Stage 1 allocation definition

/What is a Stage 1 Allocation?

A stage 1 allocation is the distribution of costs to activities. The concept is used in activity-based costing; it is a preliminary step in the allocation of overhead. A stage 2 allocation involves distributing the costs of activities to cost objects. Using two stages of allocations is intended to result in more accurate overhead allocations. The resulting information can give insights into how overhead costs are being consumed by various activities.

Example of a Stage 1 Allocation

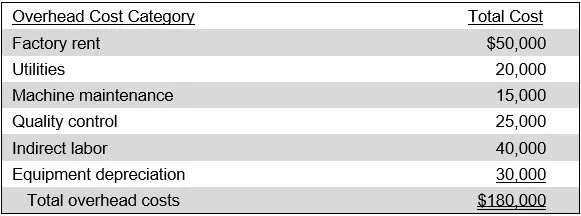

A manufacturing company, Pelican Products, produces electronic components. The company uses Activity-Based Costing (ABC) to allocate overhead costs to different activities before assigning them to products. Pelican has the following overhead costs in a given month:

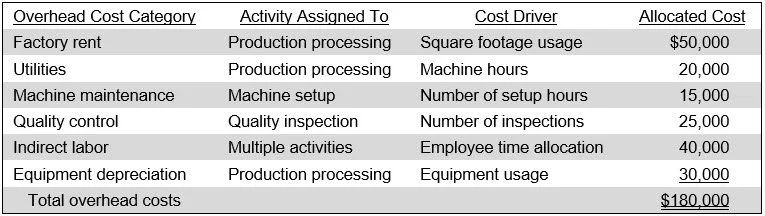

The company has identified the following key activities that consume overhead resources:

Material handling. Moving raw materials to production lines.

Machine setup. Preparing machines for different production runs.

Production processing. Running machines and assembly.

Quality inspection. Checking for defects.

Packaging and shipping. Finalizing and distributing products.

Pelican then assigns overhead costs to activities based on cost drivers, which represent the factors that cause overhead costs to be incurred. Its allocation appears in the following exhibit.

At the end of the stage 1 allocation, the $180,000 of overhead costs have been distributed to activities in the following manner: