Accounting information system definition

/What is an Accounting Information System?

An accounting information system (AIS) is one that accumulates, stores, and processes financial and accounting information. The system generates reports that are used to make decisions regarding how an organization is to be run. These reports are also used by outsiders to evaluate lending and investment opportunities with the firm. The key elements of the system are as follows:

The policies and procedures governing how information is collected.

The internal controls used to ensure that information is recorded correctly.

The training employed to ensure that users operate the system correctly.

The software and integrated database used to store and process information.

The hardware on which the software and database are stored.

An accounting information system is usually run using electronic data processing equipment, but can be operated less efficiently with a manual bookkeeping system. Using a computer-based system is highly advantageous, since it automates many accounting processes and thereby reduces transactional error rates. It can also produce reports much more quickly than a manual system.

Data and Information

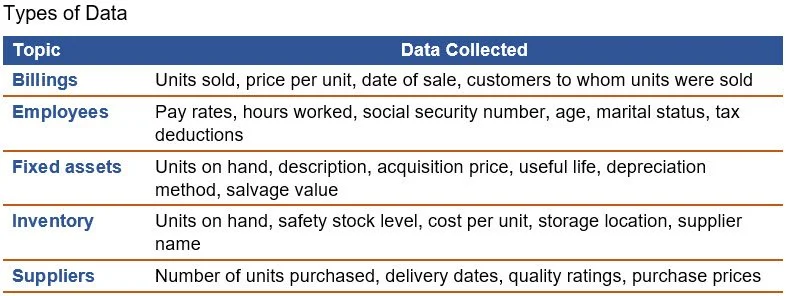

Data are stored in an AIS. Data are facts that are collected, stored, and used by an organization. There are many types of data needed by a company, as noted in the following exhibit.

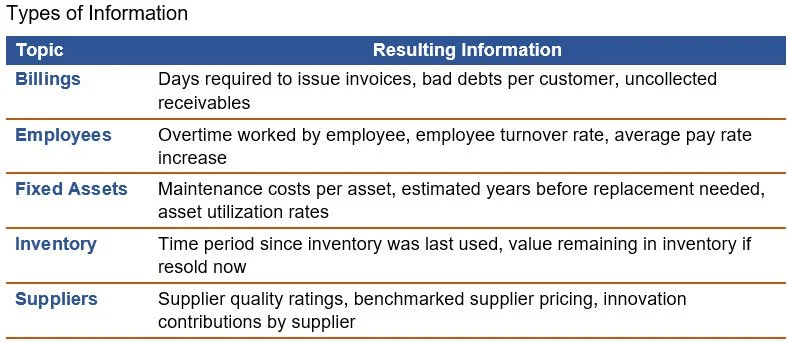

Once data have been organized and processed within a context that gives it meaning and relevance, it is referred to as information. Information is an essential input for managers, who need it to make higher-quality decisions, as well as to reduce the level of uncertainty. Examples of information are noted in the following exhibit. A primary function of an AIS is to transform data into information.

The amount of data stored by the AIS of even a moderate-sized business is immense, so the system is needed to sort through and condense it into a more usable form. For example, an AIS is routinely used to present to a collections clerk only those invoices that are more than a certain number of days overdue for payment, and only in relation to customers in the clerk’s designated collection area.

Components of an Accounting Information System

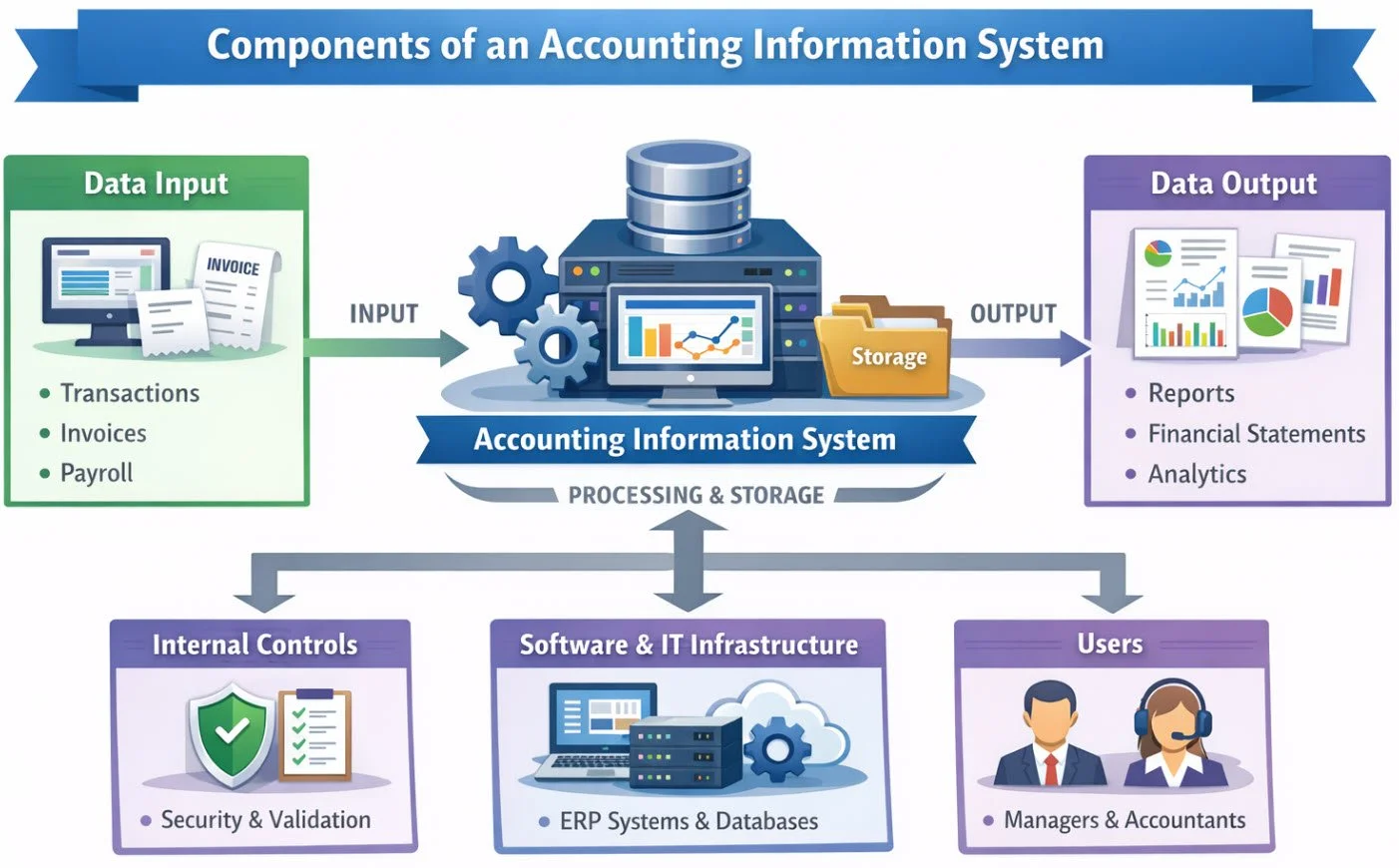

An accounting information system accepts data inputs from a variety of sources, such as sale transactions, cash receipts, supplier invoices, and payroll time cards. These inputs are stored within the AIS, which uses a number of internal controls to validate them. The system then generates outputs as needed, which include financial statements, analytics, and department-level reports. The outputs are used not only by accountants, but also by managers and other personnel throughout the organization. The basic components of an accounting information system are shown in the following exhibit.

Reports Generated by an Accounting Information System

An accounting information system generates a range of reports that support daily operations, internal management, and external financial reporting. Some reports are used to record and monitor transactions, while others help managers analyze performance, control assets, and meet compliance requirements. The more common reports are as follows;

Income statement. This report shows revenues, expenses, and profit or loss for a specific period. It helps management evaluate operating performance and financial results.

Balance sheet. The balance sheet presents assets, liabilities, and equity as of a specific date. It provides a snapshot of the organization’s financial position.

Statement of cash flows. This report summarizes cash inflows and outflows from operating, investing, and financing activities. It is useful for assessing liquidity and cash management.

General ledger report. The general ledger report lists all account activity recorded in the accounting system. It serves as the central summary of financial transactions by account.

Trial balance. A trial balance shows the ending balances in all ledger accounts at a point in time. It is used to confirm that total debits equal total credits before preparing financial statements.

Accounts receivable aging report. This report classifies customer receivables by how long they have been outstanding. It helps management monitor collections and identify overdue accounts.

Accounts payable aging report. The accounts payable aging report groups unpaid supplier invoices by age. It helps a company manage payment timing and maintain vendor relationships.

Sales report. A sales report summarizes revenue by product, customer, region, or time period. It is useful for tracking sales trends and evaluating business activity.

Purchases report. This report lists purchases made from suppliers during a period. It helps management review spending patterns and purchasing activity.

Inventory report. An inventory report shows quantities on hand, inventory values, and stock movements. It helps control inventory levels and supports purchasing and production decisions.

Budget vs. actual report. This report compares planned amounts to actual results for revenues, expenses, or other financial measures. It is used to identify variances and improve budgetary control.

Payroll report. Payroll reports summarize wages, salaries, taxes, and deductions for employees. They are important for payroll processing, compliance, and labor cost analysis.

Fixed asset report. A fixed asset report lists the company’s long-term assets, including cost, accumulated depreciation, and net book value. It supports asset tracking and depreciation accounting.

Cash receipts report. The cash receipts report summarizes all incoming cash from customers and other sources. It is useful for tracking collections and cash inflows.

Cash disbursements report. This report lists all outgoing cash payments made by the business. It helps management monitor expenditures and review cash usage.

Departmental performance report. This report shows revenues, expenses, and profits by department, division, or business segment. It helps management evaluate the performance of different parts of the organization.

Together, these reports allow an accounting information system to support transaction processing, financial control, decision-making, and external reporting. The exact set of reports varies by organization, but these are the main ones commonly generated in practice.

Advantages of an Accounting Information System

There are several advantages to operating an accounting information system. They are as follows:

Centralized repository. The system organizes business transactions from across an organization, storing it in a central repository. This centralized storage keeps transactional data consistent, and ensures that it is overseen by one department - the accounting department.

Integrated controls. The system incorporates a number of controls that can be used to mitigate the loss of company assets, while ensuring that transactions are only completed that have been properly authorized.

Enhanced accuracy. The system has built-in validation rules ensure data integrity and compliance with accounting standards.

Real-time data access. The system provides real-time financial insights and reporting, helping businesses make informed decisions quickly.

Better financial management. The system centralizes financial data for comprehensive budgeting, forecasting, and performance analysis.

Improves regulatory compliance. The system helps ensure compliance with legal and regulatory requirements, such as tax reporting and financial standards (e.g., GAAP, IFRS).

Enhanced security. The system protects sensitive financial data with encryption, user authentication, and access controls.

Scalability. The system supports growing business needs by handling larger volumes of transactions and data as the organization expands.

Cost savings. The system reduces costs associated with manual accounting processes, paper records, and errors. It also saves money on external auditing and consultancy by maintaining organized and accurate records.

Integration with other systems. The system connects seamlessly with other enterprise systems like inventory management, payroll, and customer relationship management (CRM).

By leveraging an AIS, organizations can enhance their financial processes, increase accuracy, and gain a competitive advantage through better financial management and decision-making.

Accounting Information System FAQs

What risks are associated with an accounting information system?

The risks associated with an accounting information system include unauthorized access, data entry errors, system failures, poor integration, weak internal controls, and cybersecurity threats. These issues can lead to inaccurate financial reporting, lost data, fraud, compliance problems, and delayed decision-making if the system is not properly designed, secured, and monitored.

Why is integration important in an accounting information system?

Integration is important in an accounting information system because it allows data to flow automatically between functions such as sales, purchasing, payroll, inventory, and general ledger. This reduces duplicate entry, improves accuracy, speeds reporting, and gives management a more complete and timely view of business activity and financial results.