Provision for income taxes definition

/What is the Provision for Income Taxes?

A provision for income taxes is the estimated amount that a business or individual taxpayer expects to pay in income taxes for the current year. The amount of this provision is derived by adjusting the firm’s reported net income with a variety of permanent differences and temporary differences. The adjusted net income figure is then multiplied by the applicable income tax rate to arrive at the provision for income taxes.

This provision can be altered to a considerable extent by the amount of tax planning that a person or business engages in to defer or eliminate the income tax liability. Consequently, the proportional size of this provision can vary significantly from taxpayer to taxpayer, based on their tax planning abilities.

Budgeting for the Provision for Income Taxes

A planned provision for income taxes can also be included in a company's budget model. In a well-crafted model, this planned provision would include both permanent and temporary differences. In a more basic model, the provision is simply based on the applicable tax rate.

Presentation of the Provision for Income Taxes

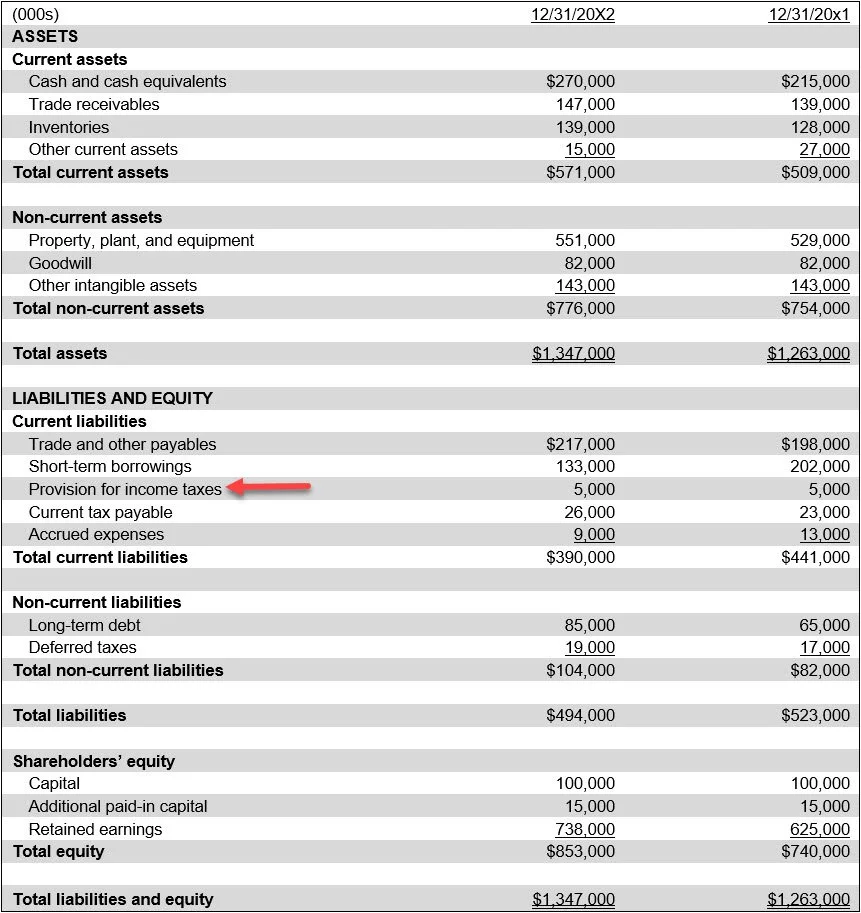

The provision for income taxes is stated within the current liabilities section of the balance sheet. A sample presentation appears in the following exhibit.

Example of a Provision for Income Taxes

Norrona Software reports a pre-tax income of $500,000 for the current year. The company’s effective tax rate is estimated to be 30% based on federal and state tax rates. To calculate the provision for income taxes, Norrona applies the tax rate to its pre-tax income, as follows:

Provision for Income Taxes = Pre-tax Income × Tax Rate

Provision for Income Taxes = $500,000 × 30% = $150,000

The associated journal entry is a debit to income tax expense for $150,000 (to reflect the tax cost on the income statement), as well as a credit to the income tax payable account for $150,000 (to recognize the liability until the tax is paid). This provision ensures that the company’s financial statements accurately reflect the tax expense for the year, matching it with the income earned. Once the actual tax payment is made to the tax authorities, the company will reduce the income tax payable account accordingly.

This example illustrates how a business estimates and records its tax obligations, ensuring that financial reports provide a realistic view of profitability after accounting for taxes.

FAQs

How does the provision for income taxes differ from taxes payable?

Taxes payable represents the amount of income taxes currently owed to taxing authorities for the reporting period. The provision for income taxes includes both current taxes payable and deferred tax expense or benefit arising from temporary differences and carryforwards. As a result, the provision reflects total tax expense under accrual accounting, while taxes payable reflects a balance sheet obligation.