Effective interest method definition

/What is the Effective Interest Method?

The effective interest method is a technique for calculating the actual interest rate in a period based on the amount of a financial instrument's book value at the beginning of the accounting period. Thus, if the book value of a financial instrument decreases, so too will the amount of related interest; if the book value increases, so too will the amount of related interest. This method is used to account for bond premiums and bond discounts. A bond premium occurs when investors are willing to pay more than the face value of a bond, because its stated interest rate is higher than the prevailing market interest rate. A bond discount occurs when investors are only willing to pay less than the face value of a bond, because its stated interest rate is lower than the prevailing market rate.

If an entity buys or sells a financial instrument for an amount other than its face amount, this means that the interest rate it is actually earning or paying on the investment is different from the stated interest paid on the financial instrument. For example, if a company buys a financial instrument for $95,000 that has a face amount of $100,000 and which pays interest of $5,000, then the actual interest it is earning on the investment is $5,000 / $95,000, or 5.26%.

Under the effective interest method, the effective interest rate, which is a key component of the calculation, discounts the expected future cash inflows and outflows expected over the life of a financial instrument. In short, the interest income or interest expense recognized in a reporting period is the effective interest rate multiplied by the carrying amount of a financial instrument.

Formula for the Effective Interest Rate

The following formula shows how to calculate the effective interest rate:

[(1+i/n)^n-1] x Current book value = Effective interest rate

In this formula, “i” is the bond’s coupon rate, while “n” is the number of coupon payments to be made per year.

The Effective Interest Method vs. the Straight-Line Method

The effective interest method is preferable to the straight-line method of charging off premiums and discounts on financial instruments, because the effective method is considerably more accurate on a period-to-period basis. However, it is also more difficult to compute than the straight-line method, since the effective method must be recalculated every month, while the straight-line method charges off the same amount in every month. Thus, in cases where the amount of the discount or premium is immaterial, it is acceptable to instead use the straight-line method. By the end of the amortization period, the amounts amortized under the effective interest and straight-line methods will be the same.

Example of the Effective Interest Method

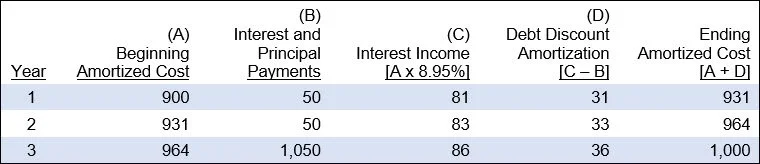

As an example, Muscle Designs Company, which makes weight lifting equipment for retail outlets, acquires a bond that has a stated principal amount of $1,000, which the issuer will pay off in three years. The bond has a coupon interest rate of 5%, which is paid at the end of each year. Muscle buys the bond for $900, which is a discount of $100 from the face amount of $1,000. Muscle classifies the investment as held-to-maturity, and records the following entry:

Based on a payment of $900 to buy the bond, three interest payments of $50 each, and a principal payment of $1,000 upon maturity, Muscle derives an effective interest rate of 8.95%. Using this rate, Muscle's controller creates the following amortization table for the bond discount:

Using the table, Muscle's controller records the following journal entries in each of the next three years:

Year 1:

Year 2:

Year 3:

Effective Interest Method FAQs

Is the effective interest method required under IFRS and GAAP?

Under IFRS the effective interest method is required for amortizing premiums, discounts, and transaction costs on financial instruments. Under U.S. GAAP, the method is preferred because it provides a more accurate allocation of interest expense, but the straight-line method is permitted if the results are not materially different. This means IFRS is stricter, while GAAP allows some flexibility.

Terms Similar to Effective Interest Method

The effective interest method is also known as the effective interest rate method.