Cash flow statement template

/The cash flows of a business are reported on the statement of cash flows. There are two variations on the template for this report, which are the direct method and the indirect method. The indirect method is used by nearly all organizations, since it is much easier to derive from the existing accounts.

Cash Flow Statement Classifications

In the statement of cash flows, cash flow information is reported within three separate classifications. The use of classifications is intended to improve the quality of the information presented. These classifications are noted below.

Operating Activities

Operating activities are an entity’s primary revenue-producing activities. Operating activities is the default classification, so if a cash flow does not belong in either of the following two classifications, it belongs in this classification. Operating cash flows are generally associated with revenues and expenses. Examples of cash inflows from operating activities are cash receipts from the sale of goods or services, accounts receivable, lawsuit settlements, normal insurance settlements, and supplier refunds. Examples of cash outflows for operating activities are for payments to employees and suppliers, fees and fines, lawsuit settlements, cash payments to lenders for interest, contributions to charity, cash refunds to customers, and the settlement of asset retirement obligations.

Investing Activities

Investing activities are investments in productive assets, as well as in the debt and equity securities issued by other entities. These cash flows are generally associated with the purchase or sale of assets. Examples are cash receipts from the sale or collection of loans, the sale of securities issued by other entities, the sale of long-term assets, and the proceeds from insurance settlements related to damaged property. Examples of cash outflows from investing activities are cash payments for loans made to other entities, the purchase of the debt or equity of other entities, and the purchase of fixed assets (including capitalized interest).

Financing Activities

Financing activities are the activities resulting in alterations to the amount of contributed equity and an entity’s borrowings. These cash flows are generally associated with liabilities or equity, and involve transactions between the reporting entity and its providers of capital. Examples are cash receipts from the sale of an entity’s own equity instruments or from issuing debt, and proceeds from derivative instruments. Examples of cash outflows from financing activities are cash outlays for dividends, share repurchases, payments for debt issuance costs, and the paydown of outstanding debt.

How to Use a Cash Flow Statement

A cash flow statement can be compared to the reporting entity’s income statement to see how well reported profits compare to cash flows; there may be a substantial difference between the two. When this is the case, investigate the sources and uses of cash on the cash flow statement. It is possible that a company is reporting profits while losing cash, in which case it is likely that costs are being capitalized and deferred for recognition as expenses at a later date. While this treatment may be legitimate, it is also possible that management is engaged in fraudulent reporting.

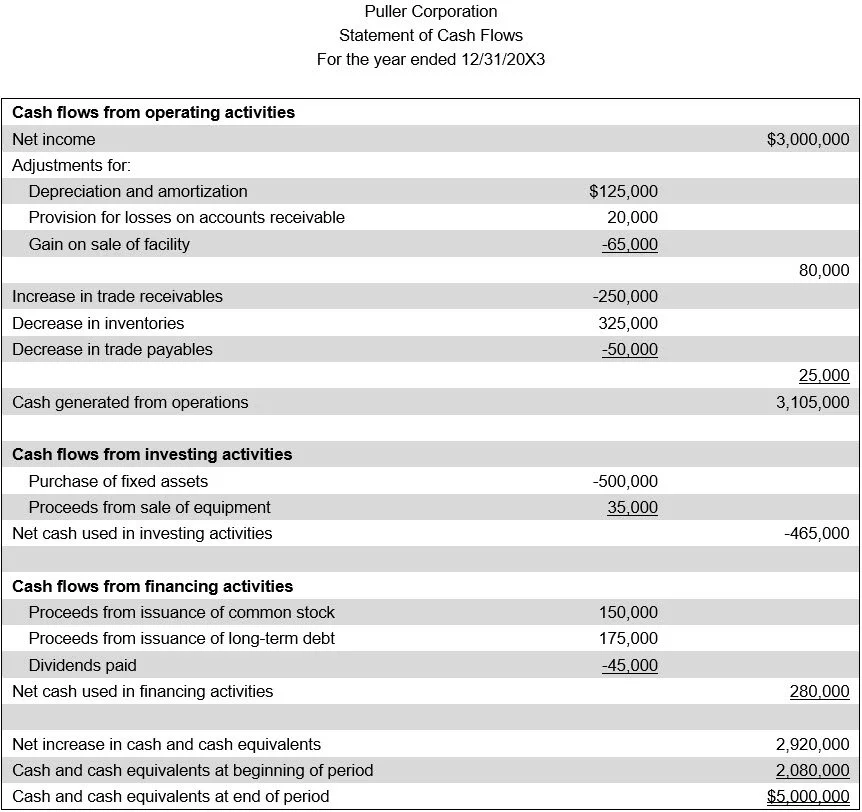

Example of a Cash Flow Statement (Indirect Method)

The format of the indirect method appears in the following example. Note that the indirect method does not include cash inflows and outflows in the cash flows from operating activities section, but rather a derivation of cash flows based on adjustments to net income.

Example of a Cash Flow Statement (Direct Method)

The format of the direct method appears in the following example, where the main differences from the indirect method appear in the Cash Flows from Operating Activities section.

Lowry Locomotion

Statement of Cash Flows

For the year ended 12/31/20X1

Cash Flow Statement FAQs

What is the difference between the direct and indirect methods?

The direct method lists specific cash inflows and outflows from operations, such as cash received from customers and cash paid to suppliers, providing a clear view of actual cash movements. The indirect method starts with net income and adjusts for non-cash items and changes in working capital to arrive at operating cash flow. While the direct method offers more transparency, the indirect method is more commonly used due to its alignment with accrual-based financial statements.

Related Articles

Cash Flow Statement - Direct Method

Cash Flow Statement - Indirect Method

Statement of Cash Flows Overview

The Difference Between Cash Flow and Funds Flow

The Difference Between Direct and Indirect Cash Flow Statements