Payroll journal entries

/What are Payroll Journal Entries?

Payroll journal entries are used to record the compensation paid to employees, as well as the associated tax and other withholdings. These entries are then incorporated into an entity's financial statements through the general ledger. The key types of payroll journal entries are noted below.

Initial Payroll Entry

The primary payroll journal entry is for the initial recordation of a payroll. This entry records the gross wages earned by employees, as well as all withholdings from their pay, and any additional taxes owed to the government by the company.

Accrued Wages Entry

There may be an accrued wages entry that is recorded at the end of each accounting period, and which is intended to record the amount of wages owed to employees but not yet paid. This entry is then reversed in the following accounting period, so that the initial recordation entry can take its place. This entry may be avoided if the amount is immaterial.

Manual Payments Entry

A company may occasionally print manual paychecks to employees, either because of pay adjustments or employment terminations.

All of these journal entries are noted below.

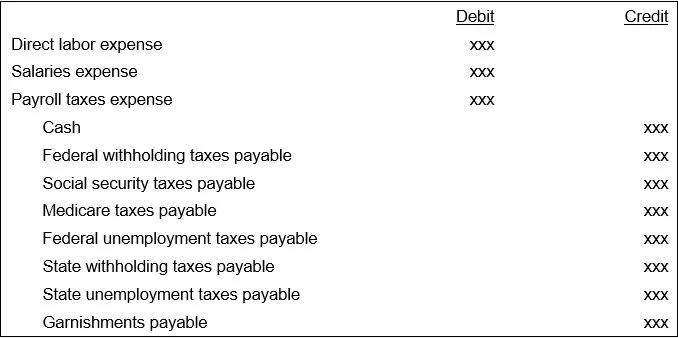

Primary Payroll Journal Entry

The primary journal entry for payroll is the summary-level entry that is compiled from the payroll register, and which is recorded in either the payroll journal or the general ledger. This entry usually includes debits for the direct labor expense, salaries, and the company's portion of payroll taxes. There will also be credits to a number of accounts, each one detailing the liability for payroll taxes that have not been paid, as well as for the amount of cash already paid to employees for their net pay. The basic entry (assuming no further breakdown of debits by individual department) is:

There may be a number of additional employee deductions to include in this journal entry. For example, there may be deductions for 401(k) pension plans, health insurance, life insurance, vision insurance, and for the repayment of advances.

When you later pay the withheld taxes and company portion of payroll taxes to the IRS, you then use the following entry to reduce the balance in the cash account, and eliminate the balances in the liability accounts:

Accrued Payroll Journal Entry

It is quite common to have some amount of unpaid wages at the end of an accounting period, so you should accrue this expense (if it is material). The accrual entry, as shown next, is simpler than the comprehensive payroll entry already shown, because you typically clump all payroll taxes into a single expense account and offsetting liability account. After recording this entry, reverse it at the beginning of the following accounting period, and then record the actual payroll expense (as just described under the "Primary Payroll Journal Entry" section whenever it occurs.

Manual Paycheck Entry

It is quite common to create a manual check, either because an employee was short-paid in the preceding payroll, or because the company is laying off or firing an employee, and so is obligated to pay that person before the next regularly scheduled payroll. This check may be paid through the corporate accounts payable bank account, rather than its payroll account, so you may need to make this entry through the accounts payable system. If you are recording it directly into the general ledger or the payroll journal, then use the same line items already noted for the primary payroll journal entry.

The volume of manual paycheck entries can be reduced by continual attention to the underlying causes of transaction errors, so there are fewer payroll errors to be rectified with a manual paycheck.

Related Articles

How to Account for Unpaid Wages

How to Calculate Accrued Vacation Pay