Intangible asset accounting

/What is an Intangible Asset?

An intangible asset is a non-physical asset that provides long-term value to a business. Examples include patents, trademarks, copyrights, brand recognition, and goodwill. These assets are often acquired through purchase or developed internally and are recorded on the balance sheet if they meet specific recognition criteria.

What is the Accounting for an Intangible Asset?

The accounting for intangible assets involves recognizing, measuring, and reporting those assets that provide future economic benefits. Intangible assets acquired externally, such as patents, trademarks, or copyrights, are recorded at their purchase cost, including legal and registration fees. Internally generated intangibles, like brand value or customer lists, are generally not capitalized, except for certain development costs under strict criteria (e.g., for software development). Intangible assets with a finite useful life are amortized over their expected life, while those with an indefinite life, such as goodwill, are not amortized but are instead tested annually for impairment. If the carrying amount exceeds the recoverable amount, an impairment loss is recognized in the income statement.

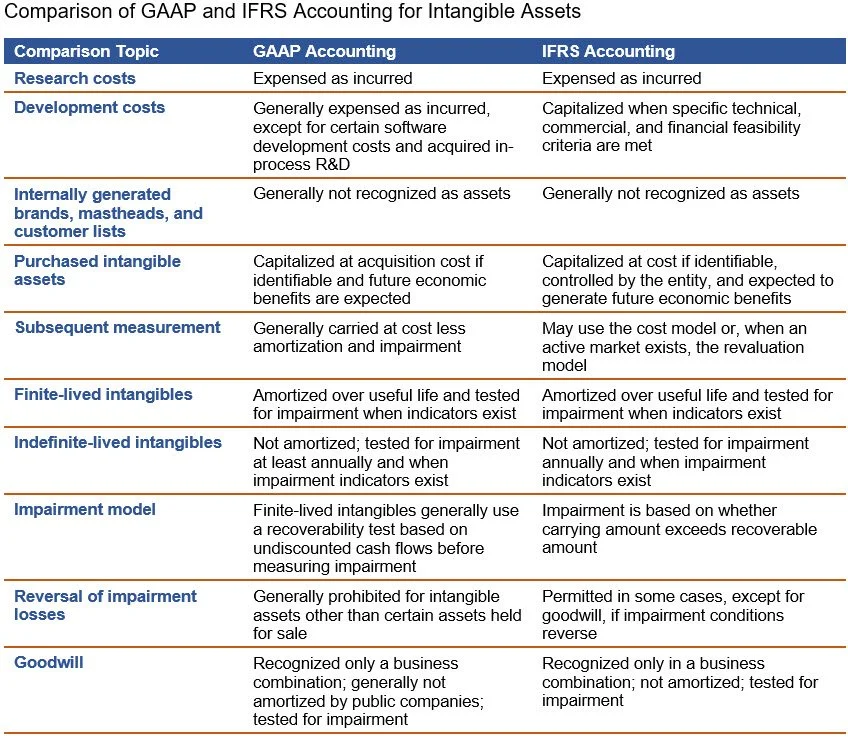

U.S. GAAP vs IFRS Treatment of Intangible Assets

U.S. GAAP and IFRS differ mainly in how they treat internally generated intangible assets. Under U.S. GAAP, research and development costs are generally expensed as incurred, except for certain software development costs and acquired in-process research and development. Under IFRS, research costs are expensed, but development costs are capitalized when specified technical, commercial, and financial feasibility criteria are met. U.S. GAAP generally uses the cost model after recognition, while IFRS allows either the cost model or, when an active market exists, the revaluation model. Both frameworks amortize finite-lived intangible assets over their useful lives and test them for impairment when indicators exist. Indefinite-lived intangibles are not amortized but are tested for impairment. The essential differences between the two accounting frameworks are noted in the following exhibit.

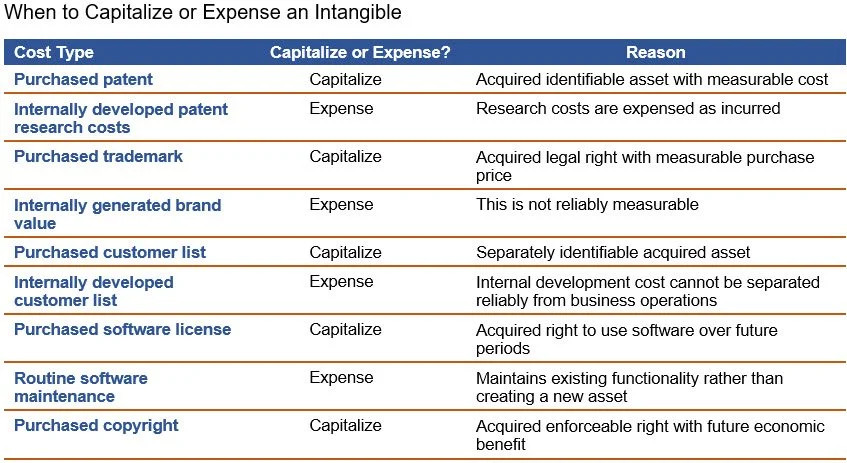

Recognition Criteria: Capitalize or Expense?

An intangible asset is generally capitalized when it is acquired from another party, is separately identifiable, provides probable future economic benefits, and has a measurable cost. Examples include purchased patents, trademarks, copyrights, licenses, and customer lists. The capitalized cost is then amortized if the asset has a finite useful life, or tested for impairment if it has an indefinite life. Costs are generally expensed when they relate to internally generated value, routine advertising, training, research, maintenance, or general business development, since these costs usually cannot be separated reliably from ongoing operations. The following exhibit shows the proper accounting treatment for many of the more common intangible assets.

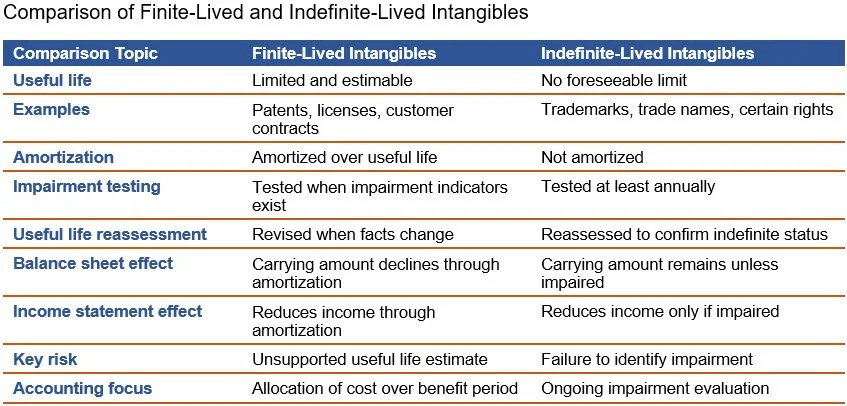

Differences Between Finite-Lived and Indefinite-Lived Intangibles

Finite-lived intangibles have a limited period of economic benefit, such as a patent, license, or customer contract with a defined term. Indefinite-lived intangibles are expected to generate benefits for an uncertain or unlimited period, such as a renewable trademark or trade name. Finite-lived intangibles are amortized over their estimated useful lives, while indefinite-lived intangibles are not amortized. Instead, indefinite-lived intangibles are tested for impairment at least annually, while finite-lived intangibles are tested when events indicate that their carrying amount may not be recoverable. The classification affects reported earnings, since finite-lived assets create recurring amortization expense, while indefinite-lived assets affect income mainly when impairment occurs. The key differences between the two concepts are noted in the following exhibit.

Differences Between Tangible and Intangible Asset Accounting

The key differences between the accounting for tangible and intangible fixed assets are as follows:

Amortization. If an intangible asset has a useful life, amortize the cost of the asset over that useful life, less any residual value. Amortization is the same as depreciation, except that amortization is applied only to intangible assets. In this context, useful life refers to the time period over which an asset is expected to enhance future cash flows.

Asset combinations. If several intangible assets are operated as a single asset, combine them for the purposes of impairment testing. This treatment is probably not suitable if they independently generate cash flows, would be sold separately, or are used by different asset groups.

Residual value. If any residual value is expected following the useful life of an intangible asset, subtract it from the carrying amount of the asset for the purposes of calculating amortization. Assume that the residual value will always be zero for intangible assets, unless there is a commitment from another party to acquire the asset at the end of its useful life, and the residual value can be determined by reference to transactions in an existing market, and that market is expected to be in existence when the useful life of the asset ends.

Useful life. An intangible asset may have an indefinite useful life. If so, do not initially amortize it, but review the asset at regular intervals to see if a useful life can then be determined. If so, test the asset for impairment and begin amortizing it. The reverse can also occur, where an asset with a useful life is judged to now have an indefinite useful life; if so, stop amortizing the asset and test it for impairment. Examples of intangible assets that have indefinite useful lives are taxicab licenses, broadcasting rights, and trademarks.

Useful life revisions. Regularly review the duration of the remaining useful lives of all intangible assets, and adjust them if circumstances warrant the change. This will require a change in the remaining amount of amortization recognized per period.

Life extensions. It is possible that the life of some intangible assets may be extended a considerable amount, usually based on contract extensions. If so, estimate the useful life of an asset based on the full duration of expected useful life extensions. These presumed extensions may result in an asset having an indefinite useful life, which avoids amortization.

Straight-line amortization. Use the straight-line basis of amortization to reduce the carrying amount of an intangible asset, unless the pattern of benefit usage associated with the asset suggests a different form of amortization.

Impairment testing. An intangible asset is subject to impairment testing in the same manner as tangible assets. Recognize impairment if the carrying amount of the asset is greater than its fair value, and the amount is not recoverable. Once recognized, the impairment cannot be reversed.

Research and development assets. If intangible assets are acquired through a business combination for use in research and development activities, initially treat them as having indefinite useful lives, and regularly test them for impairment. Once the related research and development activities have been completed or abandoned, charge them to expense.

In general, you should recognize costs as incurred when they are related to internally developing, maintaining, or restoring intangible assets that have any of the following characteristics:

There is no specifically identifiable asset

The useful life is indeterminate

The cost is inherent in the continuing operation of the business

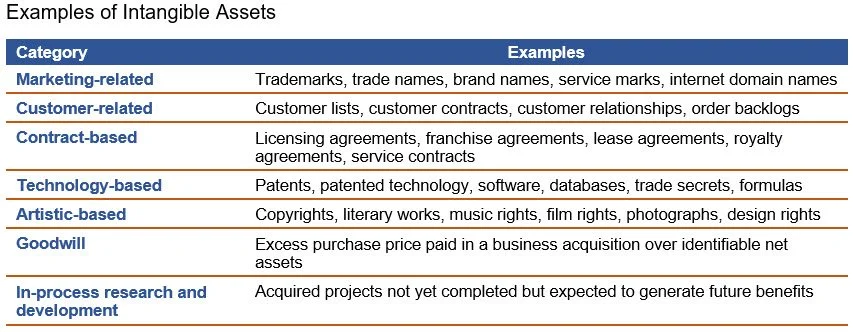

Examples of Intangible Assets

There are many types of intangible assets that cover a range of categories, including assets that are marketing-related, customer-related, and contract-based. Examples of the more common intangible assets are noted in the following exhibit.

Common Errors in Intangible Asset Accounting

Intangible asset accounting errors often arise when management applies inconsistent capitalization, amortization, impairment, or disclosure judgments. These errors can materially affect reported assets, expenses, income, and financial statement transparency. The following errors can arise:

Capitalizing internally generated brand value. Internally developed brand value is generally not recognized as an asset under U.S. GAAP, because it is difficult to distinguish from the overall cost of building the business.

Amortizing an indefinite-lived trademark. A trademark with an indefinite useful life should not be amortized. Instead, it should be tested for impairment when required.

Failing to amortize a finite-lived customer list. A customer list with a determinable useful life should be amortized over the period in which it is expected to provide economic benefit.

Ignoring impairment indicators. Management should evaluate intangible assets for impairment when events or circumstances suggest that their carrying amount may not be recoverable.

Treating goodwill as a normal amortizable intangible under U.S. GAAP. Goodwill is not amortized by public companies under U.S. GAAP. It is tested for impairment instead.

Assigning a residual value without support. Residual value should not be assumed unless there is persuasive evidence, such as a committed third-party purchase or an active market.

Capitalizing ordinary advertising or training costs. Routine advertising and employee training costs are generally expensed as incurred, rather than capitalized as intangible assets.

Failing to reassess useful lives. Useful lives should be reconsidered when facts change, such as customer attrition patterns, legal rights, technology changes, or market conditions.

Confusing tax amortization with book amortization. Tax rules may allow amortization methods or periods that differ from financial reporting requirements, so tax treatment should not automatically drive book accounting.

Omitting disclosures for significant intangible assets. Significant intangible assets require appropriate disclosures, such as carrying amounts, amortization expense, useful lives, impairment losses, and related assumptions.

Intangible Asset FAQs

Are intangible assets depreciated or amortized?

Intangible assets are amortized, not depreciated. Depreciation applies to tangible fixed assets, such as equipment and buildings. Amortization allocates the cost of a finite-lived intangible asset, such as a patent or customer list, over its useful life. Indefinite-lived intangible assets, such as some trademarks, are tested for impairment instead.

Can an intangible asset have residual value?

Yes. An intangible asset can have residual value, but it is usually assumed to be zero unless there is evidence of a resale market, contractual repurchase, or another reliable basis for estimating value at the end of its useful life. Residual value reduces the amount amortized over the asset’s life.

What is the difference between goodwill and other intangible assets?

Goodwill arises only in a business combination and represents the excess purchase price over identifiable net assets acquired. Other intangible assets, such as patents, trademarks, customer lists, and software, are separately identifiable and may be bought, sold, licensed, or legally protected. Goodwill is not amortized but tested for impairment.