Capital Budgeting Explained

/What is Capital Budgeting?

Capital budgeting is the process that a business uses to determine which proposed fixed asset purchases it should accept, and which should be declined. This process is used to create a quantitative view of each proposed fixed asset investment, thereby giving a rational basis for making a judgment. This analysis is especially necessary when there are not enough funds available to pay for all of the projects being requested. Lenders may require this analysis when they are being asked to loan funds to pay for a project; they can then review the analysis to gain a better understanding of the cash flows involved, as well as the risks of failure.

Capital Budgeting Methods

There are a number of methods commonly used to evaluate fixed assets under a formal capital budgeting system. The more important ones are noted below.

Net Present Value Analysis

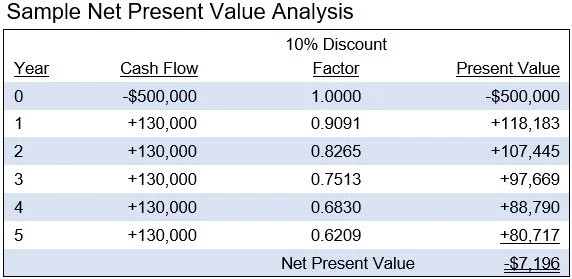

Under net present value analysis, identify the net change in cash flows associated with a fixed asset purchase, and discount them to their present value. Then compare all proposed projects with positive net present values, and accept those with the highest net present values until funds run out. A concern with using net present value analysis is that the future cash flows associated with a project are uncertain, and are subject to manipulation. The result can be projected cash flows that have been adjusted to ensure that a project will be approved. This issue can only be discovered after the fact, by comparing actual to projected cash flows. Another concern with net present value analysis is that the discount rate used to derive present values can be adjusted downward to ensure that a project is approved; this is usually justified on the grounds that a project is low risk. In short, this supposedly quantitative analysis method is actually subject to qualitative alterations that can significantly impact the decision outcome. A sample net present value analysis appears in the following exhibit, where a company is planning to acquire an asset that it expects will yield positive cash flows for the next five years. Its cost of capital is 10%, which it uses as the discount rate to construct the net present value of the project. The net present value of the proposed project is negative at the 10% discount rate, so the company should not invest in it.

Constraint Analysis

Under constraint analysis, identify the bottleneck machine or work center in a production environment and invest in those fixed assets that maximize the utilization of the bottleneck operation. Under this approach, a business is less likely to invest in areas downstream from the bottleneck operation (since they are constrained by the bottleneck operation) and more likely to invest upstream from the bottleneck (since additional capacity there makes it easier to keep the bottleneck fully supplied with inventory). This is perhaps the best capital budgeting analysis tool, since it can consistently result in capital investments that improve company profits.

Payback Period

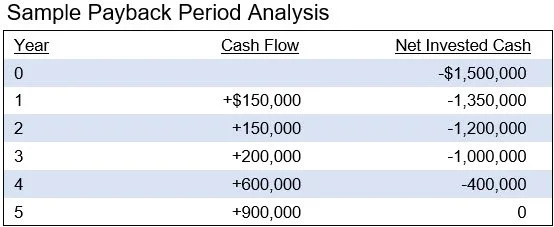

Under the payback approach, determine the period required to generate sufficient cash flow from a project to pay for the initial investment in it. This is essentially a risk measure, for the focus is on the period of time that the investment is at risk of not being returned to the company. This analysis is most useful when used as a supplement to the preceding two analysis methods, rather than as the primary basis for deciding whether to make an investment. A sample payback period analysis appears in the following exhibit, where successive periods of projected cash inflows are deducted from the initial amount of invested cash to determine how long it will take to achieve payback of the initial amount.

The exhibit indicates that the payback period is located somewhere between Year 4 and Year 5. There is $400,000 of investment yet to be paid back at the end of Year 4, and there is $900,000 of cash flow projected for Year 5. Assuming the same amount of cash flow in Year 5, the final payback should be just short of 4.5 years.

Discounted Payback

The accuracy of the payback method can be improved by incorporating the time value of money into the cash flows expected in each future year, which is known as discounted payback. However, doing so increases the complexity of this analysis method. To apply the time value of money to the calculation, follow these steps:

Create a table in which is listed the expected cash outflow related to the investment in Year 0.

In the following lines of the table, enter the cash inflows expected from the investment in each subsequent year.

Multiply the expected annual cash inflows in each year in the table by the applicable discount rate, using the same interest rate for all of the periods in the table. No discount rate is applied to the initial investment, since it occurs at once.

Create a column on the far right side of the table that lists the cumulative discounted cash flow for each year. The calculation in this final column is to add back the discounted cash flow in each period to the remaining negative balance from the preceding period. The balance is initially negative because it includes the cash outflow to fund the project.

When the cumulative discounted cash flow becomes positive, the time period that has passed up until that point represents the payback period.

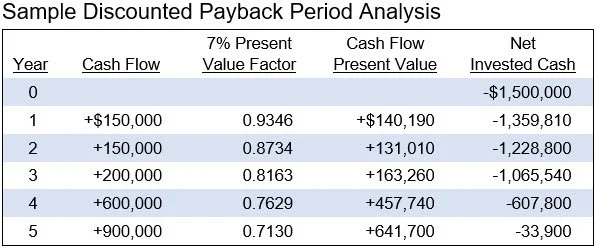

We will continue with the preceding payback example. The cost of capital is 7%, so the present value factor for 7% is included in the payback table, with the following results:

The discounted payback calculation reveals that the payback period will be slightly longer than the five years of cash flows presented in the original payback analysis.

Avoidance Analysis

Under avoidance analysis, determine whether increased maintenance can be used to prolong the life of existing assets, rather than investing in replacement assets. This analysis can substantially reduce a company's total investment in fixed assets. This is an especially useful option when the incremental maintenance expenditure is not significant, such as when there is no need for a major equipment overhaul. However, it may make more sense to upgrade to new equipment when the skills required to maintain the current equipment are so difficult to obtain that the business would be in trouble if its maintenance personnel were to leave the company.

Capital Budgeting Forms

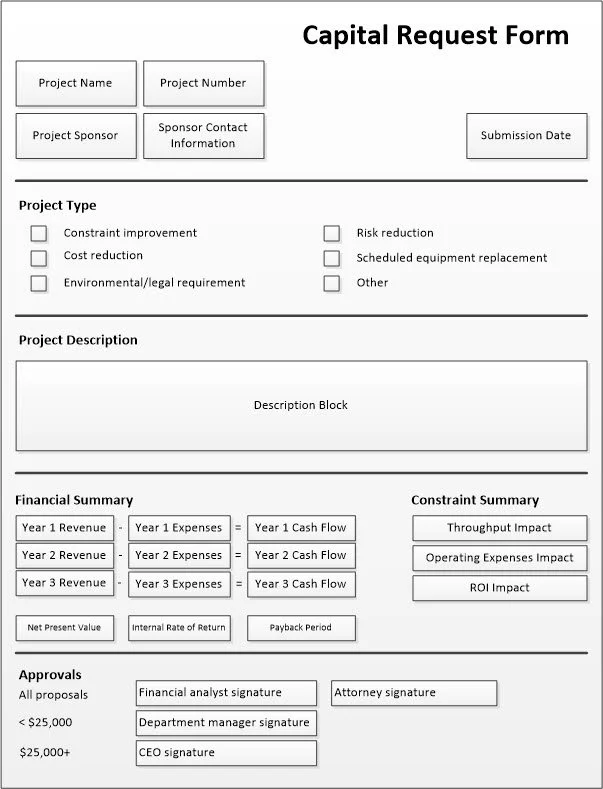

A business will usually institute a formal procedure for capital budgeting, in order to provide a consistent flow of information to those tasked with making investment decisions. Part of this procedure will likely be a standardized capital budgeting request form, in which the applicant states the case of investing in a particular project. An example appears below, containing separate blocks that identify a project, state the type of project, describe it, and provide a summary of its financial and constraint impacts. There is also a signature block at the bottom, to be filled out by those authorized to do so.

The Importance of Capital Budgeting

The amount of cash involved in a fixed asset investment may be so large that it could lead to the bankruptcy of a firm if the investment fails. Consequently, capital budgeting is a mandatory activity for larger fixed asset proposals. This is less of an issue for smaller investments; in these latter cases, it is better to streamline the capital budgeting process substantially, so that the focus is more on getting the investments made as expeditiously as possible; by doing so, the operations of profit centers are not hindered by the analysis of their fixed asset proposals.

Common Capital Budgeting Mistakes

Capital budgeting mistakes usually arise when the analysis excludes relevant cash flows, includes irrelevant costs, or relies on assumptions that do not reflect economic reality. The most common mistakes are as follows:

Treating sunk costs as relevant costs. Sunk costs have already been incurred and cannot be changed by accepting or rejecting a project. Including them distorts the investment decision by making a project appear less attractive than it really is. The analysis should focus only on future incremental cash flows.

Ignoring working capital requirements. A project may require additional inventory, receivables, or operating cash before it generates returns. Excluding these needs understates the initial investment and overstates project profitability. Any working capital released at the end of the project should also be included.

Using accounting profit instead of cash flow. Accounting profit includes noncash charges, accruals, and allocations that may not reflect actual cash movement. Capital budgeting should focus on cash inflows and outflows, since investment value depends on the timing and amount of cash generated.

Omitting tax effects. Taxes can materially change project economics through depreciation deductions, tax credits, taxable gains, and deductible expenses. Ignoring these effects can overstate or understate returns. The analysis should use after-tax cash flows when evaluating investment value.

Ignoring disposal value. Equipment, property, or other project assets may have resale or salvage value at the end of the project. Excluding this amount understates total cash inflows. The analysis should also consider tax effects from gains or losses on disposal.

Using an unrealistic discount rate. A discount rate that is too low can make risky projects appear attractive, while a rate that is too high can reject sound investments. The rate should reflect the project’s risk, financing environment, and opportunity cost of capital.

Failing to consider project interdependencies. Some projects affect other projects, products, departments, or capacity constraints. One investment may increase sales elsewhere, reduce another product’s demand, or require additional support spending. Ignoring these relationships can produce an incomplete view of project value.

Approving projects without post-completion review. Without a post-completion review, management cannot determine whether actual results matched the original assumptions. This weakens accountability, hides forecasting errors, and reduces learning. Reviews improve future estimates and encourage more disciplined project proposals.

A sound capital budgeting process separates relevant from irrelevant information, evaluates after-tax cash flows, and tests assumptions before and after project approval.

Capital Budgeting FAQs

How is risk considered in capital budgeting?

Risk in capital budgeting is considered by analyzing how changes in key assumptions affect a project's outcomes, using tools like sensitivity analysis and scenario analysis. Companies may also adjust the discount rate upward for riskier projects to reflect the higher required return. This helps ensure that only projects with acceptable risk-reward profiles are selected.

How should qualitative factors be incorporated into capital budgeting?

Qualitative factors should supplement, not replace, financial analysis in capital budgeting. Management should evaluate issues such as strategic alignment, regulatory exposure, operational risk, environmental impact, employee safety, and customer relationships. These factors may justify approving or rejecting a project even when its numerical results alone appear acceptable.

How should capital budgeting address uncertainty in cash flow estimates?

Capital budgeting should address uncertainty by testing how project results change under different assumptions. Sensitivity analysis, scenario analysis, probability estimates, and simulation models can reveal the effects of changes in sales, costs, timing, and project life. This process helps management identify key risks and make better-informed investment decisions.

Related Articles

Capacity Planning in the Budget