Lease Accounting Explained

/What is a Lease?

A lease is a contractual agreement in which one party (the lessee) obtains the right to use an asset owned by another party (the lessor) for a specified period in exchange for periodic payments. Leases are commonly used for property, equipment, or vehicles and can be structured as operating or finance leases. The lessee typically gains access to the asset without having to purchase it outright, conserving capital while still meeting operational needs. Depending on the lease terms, the lessee may also be responsible for maintenance, insurance, or even the option to purchase the asset at the end of the lease.

What is Lease Accounting?

Lease accounting is the process of recording and reporting lease transactions in an organization's financial statements in accordance with applicable accounting standards, such as ASC 842 or IFRS 16. It requires lessees to recognize most leases on the balance sheet by recording a right-of-use asset and a corresponding lease liability. The accounting treatment varies based on whether the lease is classified as a finance lease or an operating lease, affecting how expenses are recognized in the income statement. For lessors, lease accounting involves determining whether a lease is a sales-type, direct financing, or operating lease, which dictates how revenue and assets are reported.

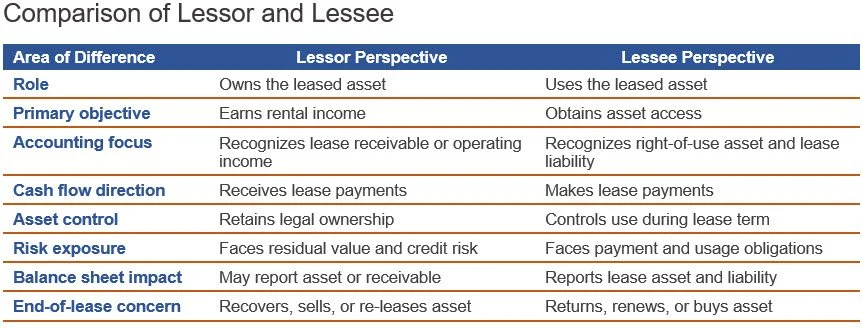

Lessee vs. Lessor

In a lease arrangement, the lessee is the party that obtains the right to use an asset owned by another party for a specified period in exchange for periodic payments. The lessee does not own the asset but gains control over its use under agreed-upon terms, such as duration, payment amounts, and maintenance responsibilities. The lessor, on the other hand, is the owner of the asset who grants the usage rights to the lessee while retaining legal ownership. The lessor receives lease payments and may impose conditions to protect the asset’s value and ensure proper use. This relationship allows the lessee to access necessary assets without a large upfront investment, while providing the lessor with a steady income stream. The key differences between the lessor and lessee are noted in the following exhibit.

Lease Classifications for a Lessee

The choices for a lessee are that a lease can be designated as either a finance lease or an operating lease. A lessee should classify a lease as a finance lease when any of the following criteria are met:

Ownership of the underlying asset is shifted to the lessee by the end of the lease term.

The lessee has a purchase option to buy the leased asset, and is reasonably certain to use it.

The lease term covers the major part of the underlying asset’s remaining economic life. This is considered to be 75% or more of the remaining economic life of the underlying asset (this threshold is commonly used as a practical guideline, but ASC 842 uses principles-based wording, such as “major part”).

The present value of the sum of all lease payments and any lessee-guaranteed residual value matches or exceeds the fair value of the underlying asset.

The asset is so specialized that it has no alternative use for the lessor following the lease term.

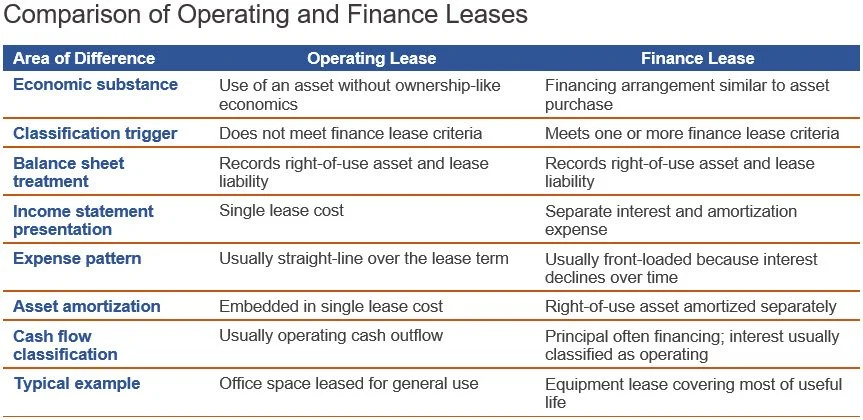

When none of the preceding criteria are met, the lessee must classify a lease as an operating lease. An operating lease is the rental of an asset from a lessor, but not under terms that transfer ownership of the asset to the lessee. During the rental period, the lessee typically has unrestricted use of the asset, but is responsible for the condition of the asset at the end of the lease, when it is returned to the lessor. The key differences between an operating lease and a finance lease are noted in the following exhibit.

Lease Classifications for a Lessor

The choices for a lessor are that a lease can be designated as a sales-type lease, direct finance lease, or operating lease. If all of the preceding conditions just noted for a lessee’s finance lease are met by a lease, then the lessor designates it as a sales-type lease. If this is not the case, then the lessor has a choice of designating a lease as either a direct financing lease or an operating lease. The lessor should designate any remaining lease as a direct financing lease when both of the following criteria are met:

The present value of the lease payments and any residual asset value that is guaranteed by the lessee or any other party matches or exceeds substantially all of the fair value of the underlying asset. In this context, “substantially” means 90% or more of the fair value of the underlying asset.

The lessor will probably collect the lease payments, as well as any additional amount needed to satisfy the residual value guarantee.

When none of these additional criteria are met, the lessor classifies a lease as an operating lease. A summarized comparison of these lease types appears in the following exhibit.

Lessee Accounting for a Lease

As of the commencement date of a lease, the lessee measures the liability and the right-of-use asset associated with the lease. These measurements are derived as follows:

Lease liability. The present value of the lease payments, discounted at the discount rate for the lease. This rate is the rate implicit in the lease when that rate is readily determinable. If not, the lessee instead uses its incremental borrowing rate.

Right-of-use asset. The initial amount of the lease liability, plus any lease payments made to the lessor before the lease commencement date, plus any initial direct costs incurred, minus any lease incentives received.

When a lessee has designated a lease as a finance lease, it should recognize the following over the term of the lease:

The ongoing amortization of the right-of-use asset

The ongoing amortization of the interest on the lease liability

Any variable lease payments that are not included in the lease liability

Any impairment of the right-of-use asset

When a lessee has designated a lease as an operating lease, the lessee should recognize the following over the term of the lease:

A lease cost in each period, where the total cost of the lease is allocated over the lease term on a straight-line basis.

Any variable lease payments that are not included in the lease liability

Any impairment of the right-of-use asset

Lessor Accounting for a Lease

In a sales-type lease, the lessor is assumed to be selling a product to the lessee, which calls for the recognition of a profit or loss on the sale. Consequently, this results in the following accounting at the commencement date of the lease:

The lessor derecognizes the underlying asset, since it is assumed to have been sold to the lessee.

The lessor recognizes a net investment in the lease. This investment includes the following:

The present value of lease payments not yet received

The present value of the guaranteed amount of the underlying asset’s residual value at the end of the lease term

The present value of the unguaranteed amount of the underlying asset’s residual value at the end of the lease term

The lessor recognizes any selling profit or loss caused by the lease.

The lessor recognizes any initial direct costs as an expense, if there is a difference between the carrying amount of the underlying asset and its fair value. If the fair value of the underlying asset is instead equal to its carrying amount, then defer the initial direct costs and include them in the measurement of the lessor’s investment in the lease.

In addition, the lessor must account for the following items subsequent to the commencement date of the lease:

The ongoing amount of interest earned on the net investment in the lease.

If there are any variable lease payments that were not included in the net investment in the lease, record them in profit or loss in the same reporting period as the events that triggered the payments.

Recognize any impairment of the net investment in the lease.

Adjust the balance of the net investment in the lease by adding interest income and subtracting any lease payments collected during the period.

At the commencement date of a direct financing lease, the lessor engages in the following activities:

Recognize the net investment in the lease. This includes the selling profit and any initial direct costs for which recognition is deferred.

Recognize a selling loss caused by the lease arrangement, if this has occurred

Derecognize the underlying asset

In addition, the lessor must account for the following items subsequent to the commencement date of the lease:

Record the ongoing amount of interest earned on the net investment in the lease.

If there are any variable lease payments that were not included in the net investment in the lease, record them in profit or loss in the same reporting period as the events that triggered the payments.

Record any impairment of the net investment in the lease.

Adjust the balance of the net investment in the lease by adding interest income and subtracting any lease payments collected during the period.

Lease Accounting Example

This example shows the basic lease accounting entries required for an operating lease. We assume that a company enters into a three-year equipment lease with the following terms: 36-month term, $2,000 monthly lease payments, a 6% annual discount rate, and a $65,738 present value of lease payments.

At lease commencement, the lessee records a right-of-use asset and a lease liability. In this example, there are no prepaid payments, initial direct costs, or lease incentives, so the right-of-use asset equals the lease liability.

This entry records the lessee’s right to use the leased equipment and the related obligation to make future lease payments.

For an operating lease, the lessee generally recognizes a single lease cost on a straight-line basis. Since the monthly payment is $2,000, the monthly lease expense is also $2,000. In the first month, interest on the lease liability is calculated as follows:

$65,738 × 0.5% = $329

The difference between the total lease expense and the interest amount reduces the right-of-use asset:

$2,000 - $329 = $1,671

The monthly expense entry is:

The payment entry is:

After these entries, the lease liability is reduced by the difference between the cash payment and the interest accretion:

$2,000 - $329 = $1,671

Common Lease Accounting Errors

Lease accounting errors often arise when companies identify leases too narrowly, apply incomplete assumptions, or fail to update accounting records after contract changes. The following issues can distort assets, liabilities, expenses, and disclosures under ASC 842:

Omitting embedded leases from service contracts. A service contract may contain an embedded lease when the customer controls the use of an identified asset, such as dedicated equipment, vehicles, or servers. If management overlooks this feature, the company may omit a right-of-use asset and lease liability from the balance sheet.

Using the wrong discount rate. Lease liabilities depend heavily on the discount rate. Errors occur when a company uses a generic borrowing rate, an outdated rate, or the lessor’s implicit rate without sufficient support. An incorrect rate can materially overstate or understate both the lease liability and related right-of-use asset.

Ignoring renewal options that are reasonably certain to be exercised. The lease term should include renewal periods when exercise is reasonably certain. Companies may ignore renewal options to reduce the recorded liability. This error is especially likely when the leased asset is specialized, difficult to replace, or central to ongoing operations.

Failing to separate lease and non-lease components. Contracts often bundle asset use with maintenance, utilities, support, or other services. If these components are not separated properly, the company may mismeasure the lease liability. The error can also distort expense classification and reduce comparability across contracts.

Misclassifying finance leases as operating leases. A finance lease transfers substantially all economic benefits of the asset to the lessee. Misclassification may occur when management overlooks purchase options, lease terms covering most of the asset’s life, or payments representing substantially all fair value. This affects expense pattern and presentation.

Not remeasuring leases after modifications. Lease accounting should be revisited when payment terms, lease duration, asset scope, or contract rights change. If a company treats modifications as mere administrative changes, it may leave obsolete assets and liabilities on the books and fail to recognize the revised economics of the arrangement.

Treating lease incentives incorrectly. Lease incentives, such as tenant improvement allowances, rent holidays, or lessor reimbursements, generally reduce the measurement of the right-of-use asset. Errors occur when incentives are recorded as immediate income, ignored, or netted against the wrong account, causing misstated assets or expenses.

Weak lease data controls. Lease accounting depends on complete and accurate contract data. Weak controls over contract entry, renewal tracking, payment changes, and modification approvals can cause recurring errors. A decentralized lease process increases the risk that accounting records do not reflect the current lease population.

In summary, lease accounting errors usually stem from incomplete contract analysis, weak data capture, or failure to reassess assumptions over time. Better controls, periodic lease reviews, centralized contract tracking, and documented classification judgments can reduce these errors and improve financial reporting reliability.

Lease Accounting FAQs

What is the difference between a lessor and a lessee?

A lessee obtains the right to use an asset in exchange for lease payments and records a right-of-use asset and lease liability. A lessor owns or controls the asset and grants usage rights, recognizing lease income or a lease receivable depending on classification.

How are lease modifications accounted for?

Lease modifications are accounted for as separate contracts when they add a right of use and the added payments reflect the standalone price. Otherwise, the lessee remeasures the lease liability using a revised discount rate and adjusts the right-of-use asset. Lessors reassess classification and account for the modified lease accordingly.

How does impairment affect right-of-use assets?

Impairment reduces the carrying amount of a right-of-use asset when the related asset group is not recoverable. The company writes the asset down to fair value, recognizes an impairment loss, and then adjusts future expense recognition. For operating leases, impairment can change the straight-line expense pattern.

Related Articles

Accounting for a Finance Lease

The Difference Between a Finance Lease and an Operating Lease