Accounting equation definition

/What is the Accounting Equation?

The accounting equation shows the relationship between assets, liabilities and equity. It is the basis upon which the double entry accounting system is constructed. Business transactions must be recorded in accordance with the accounting equation, to ensure that each part of a journal entry is correct. In essence, the accounting equation is as follows:

Assets = Liabilities + Shareholders' Equity

The asset, liability, and shareholders’ equity portions of the accounting equation are explained further below, noting the different accounts that may be included in each one. You can see this relationship between assets, liabilities, and shareholders' equity in the balance sheet, where the total of all assets always equals the sum of the liabilities and shareholders' equity sections.

Assets in the Accounting Equation

The assets in the accounting equation are the resources that a company has available for its use, such as cash, accounts receivable, fixed assets, and inventory. Accounts receivable include all amounts billed to customers on credit that relate to the sale of goods or services. Inventory includes all raw materials, work-in-process, finished goods, merchandise, and consigned goods being offered for sale by third parties.

A company pays for assets by either incurring liabilities (which is the Liabilities part of the accounting equation) or by obtaining funding from investors (which is the Shareholders' Equity part of the equation). Thus, you have resources with offsetting claims against those resources, either from creditors or investors. All three components of the accounting equation appear in the balance sheet, which reveals the financial position of a business at any given point in time.

Liabilities in the Accounting Equation

The Liabilities part of the equation is usually comprised of accounts payable that are owed to suppliers, a variety of accrued liabilities, such as sales taxes and income taxes, and debt payable to lenders. Accounts payable include all goods and services billed to the company by suppliers that have not yet been paid. Accrued liabilities are for goods and services that have been provided to the company, but for which no supplier invoice has yet been received.

Shareholders’ Equity in the Accounting Equation

The Shareholders' Equity part of the equation is more complex than simply being the amount paid to the company by investors. It is actually their initial investment, plus any subsequent gains, minus any subsequent losses, minus any dividends or other withdrawals paid to the investors. The shareholders’ equity section tends to increase for larger businesses, since lenders want to see a large investment in a business before they will lend significant funds to an organization.

Why is the Accounting Equation Important?

The reason why the accounting equation is so important is that it is always true - and it forms the basis for all accounting transactions in a double entry system. At a general level, this means that whenever there is a recordable transaction, the choices for recording it all involve keeping the accounting equation in balance. The accounting equation concept is built into all accounting software packages, so that all transactions that do not meet the requirements of the equation are automatically rejected.

Limitations of the Accounting Equation

The accounting equation is only designed to provide the underlying structure for how the balance sheet is formulated. As long as an organization follows the accounting equation, it can report any type of transaction, even if it is fraudulent. In short, the accounting equation does not ensure that reported financial information is correct - only that it follows certain rules regarding how information is to be recorded within an accounting system.

In addition, the accounting equation only provides the underlying structure for how a balance sheet is devised. Any user of a balance sheet must then evaluate the resulting information to decide whether a business is sufficiently liquid and is being operated in a fiscally sound manner.

Example of the Accounting Equation

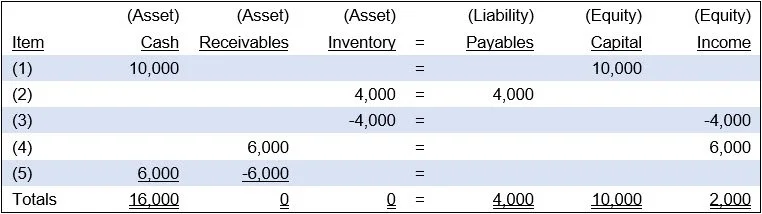

ABC International engages in the following series of transactions:

ABC sell shares to an investor for $10,000. This increases the cash (asset) account as well as the capital (equity) account.

ABC buys $4,000 of inventory from a supplier. This increases the inventory (asset) account as well as the payables (liability) account.

ABC sells the inventory for $6,000. This decreases the inventory (asset) account and creates a cost of goods sold expense that appears as a decrease in the income (equity) account.

The sale of ABC's inventory also creates a sale and offsetting receivable. This increases the receivables (asset) account by $6,000 and increases the income (equity) account by $6,000.

ABC collects cash from the customer to which it sold the inventory. This increases the cash (asset) account by $6,000 and decreases the receivables (asset) account by $6,000.

These transactions appear in the following table:

Note how every transaction is balanced within the accounting equation - either because there are changes on both sides of the equation, or because a transaction cancels itself out on one side of the equation (as was the case when the receivable was converted to cash).

Recording accounting transactions with the accounting equation means that you use debits and credits to record every transaction, which is known as double-entry bookkeeping.

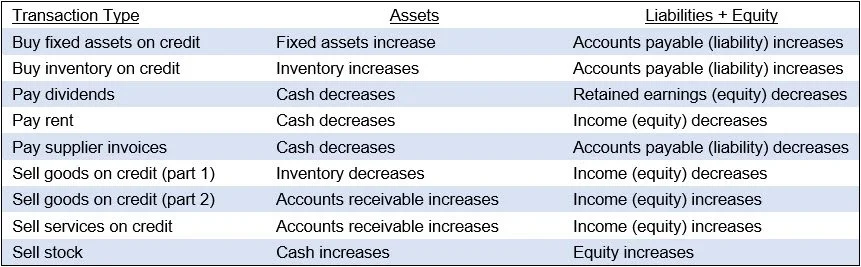

Sample Accounting Equation Transactions

The following table shows how a number of typical accounting transactions are recorded within the framework of the accounting equation:

Examples of Accounting Equation Transactions

We note below several examples of each of the preceding transactions, where we show how they comply with the accounting equation:

Buy fixed assets on credit. ABC Company buys a machine on credit for $10,000. This increases the fixed assets (Asset) account and increases the accounts payable (Liability) account. Thus, the asset and liability sides of the transaction are equal.

Buy inventory on credit. ABC Company buys raw materials on credit for $5,000. This increases the inventory (Asset) account and increases the accounts payable (Liability) account. Thus, the asset and liability sides of the transaction are equal.

Pay dividends. ABC Company pays $25,000 in dividends. This reduces the cash (Asset) account and reduces the retained earnings (Equity) account. Thus, the asset and equity sides of the transaction are equal.

Pay rent. ABC Company pays $4,000 in rent. This reduces the cash (Asset) account and reduces the accounts payable (Liabilities) account. Thus, the asset and liability sides of the transaction are equal.

Pay supplier invoices. ABC Company pays $29,000 on existing supplier invoices. This reduces the cash (Asset) account by $29,000 and reduces the accounts payable (Liability) account. Thus, the asset and liability sides of the transaction are equal.

Sell goods on credit. ABC Company sell goods for $55,000 on credit. This increases the accounts receivable (Asset) account by $55,000, and increases the revenue (Equity) account. Thus, the asset and equity sides of the transaction are equal.

Sell stock. ABC Company sells $120,000 of its shares to investors. This increases the cash account (Asset) by $120,000, and increases the capital stock (Equity) account. Thus, the asset and equity sides of the transaction are equal.

Additional Accounting Equation Issues

What if you print the balance sheet and the total of all assets do not match the total of all liabilities and shareholders' equity? There may be one of three underlying causes of this problem, which are noted below:

Rounding error. If your accounting software is rounding to the nearest dollar or thousand dollars, the rounding function may result in a presentation that appears to be unbalanced. This is merely a rounding issue - there is not actually a flaw in the underlying accounting equation.

Unbalanced starting numbers. If you have just started using the software, you may have entered beginning balances for the various accounts that do not balance under the accounting equation. The accounting software should flag this problem when you are entering the beginning balances, and require you to correct the problem.

Unbalanced transactions. You may have made a journal entry where the debits do not match the credits. This should be impossible if you are using accounting software, but is entirely possible (if not likely) if you are recording accounting transactions manually. In the latter case, the only way to correct the issue is to review all entries made to date, to find the unbalanced entry.

What is the Expanded Accounting Equation?

The expanded accounting equation provides an enhanced level of detail regarding the standard accounting equation. The expanded accounting equation reveals all of the components of the shareholders' equity part of the accounting equation. The expanded equation is:

Assets = Liabilities + (Paid in Capital - Dividends - Treasury Stock + Revenue - Expenses)

This additional level of detail shows how profits and losses from the income statement appear in the shareholders' equity section of the balance sheet, as well as how cash outflows to pay for dividends and the repurchase of stock will reduce the amount of shareholders' equity.

The concept of the expanded accounting equation does not extend to the asset and liability sides of the accounting equation, since those elements are not directly altered by changes in the income statement. Thus, there is no need to show additional detail for the asset or liability sides of the accounting equation.

Accounting Equation for Nonprofit Entities

The equation differs for a nonprofit entity, since a nonprofit does not record any shareholders' equity. Instead, the equation for a nonprofit is as follows:

Assets = Liabilities + Net Assets

The net assets part of this equation is comprised of unrestricted and restricted net assets.

Terms Similar to Accounting Equation

The accounting equation is also known as the balance sheet equation or the basic accounting equation.