Fiduciary Accounting Explained

/What is Fiduciary Accounting?

Fiduciary accounting involves recording the transactions associated with a trust or estate entity, and issuing periodic reports on the status of the entity. This accounting is dealt with on a cash basis, where cash is recorded when received and disbursements and distributions are recorded when paid.

A large part of the trustee’s accounting work involves determining whether receipts and disbursements should be assigned to income or principal. Income is money or property received as a current return from a principal asset, while principal is property held in trust for later distribution to a remainder beneficiary. The rules for how to allocate receipts and disbursements may be contained within the relevant will or trust document; if not, the trustee uses the rules laid out in the Uniform Principal and Income Act (as modified by the applicable state government).

In addition, a will or trust agreement may have a unique distribution scheme that varies from the standard approach of issuing income periodically to the income beneficiary, with the remainder beneficiary receiving the principal at a later date. Thus, the accounting associated with a specific estate or trust could be entirely unique from what is needed for other estates or trusts.

The Fiduciary Accounting Report

At least once a year, the trustee issues a fiduciary accounting to all trustee beneficiaries. There is no fixed format for this document, but it usually contains the following items:

Cover page and summary of accounts

Schedule of receipts

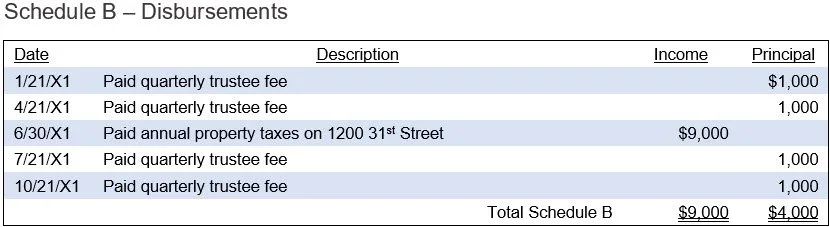

Schedule of disbursements

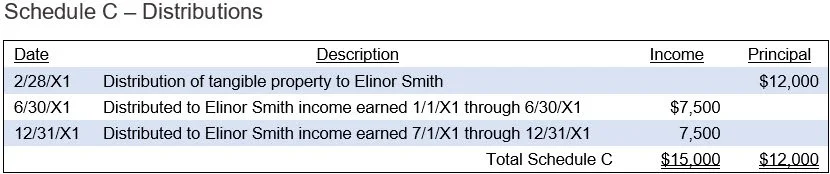

Schedule of distributions

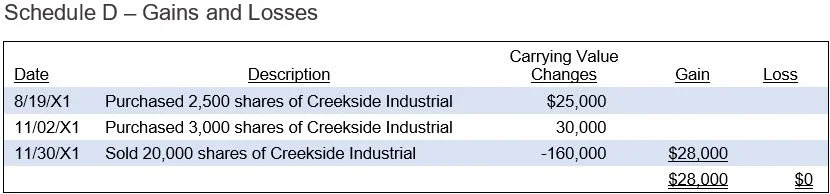

Schedule of gains and losses

Beginning and ending schedules of assets on hand

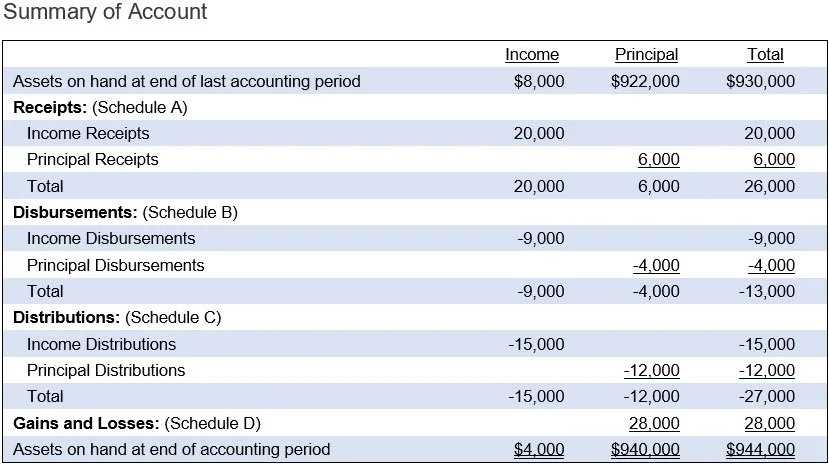

A sample summary of accounts and supporting schedules appear in the following exhibits.

Carrying Value in Fiduciary Accounting

Another fiduciary accounting issue is the concept of carrying value. In most accounting frameworks, this simply means the current book value of an asset, but in a fiduciary accounting system, it means that an asset’s value has been remeasured after a specific event, such as the start of a trustee’s administration, so that subsequent changes in asset value can be ascribed to that specific trustee.

Transfers Between Income and Principal

The trustee may also need to account for transfers between income and principal. These transactions may be needed to pay for large expenses, to make significant capital investments, or to pay for trust indebtedness.

Fiduciary Accounting FAQs

Are fiduciary accounting standards uniform across jurisdictions?

No. Fiduciary accounting standards are not fully uniform across jurisdictions. Uniform laws, such as the Uniform Principal and Income Act and Uniform Trust Code, influence many states, but states adopt, modify, or reject provisions differently. Reporting duties, principal-income allocations, court procedures, and fiduciary obligations therefore can vary by state significantly.