Cost Accounting Explained

/What is Cost Accounting?

Cost accounting examines the cost structure of a business. It does so by collecting information about the costs incurred by a company's activities, assigning selected costs to products and services and other cost objects, and evaluating the efficiency of cost usage. Cost accounting is mostly concerned with developing an understanding of where a company earns and loses money, and providing input into decisions to generate profits in the future.

Related AccountingTools Courses

Cost Accounting Methods

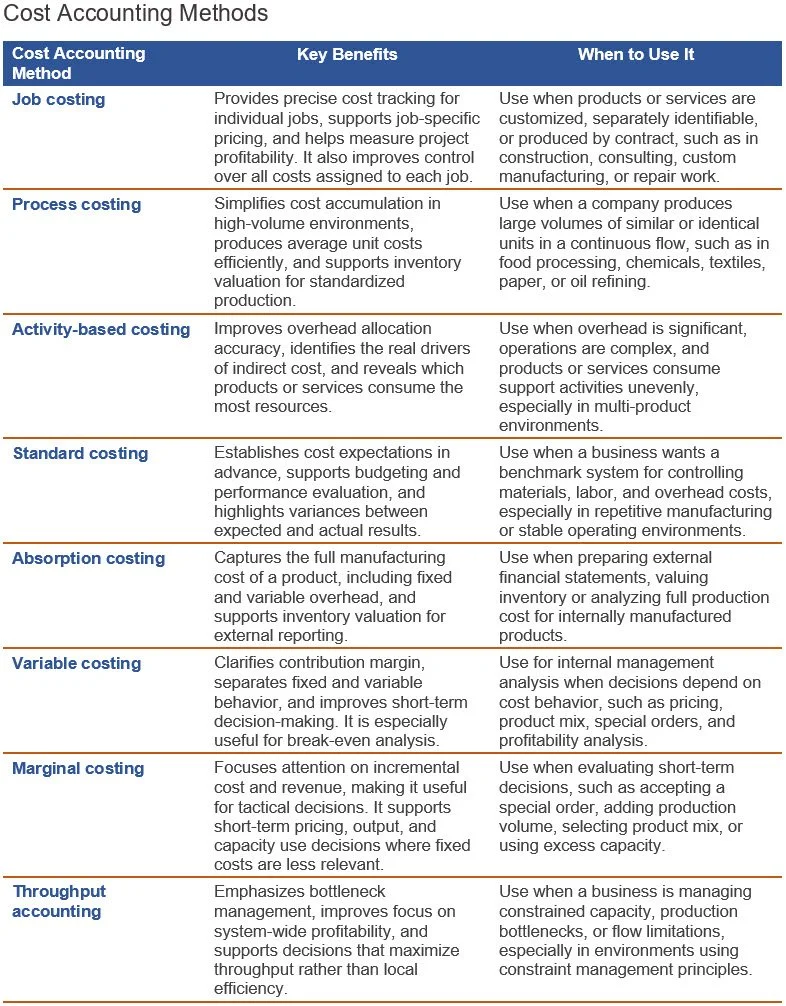

Cost accounting includes several methods, each designed to measure costs for a different operating environment or management objective. Some methods focus on assigning historical costs, while others emphasize planning, control, pricing, or strategic decision-making.

Job costing tracks the direct materials, direct labor, and allocated overhead associated with a specific job, contract, or batch. It works best when products or services are customized and separately identifiable. Managers use it to measure job profitability, support pricing decisions, and control project-specific spending.

Process costing accumulates costs by department, process, or production stage, then averages those costs over large numbers of similar units. It is most useful in continuous-production environments. This method helps organizations value inventory, measure unit cost, and evaluate production efficiency across standardized operations.

Activity-based costing (ABC) assigns overhead costs based on the activities that actually consume resources, such as setups, inspections, or material handling. It improves costing accuracy where overhead is significant and products differ in complexity. Managers use ABC to identify cost drivers and refine pricing and process decisions.

Standard costing uses predetermined estimates for materials, labor, and overhead instead of relying solely on actual costs. Actual results are then compared to standards through variance analysis. This method supports budgeting, performance evaluation, and cost control by highlighting where operations differ from expected efficiency levels.

Absorption costing assigns all manufacturing costs to products, including direct materials, direct labor, variable overhead, and fixed overhead. Because fixed manufacturing overhead becomes part of inventory cost, this method is generally required for external financial reporting. It is useful for full product costing and inventory valuation.

Variable costing assigns only variable manufacturing costs to products, while fixed manufacturing overhead is charged directly to expense in the period incurred. This approach is especially useful for internal analysis because it clarifies contribution margin behavior. Managers often use it for break-even analysis and short-term planning.

Marginal costing focuses on the additional cost incurred to produce one more unit, which is usually the variable cost of that unit. It is highly useful for short-term decisions involving pricing, special orders, product mix, and capacity utilization where incremental cost and incremental revenue are central.

Throughput accounting emphasizes the rate at which a business generates revenue through its constrained resource, rather than allocating costs broadly across products. Direct materials are often treated as the main truly variable cost. This approach supports decisions aimed at maximizing system-wide flow and reducing bottlenecks.

Together, these methods give management different lenses for measuring cost behavior, valuing inventory, improving efficiency, and making better operational and strategic decisions. The following comparison table shows the benefits of each method and where it should be used.

Types of Cost Accounting Activities

Key cost accounting activities include the following:

Defining costs as direct materials, direct labor, fixed overhead, variable overhead, and period costs

Assisting the engineering and procurement departments in generating standard costs, if a company uses a standard costing system

Using an allocation methodology to assign all costs except period costs to products and services and other cost objects

Defining the transfer prices at which components and parts are sold from one subsidiary of a parent company to another subsidiary

Examining costs incurred in relation to activities conducted, to see if the company is using its resources effectively

Highlighting any changes in the trend of various costs incurred

Analyzing costs that will change as the result of a business decision

Evaluating the need for capital expenditures

Building a budget model that forecasts changes in costs based on expected activity levels

Understanding how costs change in relation to changes in unit volume

Determining whether costs can be reduced

Providing cost reports to management, so they can better operate the business

Participating in the calculation of costs that will be required to manufacture a new product design

Analyzing the system of production to understand where bottlenecks are positioned, and how they impact the throughput generated by the entire manufacturing system

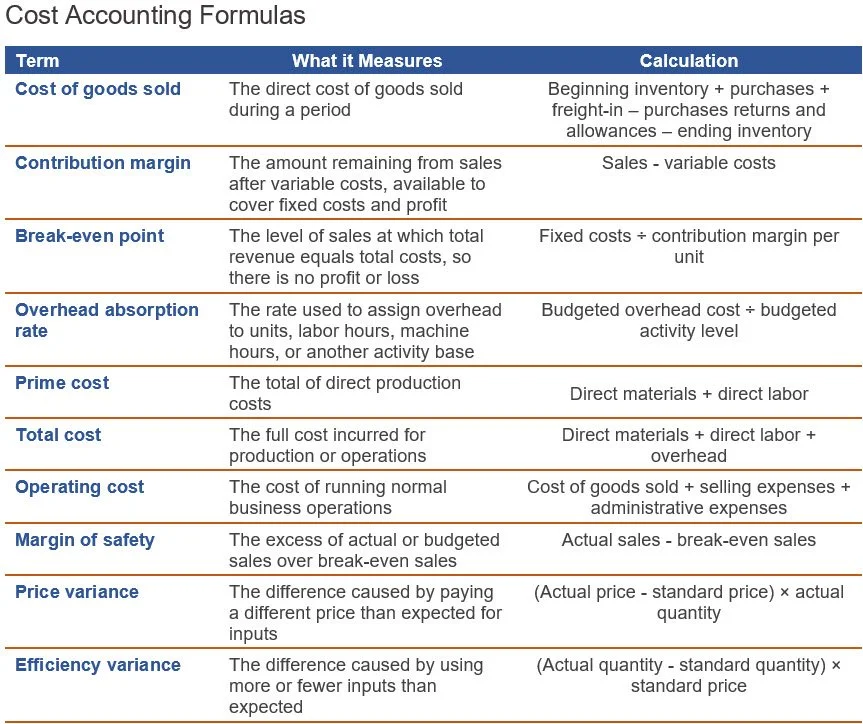

Cost Accounting Formulas

There are dozens of formulas and ratios that can be useful for a cost accounting analysis, depending on the circumstances. Several of the more common formulas are described in the following table, including what is being measured and how they are calculated.

Cost Accounting Principles

Cost accounting principles are the foundational concepts used to measure, assign, analyze, and control costs so that management can make better decisions. Unlike financial accounting, which is aimed primarily at external reporting, cost accounting is intended mainly for internal use. Its principles focus on identifying how resources are consumed, how costs behave, and how those costs should be assigned to products, services, departments, or activities. These principles are as follows:

Cost identification. A business must first determine what costs have been incurred and what they relate to. This involves distinguishing among materials, labor, and overhead, as well as separating product costs from period costs. Product costs are attached to goods or services produced, while period costs are charged to expense in the period incurred.

Cost classification. Costs may be classified in several ways depending on the purpose of the analysis. They can be direct or indirect, fixed or variable, controllable or uncontrollable, relevant or irrelevant, and joint or common. These classifications are not merely descriptive. They help management decide how costs should be traced, allocated, budgeted, or considered in decision-making.

Cost tracing and allocation. Direct costs should be traced to a cost object whenever feasible, because tracing produces the most accurate measure of cost. Indirect costs cannot usually be traced directly, so they must be allocated using a logical basis, such as labor hours, machine hours, square footage, or activity drivers. The principle here is that allocation should reflect a reasonable relationship between the cost incurred and the cost object receiving the charge.

Cause-and-effect costing. Whenever possible, costs should be assigned based on the actual factors that drive them. This principle is especially important in more advanced systems such as activity-based costing, where costs are linked first to activities and then to products, services, or customers based on the actual consumption of those activities. The closer the assignment reflects cost causation, the more useful the resulting information.

Cost behavior analysis. Managers need to understand how costs respond to changes in activity levels. Some costs vary directly with production volume, some remain fixed within a relevant range, and others are mixed or step-based. Understanding this behavior is crucial for budgeting, break-even analysis, contribution margin analysis, and short-term planning.

Matching costs with operations. Costs should be recognized and analyzed in a way that corresponds with the operations or outputs they support. In internal reporting, this helps managers evaluate profitability more accurately by aligning costs with the products, services, or departments responsible for them.

Relevance for decision-making. Not all costs matter in every decision. Sunk costs, for example, are generally irrelevant because they cannot be changed by future actions. Relevant costs are those that differ among alternatives and therefore affect the outcome of a decision. Cost accounting emphasizes isolating the costs and revenues that truly matter in decisions such as pricing, outsourcing, discontinuing a product line, or accepting a special order.

Consistency in measurement methods. Once a company adopts a costing approach, such as a method for overhead allocation or inventory costing, it should apply that method consistently enough to allow meaningful comparisons over time. At the same time, cost accounting remains flexible, since internal usefulness may justify refinement when operations change.

Timeliness and practicality. Cost information does not need to be perfectly precise to be useful, but it must be available in time to support management action. This means cost accounting often balances precision against speed and cost-benefit considerations. A highly refined costing model may be less useful if it is too expensive or slow to maintain.

Control and performance evaluation. Costs are not just measured; they are monitored against standards, budgets, or expectations. Variance analysis, responsibility accounting, and standard costing all reflect the idea that cost information should help management assess efficiency, identify problems, and improve operations.

In summary, cost accounting principles revolve around identifying costs clearly, classifying them meaningfully, assigning them rationally, analyzing their behavior, and using them in a way that improves planning, control, and decision-making. The purpose is not simply to record spending, but to convert cost data into useful managerial insight.

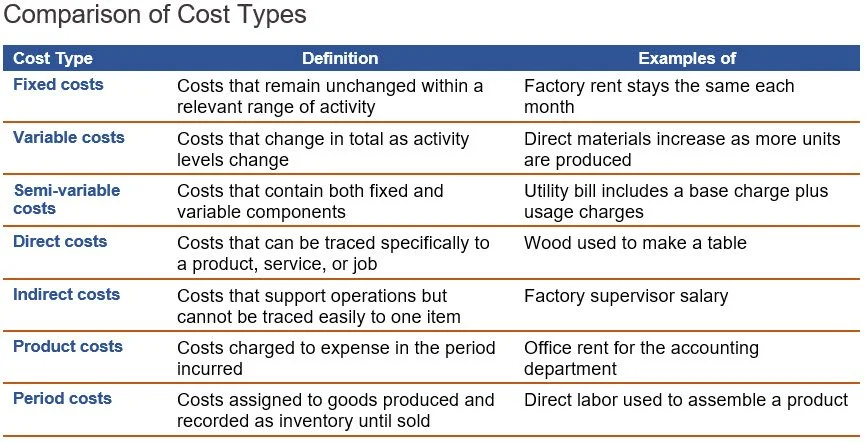

Types of Costs in Cost Accounting

Cost accounting classifies costs in several ways so managers can plan operations, price products, control spending, and evaluate performance. Some classifications focus on how costs behave as activity changes, while others focus on whether costs can be traced to products or must be expensed in the current period.

Fixed costs. These costs remain constant in total within a relevant range of activity, even when production volume changes. Examples include rent, salaried supervision, property taxes, and insurance. Although total fixed cost stays the same in the short term, the fixed cost per unit declines as more units are produced and rises when output falls.

Variable costs. These costs change in direct proportion to the level of activity or production volume. Total direct materials, sales commissions, and piece-rate labor are common examples. On a per-unit basis, variable costs usually remain constant, assuming stable pricing and efficiency. These costs are especially important for contribution margin analysis, budgeting, and short-term decision-making.

Semi-variable costs. These costs, also called mixed costs, contain both fixed and variable components. A utility bill is a common example, because it may include a base monthly charge plus usage-based charges. These costs do not move in perfect proportion to activity. Managers often separate them into fixed and variable elements for forecasting, budgeting, and cost behavior analysis.

Direct costs. These costs can be traced specifically and economically to a cost object, such as a product, job, service, or department. Direct materials and direct labor are the most common examples in manufacturing. Because they are clearly associated with a specific output, direct costs are useful for product costing, pricing, profitability analysis, and operational control.

Indirect costs. These costs cannot be traced conveniently or economically to a single cost object, so they must be allocated using a reasonable method. Examples include factory rent, maintenance, production supervision, and shared utilities. These costs support overall operations rather than one specific unit, making allocation methods important for accurate product costing and performance evaluation.

Period costs. These costs are charged to expense in the period incurred rather than being attached to inventory. Selling, general, and administrative expenses are the main examples, including office salaries, advertising, and corporate rent. These costs relate more to time and business operations than to production, so they appear directly on the income statement.

Product costs. These costs are the costs assigned to goods produced or purchased for resale. In manufacturing, they usually include direct materials, direct labor, and manufacturing overhead. These costs are first recorded as inventory on the balance sheet and later recognized as cost of goods sold when the related products are sold.

These cost categories give managers different ways to view the same spending, depending on the purpose of the analysis. By understanding how costs behave, how they are traced, and when they are recognized, a company can make better decisions about pricing, budgeting, production, and profitability. A comparison of these costs appears in the following exhibit.

Cost Accounting FAQs

Can cost accounting be used in service industries?

Cost accounting can be effectively used in service industries to track and control costs related to labor, overhead, and service delivery. Unlike manufacturing, service industries focus more on allocating indirect costs, such as salaries and facility expenses, to specific services or clients. Techniques like activity-based costing are especially useful for accurately assigning costs in service environments.

What is the difference between cost accounting and financial accounting?

Cost accounting is a source of information for the financial statements, especially in regard to the valuation of inventory. However, it is not directly involved in the generation of financial statements. Cost accounting is designed to assist management in how a business is run, while financial accounting is designed to provide information about a business to financial statement users.

What is the difference between job costing and process costing?

Job costing accumulates costs for a specific job, contract, batch, or customer order, making it suitable for customized work. Process costing accumulates costs by department or production process and averages them across identical units, making it appropriate for continuous, standardized production where individual units are not separately distinguishable.

Why is variance analysis not enough on its own?

Variance analysis identifies differences between actual and expected results, but it does not explain their underlying causes or business significance. A variance may reflect inefficiency, poor planning, changing conditions, or a deliberate management decision. Managers must interpret variances in context before deciding whether corrective action is needed.

Related Articles

The Advantages of Cost Accounting

The Difference Between Cost Accounting and Financial Accounting