Inventory Accounting Guide

/Introduction

Inventory accounting encompasses the methods and practices used to record and value a company’s goods on its financial statements. It determines ending inventory on the balance sheet and the cost of goods sold on the income statement. Choosing the appropriate valuation method (such as the FIFO, LIFO, or weighted average methods) affects profitability, financial analysis, and comparability across businesses.

What is Inventory Accounting?

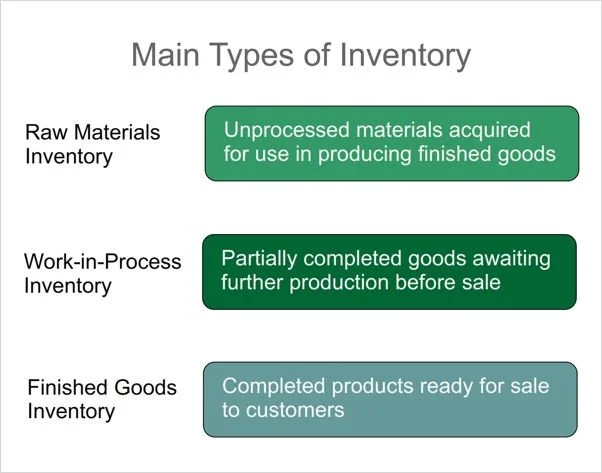

Inventory valuation plays a central role in the financial oversight of businesses that produce or trade physical products. It encompasses the policies and procedures used to measure, track, and report goods within the accounting records. Inventory refers to items intended for resale, as well as materials and partially completed units awaiting further processing. These items are generally classified into three groups: raw materials, work-in-process, and finished goods.

The objective of inventory measurement is to present an accurate carrying amount on the balance sheet and a properly calculated cost of goods sold on the income statement. By applying consistent valuation techniques, organizations ensure that reported assets, expenses, and gross margins faithfully represent operational results. Proper inventory accounting supports reliable financial reporting and informed managerial decision-making.

The Inventory Valuation Concept

Inventory valuation is the process of assigning a monetary amount to goods held for sale, including raw materials, work in process, and finished goods. It determines the cost attached to items remaining on hand at the end of a reporting period. Accurate valuation is crucial because it directly affects cost of goods sold, gross profit, taxable income, working capital, and key financial ratios. Errors can distort earnings trends, misstate assets, impair decision making, and undermine the reliability of financial statements.

The Primary Inventory Valuation Methods

There are four primary inventory valuation methods that may be used. They have varying levels of calculation complexity, as well as impacts on the financial statements and tax liabilities. They are as follows:

FIFO (First-In, First-Out). Under FIFO, the earliest acquired inventory costs are assigned to cost of goods sold first, while more recent costs remain in ending inventory. The method assumes a logical physical flow in many businesses where older goods are sold before newer ones. During periods of rising prices, FIFO typically results in lower cost of goods sold and higher reported income. Ending inventory reflects more current costs on the balance sheet.

LIFO (Last-In, First-Out). Under LIFO, the most recently acquired inventory costs are assigned to cost of goods sold first, leaving older costs in ending inventory. This approach matches current costs against current revenues during inflationary periods. As prices rise, LIFO generally produces higher cost of goods sold and lower taxable income. However, ending inventory may reflect outdated costs. The method can create cost layers that affect earnings when inventory quantities decline.

Weighted average method. The weighted average method assigns a single average cost to all units available for sale during a period. This average is calculated by dividing total cost of goods available by total units available. The resulting unit cost is applied to both cost of goods sold and ending inventory. This method smooths price fluctuations and reduces earnings volatility. It is straightforward to apply and works well when inventory items are interchangeable.

Specific identification method. The specific identification method tracks the actual cost of each individual inventory item and assigns that exact cost to cost of goods sold when the item is sold. It is most appropriate for unique, high-value, or easily distinguishable goods. Because each item is separately tracked, reported profit reflects the precise cost associated with each sale. This method requires detailed recordkeeping and strong internal controls.

The preceding methods are based on assumptions about the actual physical flow of inventory through a business that may not reflect reality. A business might choose to use a method such as LIFO in order to reduce its reported income, even if its actual inventory flow is more in accordance with the FIFO method.

Another inventory valuation method is the retail inventory method, which is actually an inventory estimation technique. It estimates ending inventory by converting retail prices to cost using a cost-to-retail ratio. Businesses accumulate the total cost and retail value of goods available for sale during the period. By dividing total cost by total retail value, they derive a percentage that represents the relationship between cost and selling price. After subtracting net sales from goods available at retail, the remaining retail amount is multiplied by the cost ratio to estimate ending inventory at cost. This method is efficient for high-volume retailers, supports interim reporting, and reduces the need for frequent physical inventory counts.

How to Account for Inventory

The accounting for inventory involves determining the correct unit counts comprising ending inventory, and then assigning a value to those units. The resulting costs are then used to record an ending inventory value, as well as to calculate the cost of goods sold for the reporting period. These basic inventory accounting activities are expanded upon below:

Determine ending unit counts. A company may use either a periodic inventory system or perpetual inventory system to maintain its inventory records. A periodic system relies upon a physical count to determine the ending inventory balance, while a perpetual system uses constant updates of the inventory records to arrive at the same goal.

Improve record accuracy. If a company uses the perpetual inventory system to arrive at ending inventory balances, the accuracy of the transactions is paramount. Accuracy levels can be improved by conducting cycle counts; these are ongoing daily counts of a small portion of the total inventory. Over time, cycle counts can dramatically improve the accuracy of inventory records.

Conduct physical counts. If a company uses the periodic inventory system to create ending inventory balances, the physical count must be conducted correctly. This involves the completion of a specific series of activities to improve the odds of counting all inventory items. A key element of these counts is to only use experienced people, such as the warehouse staff. Having the administrative staff conduct physical counts can actually reduce the accuracy of the inventory counts, since they do not have enough knowledge about the nature of the inventory.

Estimate ending inventory. There may be situations where it is not possible to conduct a physical count to arrive at the ending inventory balance. If so, the gross profit method or the retail inventory method can be used to derive an approximate ending balance. It must be emphasized that these methods yield only approximate results, and will likely need to be supplemented by an actual physical count from time to time.

Assign costs to inventory. The main role of the accountant on a monthly basis is assigning costs to ending inventory unit counts. The basic concept of cost layering, which involves tracking tranches of inventory costs, involves the first in, first out (FIFO) layering system and the last in, first out (LIFO) system. The specific identification method may also be used. We described these valuation methods earlier.

Allocate overhead to inventory. The typical production facility has a large amount of overhead costs, which must be allocated to the units produced in a reporting period. This is required by the accounting frameworks (such as GAAP and IFRS) to ensure that the full cost of unused units on hand is being recorded within the inventory balance at the end of each reporting period.

Impact of Inventory on the Financial Statements

Inventory directly affects both the profitability and financial position of a business. On the income statement, the beginning inventory, plus purchases, minus ending inventory determines the cost of goods sold. When ending inventory is higher, the cost of goods sold declines and gross profit increases. Conversely, lower ending inventory increases expense recognition and reduces reported income. Because the cost of goods sold is typically a company’s largest expense category, inventory valuation materially influences gross margin, operating income, and net income.

On the balance sheet, inventory is classified as a current asset and represents resources expected to be converted into cash within the operating cycle. Its valuation affects total current assets, working capital, and liquidity ratios. Overstated inventory inflates assets and equity, while understated inventory depresses both, directly impacting financial analysis and covenant compliance.

LIFO Conformity Rule

The LIFO conformity rule requires a company that uses the last-in, first-out method for federal income tax reporting to also use LIFO for financial reporting. This requirement, established under Internal Revenue Code Section 472, prevents entities from obtaining a tax benefit through LIFO while presenting higher income under an alternative cost flow assumption in their financial statements.

The rule directly affects both reported earnings and tax expense. In periods of rising prices, LIFO increases the cost of goods sold, reduces taxable income, and lowers income taxes payable. However, the same higher cost of goods sold reduces reported gross profit and net income, impacting earnings metrics, retained earnings, and financial ratios.

Impact of Inventory Accounting on Financial Analysis

The decisions made during inventory accounting can have a direct impact on some of the key performance metrics used to examine the performance of a business. Two especially susceptible metrics are noted below.

Days sales of inventory (DSI) measures the average number of days inventory remains on hand before sale. It is calculated by dividing average inventory by cost of goods sold and multiplying by the number of days in the period. A lower DSI indicates faster inventory movement and stronger liquidity, while a higher DSI may signal slow-moving or obsolete stock and increased carrying costs.

Inventory turnover measures how many times inventory is sold and replaced during a period. It is calculated by dividing cost of goods sold by average inventory. Higher turnover suggests efficient inventory management and strong demand, whereas lower turnover may reflect overstocking, weak sales, or operational inefficiencies.

Inventory accounting policies directly influence both metrics. Overstated inventory inflates average inventory, increasing DSI and lowering turnover. Write-downs reduce inventory balances, decreasing DSI and increasing turnover. Cost flow assumptions and overhead capitalization affect cost of goods sold, further altering ratio outcomes and potentially distorting performance analysis.

Additional Inventory Accounting Issues

The preceding points cover the essential accounting for the valuation of inventory. In addition, it may be necessary to write down the inventory values for obsolete inventory, or for spoilage or scrap, or because the market value of some goods have declined below their cost. There may also be issues with assigning costs to joint and by-product inventory items. We expand upon these additional accounting activities in the following bullet points:

Write down obsolete inventory. There must be a system in place for identifying obsolete inventory and writing down its associated cost.

Review lower of cost or market. The accounting standards mandate that the carrying amount of inventory items be written down to their market values (subject to various limitations) if those market values decline below cost.

Account for spoilage, rework, and scrap. In any manufacturing operation, there will inevitably be certain amounts of inventory spoilage, as well as items that must be scrapped or reworked. There is different accounting for normal spoilage and abnormal spoilage, the sale of spoiled goods, rework, scrap, and related topics.

Account for joint products and by-products. Some production processes have split-off points at which multiple products are created. The accountant must decide upon a standard method for assigning product costs in these situations.

Disclosures. There are a small number of disclosures about inventory that the accountant must include in the financial statements.

5 Inventory Management Techniques

Given the high impact of inventory on the reported profits and financial position of a business, it makes a great deal of sense to minimize a firm’s overall investment in inventory. Here are five techniques for doing so:

Implement just-in-time purchasing. Only purchase materials when production or sales require them. Managers coordinate closely with suppliers to ensure timely deliveries that match production schedules. This approach reduces raw material storage, lowers carrying costs, and minimizes the risk of damage or obsolescence. Reliable suppliers and accurate scheduling are essential for success.

Reduce order quantities. Place smaller, more frequent orders rather than large batch purchases. This approach keeps fewer materials or goods in storage at any one time. Lower order quantities reduce carrying costs, shrink storage requirements, and limit the financial impact of inventory damage, theft, or obsolescence during holding periods.

Standardize components and materials. Design common parts into multiple products whenever possible. Standardization reduces the variety of materials that the company must store and manage. With fewer unique components required, the business can maintain lower inventory levels, simplify its purchasing processes, and increase flexibility in production scheduling.

Improve demand forecasting. Analyze historical sales data, seasonality, and market trends to predict future demand more accurately. Accurate forecasts allow purchasing and production teams to plan inventory levels that closely match expected sales. By reducing forecasting errors, the company avoids overstocking, limits safety stock requirements, and decreases the capital tied up in inventory.

Shorten supplier lead times. Collaborate with suppliers to reduce the time required between placing an order and receiving materials. Shorter lead times allow the company to order inventory closer to the moment it is needed. This practice reduces the need for safety stock and lowers the total amount of inventory maintained.

FAQs

How do production variances affect inventory valuation?

Production variances affect inventory valuation under standard costing by adjusting recorded inventory from standard cost toward actual cost. Favorable variances may reduce inventory carrying amounts, while unfavorable variances increase them. If variances are allocated to work in process, finished goods, and cost of goods sold, inventory balances reflect corrected production costs.

How do inventory errors affect multiple accounting periods?

Inventory errors create timing distortions between periods. An overstated ending inventory understates cost of goods sold and overstates net income in the current period. In the following period, beginning inventory is overstated, which overstates cost of goods sold and understates income. Over two periods, total income remains unchanged.

Related Articles

Inventory Accounting, GAAP vs. IFRS (podcast)

The Difference Between Periodic and Perpetual Inventory Systems