material transactions between the entities.

Related AccountingTools Course

The Loss of Control

An investor can lose significant control over a joint venture, despite the presence of one or more of the preceding factors. For example, a government, regulator, or bankruptcy court may gain effective control over a joint venture, thereby eliminating what had previously been the significant influence of an investor.

The Equity Method

If significant influence is present, an investor should account for its investment in an joint venture using the equity method. In essence, the equity method mandates that the initial investment be recorded at cost, after which the investment is adjusted for the actual performance of the joint venture. The following calculation illustrates how the equity method operates:

+ Initial investment recorded at cost

+/- Investor's share of joint venture profit or loss

- Distributions received from the joint venture

= Ending investment in joint venture

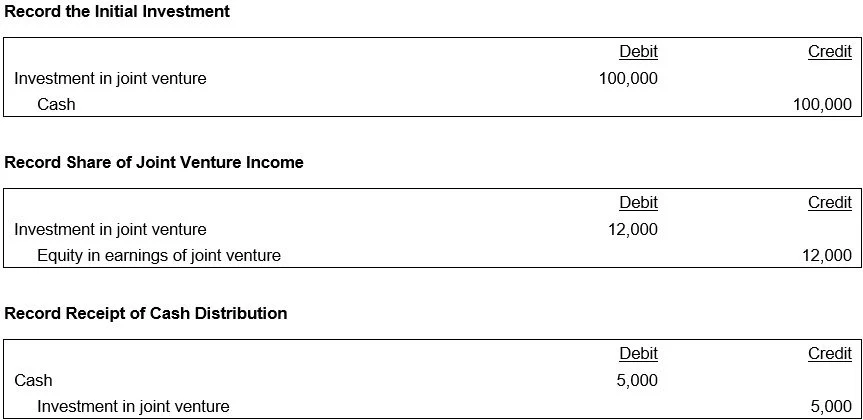

For example, an investor pays $100,000 for its interest in a joint venture, is entitled to 30% of its income, the venture reports $40,000 of net income, and the investor receives a $5,000 cash distribution. The related journal entries are as follows:

After these entries have been made, the investor’s total investment balance in the venture is $107,000.

The investor’s share of the joint venture’s profits and losses are recorded within the income statement of the investor. Also, if the joint venture records changes in its other comprehensive income, the investor should record its share of these items within other comprehensive income, as well.

Accounting for Joint Venture Losses

If a joint venture reports a large loss, or a series of losses, it is possible that recording the investor’s share of these losses will result in a substantial decline of the investor’s recorded investment in the joint venture. If so, the investor stops using the equity method when its investment reaches zero. If an investor’s investment in an joint venture has been written down to zero, but it has other investments in the joint venture (such as loans), the investor should continue to recognize its share of any additional joint venture losses and offset them against the other investments, in sequence of the seniority of those investments (with offsets against the most junior items first). If the joint venture later begins to report profits again, the investor does not resume use of the equity method until such time as its share of joint venture profits have offset all joint venture losses that were not recognized during the period when use of the equity method was suspended.

Joint Venture FAQs

What disclosures are required for joint ventures?

Joint venture disclosures typically include the nature of the joint arrangement, ownership interests, and the basis for joint control. Entities also disclose summarized financial information, including assets, liabilities, revenues, and profit or loss. Commitments, contingencies, and any guarantees related to the joint venture must be disclosed to explain risk exposure.