Current portion of long-term debt definition

/What is the Current Portion of Long-Term Debt?

The current portion of long-term debt represents the principal amount of a long-term borrowing that is scheduled to be repaid within one year of the balance sheet date. It is classified as a current liability because it requires the use of current assets or the creation of other current liabilities for settlement. The amount is determined based on the contractual repayment schedule and excludes accrued interest, which is reported separately as interest payable. Each reporting period, the portion of principal due in the upcoming year is reclassified from noncurrent to current liabilities. This classification directly affects liquidity measures such as working capital and the current ratio, making it an important indicator of near-term debt obligations.

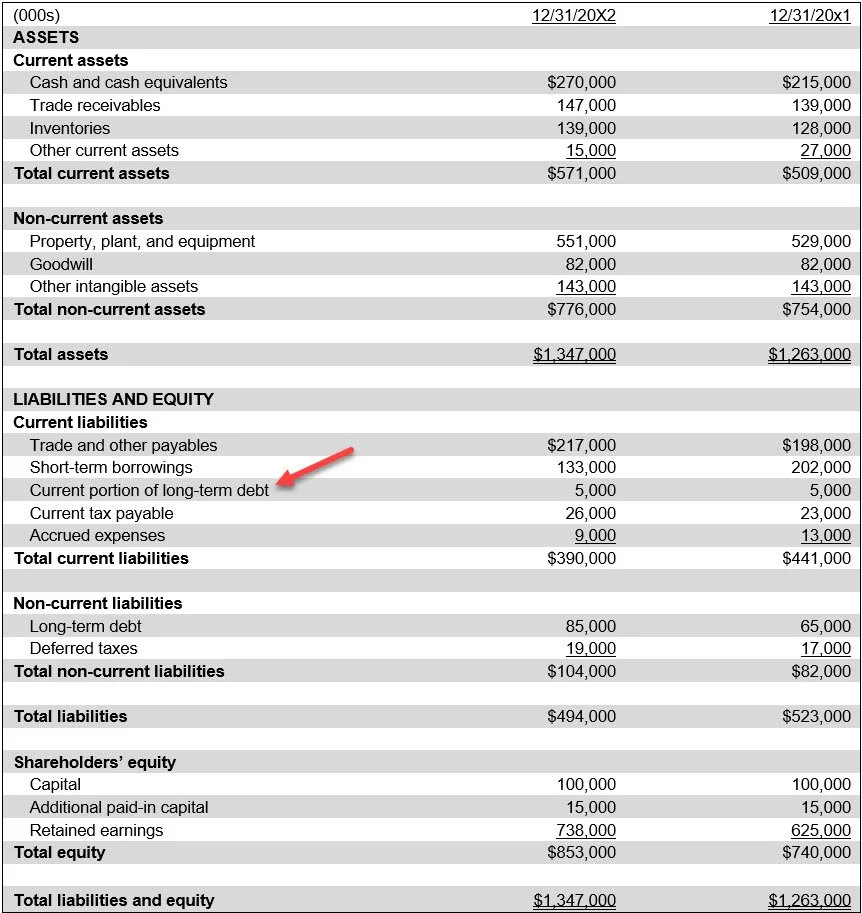

A sample presentation of this line item appears in the following balance sheet exhibit.

Related AccountingTools Course

Example of the Current Portion of Long-Term Debt

A business has a $1,000,000 loan outstanding, for which the principal must be repaid at the rate of $200,000 per year for the next five years. In the balance sheet, $200,000 will be classified as the current portion of long-term debt, and the remaining $800,000 as long-term debt.

Current Debt vs. Long-Term Debt

Current debt refers to the portion of a company’s total debt that is due within one year, such as short-term loans, the current portion of long-term loans, or lines of credit, and it is reported under current liabilities on the balance sheet. In contrast, long-term debt represents obligations that are not due within the next year, such as bonds payable, long-term leases, or loans with extended repayment periods, and is recorded under non-current liabilities. The distinction is important for assessing a company’s short-term liquidity versus its long-term solvency. While current debt pressures immediate cash flow management, long-term debt impacts future financial commitments and interest expense planning.