Activity-Based Costing Explained

/What is Activity-Based Costing?

Activity-based costing (ABC) is a methodology for more precisely allocating overhead costs to products and services. This approach is more accurate than the traditional, less-targeted methods for allocating overhead costs. However, it is always difficult to assign overhead costs with any degree of accuracy, no matter how highly-refined the allocation methodology may be.

Activity-based costing is useful for gaining a greater understanding of which activities and cost objects within a business absorb the most (and least) overhead. With this information, a management team can engage in the targeted reduction of overhead costs. ABC works best in complex environments, where there are many machines and products, and tangled processes that are not easy to sort out. Conversely, it is of less use in a streamlined environment where production processes are abbreviated, so that costs are easy to assign.

How Does Activity-Based Costing Work?

Activity-based costing requires a complicated set of actions in order to achieve the best outcome. It is best explained by walking through the following steps.

Step 1. Identify Costs

The first step in ABC is to identify those costs that we want to allocate. This is the most critical step in the entire process, since we do not want to waste time with an excessively broad project scope. For example, if we want to determine the full cost of a distribution channel, we will identify advertising and warehousing costs related to that channel, but will ignore research costs, since they are related to products, not channels. Generally, the scope of an ABC project should be kept fairly narrow, to make the project easier to manage and more cost-effective.

Step 2. Load Secondary Cost Pools

Create cost pools for those costs incurred to provide services to other parts of the company, rather than directly supporting a company’s products or services. The contents of secondary cost pools typically include computer services and administrative salaries, and similar costs. These costs are later allocated to other cost pools that more directly relate to products and services. There may be several of these secondary cost pools, depending upon the nature of the costs and how they will be allocated. It can help to avoid a large number of cost pools, to reduce the complexity of the ABC system.

Step 3. Load Primary Cost Pools

Create a set of cost pools for those costs more closely aligned with the production of goods or services. It is very common to have separate cost pools for each product line, since costs tend to occur at this level. Such costs can include research and development, advertising, procurement, and distribution. Similarly, you might consider creating cost pools for each distribution channel, or for each facility. If production batches are of greatly varying lengths, then consider creating cost pools at the batch level, so that you can adequately assign costs based on batch size.

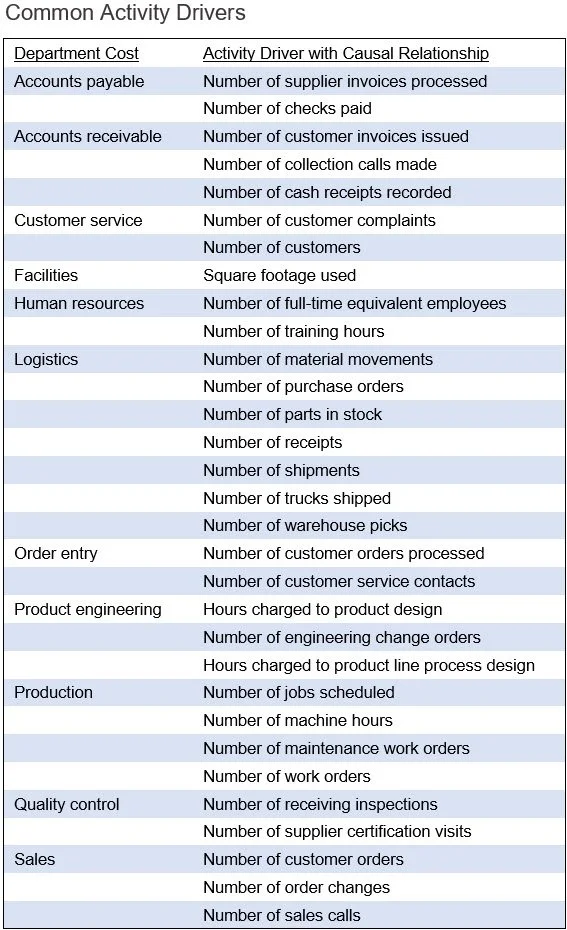

Step 4. Measure Activity Drivers

Use a data collection system to collect information about the activity drivers that are used to allocate the costs in secondary cost pools to primary cost pools, as well as to allocate the costs in primary cost pools to cost objects. It can be expensive to accumulate activity driver information, so use activity drivers for which information is already being collected, where possible. Or, if you have a choice of activity drivers, use the one for which the associated data collection cost is the lowest. The following exhibit contains a list of several of the more common activity drivers.

Step 5. Allocate Costs in Secondary Pools to Primary Pools

Use activity drivers to reassign the costs accumulated in the secondary cost pools to the primary cost pools that consume those services. For example, allocate maintenance based on machine hours, information technology based on user counts, and human resources based on employee headcount. This step transfers support department costs into operating cost pools, so the secondary pools are reduced to zero. The result is a fuller measure of the costs ultimately associated with producing goods or services.

Step 6. Charge Costs to Cost Objects

Use an activity driver to allocate the contents of each primary cost pool to cost objects. There will be a separate activity driver for each cost pool. To allocate the costs, divide the total cost in each cost pool by the total amount of activity in the activity driver, to establish the cost per unit of activity. Then allocate the cost per unit to the cost objects, based on their use of the activity driver.

Step 7. Formulate Reports

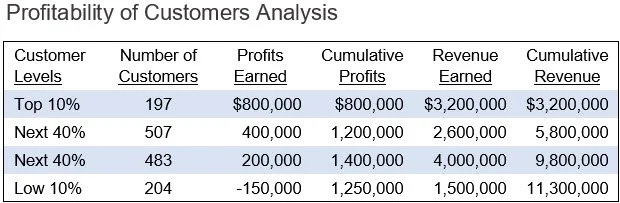

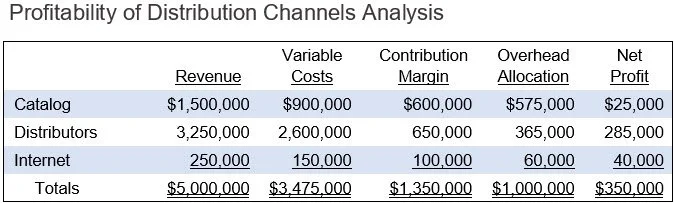

Convert the results of the ABC system into reports for management consumption. For example, if the system was originally designed to accumulate overhead information by geographical sales region, then report on revenues earned in each region, all direct costs, and the overhead derived from the ABC system. This gives management a full cost view of the results generated by each region, and therefore of the sources of the profits that the region is generating. Two ABC reports are noted in the following exhibits; the first focuses on the profitability of customers, while the second focuses on the profitability of distribution channels. Both reports include targeted allocations of overhead costs.

Step 8. Act on the Information

The most common management reaction to an ABC report is to reduce the quantity of activity drivers used by each cost object. Doing so should reduce the amount of overhead cost being used. In addition, it can be useful for the controller to monitor the actions taken by management in response to ABC reports. If management is no longer taking any action, then it may be necessary to shut down the ABC reporting system; otherwise, the company is incurring a reporting cost without benefiting from any actions to enhance operations.

We have now arrived at a complete ABC allocation of overhead costs to those cost objects that deserve to be charged with overhead costs. By doing so, managers can see which activity drivers need to be reduced in order to shrink a corresponding amount of overhead cost. For example, if the cost of a single purchase order is $100, managers can focus on letting the production system automatically place purchase orders, or on using procurement cards as a way to avoid purchase orders. Either solution results in fewer purchase orders and therefore lower purchasing department costs.

Example of Activity-Based Costing

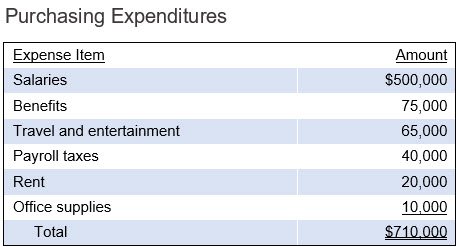

A company’s president commissions a benchmarking study of various company processes, which concludes that the company’s purchasing function is more expensive than the purchasing functions of competing companies. The president supports the creation of an ABC project to determine why the firm’s purchasing is so expensive. The project is assigned to the cost accountant, David Johnston. Mr. Johnston accesses the general ledger accounts for the purchasing department, and finds that its annual expenditures are:

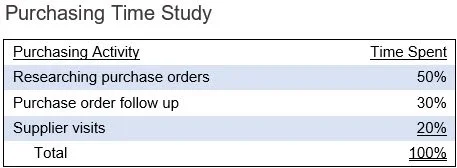

He then conducts a time study in the purchasing department to determine which activities consume the staff’s time. He compiles the following information:

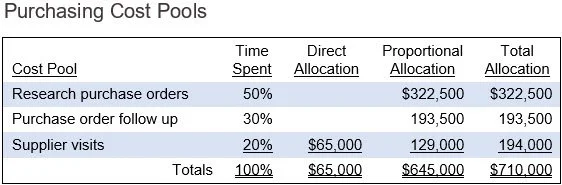

Mr. Johnston creates a separate cost pool for each of the three activities and allocates the $710,000 of expenses consumed by the department to them, using the following calculation:

The travel and entertainment portion of the department’s expenses are clearly associated with the supplier visits activity, so he shifts that entire cost to the Supplier Visits cost pool. All remaining costs are allocated among the cost pools based on the staff time spent on each one.

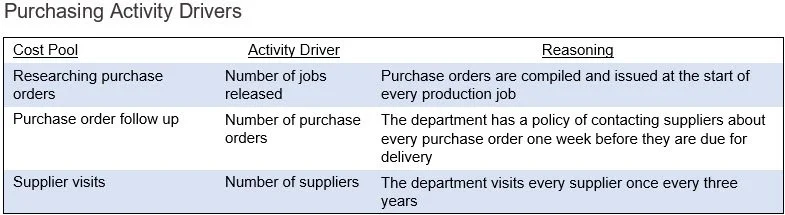

Mr. Johnston then investigates which activity drivers would be most appropriate for each cost pool. His conclusions are:

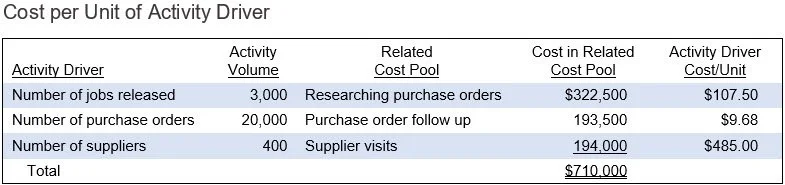

Next, Mr. Johnston compiles volume information for the activity drivers. Job information is readily available from the logistics department, purchase orders are already compiled within the purchasing department, and the supplier count is available in the accounting database. Thus, all three activity measures cost little to monitor. He then adds the activity volume to the following table to derive the cost per unit of activity driver:

At this point, there is no need to allocate the purchasing costs even further, at the product level. There are several obvious conclusions from the research project, which Mr. Johnston includes in the following memo to the president:

Researching purchase orders. Purchase orders are tied to job releases, and it is unlikely that the company will substantially alter the number of jobs.

Purchase order follow up. Follow up calls are based on a department policy to follow up on 100 percent of all purchase orders. This can be restricted to monitor only those suppliers who have a history of faulty deliveries.

Recommendation: Create a receiving procedure to create a supplier ranking system, and eliminate all suppliers who persist in faulty deliveries. The result should be the complete elimination of purchase order follow-up.

Supplier visits. There is a substantial $485 cost associated with visiting every supplier on a rotating basis. This is a policy issue, and so can be fixed with a policy change.

Recommendation: Only visit those suppliers with whom the company spends at least $100,000 per year. This will eliminate 75% of the supplier visits, and thereby reduce costs by $145,500 (300 eliminated visits × $485 per visit).

The ABC study indicates high costs at the activity driver level for all three cost pools. The key issue was how the ABC research uncovered the existence of two purchasing department policies that were significant factors in driving up the cost of the department. By altering the policies, the company was able to eliminate a large part of its purchasing expense.

Advantages of Activity-Based Costing

The fundamental advantage of using an ABC system is to more precisely determine how overhead is used. Once you have an ABC system, you can obtain better information about the issues noted below:

Learn about activity costs. ABC is designed to track the cost of activities, so you can use it to see if activity costs are in line with industry standards. If not, ABC is an excellent feedback tool for measuring the ongoing cost of specific services as management focuses on cost reduction. This analysis may even result in some activities being eliminated entirely, or outsourced.

Identify profitable customers. Though most of the costs incurred for individual customers are simply product costs, there is also an overhead component, such as unusually high customer service levels, product return handling, and cooperative marketing agreements. An ABC system can sort through these additional overhead costs and help you determine which customers are actually earning you a reasonable profit. This analysis may result in some unprofitable customers being turned away, or more emphasis being placed on those customers who are earning the company its largest profits.

Calculate cost of distribution channels. The typical company uses a variety of distribution channels to sell its products, such as retail, Internet, distributors, and mail order catalogs. Most of the structural cost of maintaining a distribution channel is overhead, so if you can make a reasonable determination of which distribution channels are using overhead, you can make decisions to alter how distribution channels are used, or even to drop unprofitable channels.

Decide when to outsource. ABC provides a comprehensive view of every cost associated with the in-house manufacture of a product, so that you can see precisely which costs will be eliminated if an item is outsourced, versus which costs will remain. This can result in extremely targeted outsourcing that is most likely to enhance profits.

Calculate product margins. With proper overhead allocation from an ABC system, you can determine the margins of various products, product lines, and entire subsidiaries. This can be quite useful for determining where to position company resources to earn the largest margins.

Set minimum price points. Product pricing is really based on the price that the market will bear, but the marketing manager should know what the cost of the product is, in order to avoid selling a product that will lose a company money on every sale. ABC is very good for determining which overhead costs should be included in this minimum cost, depending upon the circumstances under which products are being sold.

Determine facility production costs. It is usually quite easy to segregate overhead costs at the plant-wide level, so you can compare the costs of production between different facilities. This can lead to the reapportionment of production work to those facilities incurring lower overhead costs, and possibly the shut-down of unusually high-cost facilities.

Identify costs of low-volume products. Low-volume products tend to have a high proportion of overhead and other setup costs associated with them. These additional costs are not noted in a normal costing system, but are assigned to the products in an ABC system. The result is a better understanding of the increased costs of low-volume products. This can result in either increased prices for these products, their outright termination, or more attention being paid to reducing their associated overhead and other setup costs.

Clearly, there are many valuable uses for the information provided by an ABC system. However, this information will only be available if you design the system to provide the specific set of data needed for each decision. If you install a generic ABC system and then use it for the above decisions, you may find that it does not provide the information that you need. Ultimately, the design of the system is determined by a cost-benefit analysis of which decisions you want it to assist with, and whether the cost of the system is worth the benefit of the resulting information.

Disadvantages of Activity Based Costing

Many companies initiate ABC projects with the best of intentions, only to see a very high proportion of the projects either fail or eventually lapse into disuse. There are several reasons for these issues, which are noted below:

Too many cost pools. The advantage of an ABC system is the high quality of information that it produces, but this comes at the cost of using a large number of cost pools – and the more cost pools there are, the greater the cost of managing the system. To reduce this cost, run an ongoing analysis of the cost to maintain each cost pool, in comparison to the utility of the resulting information. Doing so should keep the number of cost pools down to manageable proportions.

Difficult to install. ABC systems are notoriously difficult to install, with multi-year installations being the norm when a company attempts to install it across all product lines and facilities. For such comprehensive installations, it is difficult to maintain a high level of management and budgetary support as the months roll by without installation being completed. Success rates are much higher for smaller, more targeted ABC installations.

Requires data from many sources. An ABC system may require data input from multiple departments, and each of those departments may have greater priorities than the ABC system. Thus, the larger the number of departments involved in the system, the greater the risk that data inputs will fail over time. This problem can be avoided by designing the system to only need information from the most supportive managers.

Information only collected once. Many ABC projects are authorized on a project basis, so that information is only collected once; the information is useful for a company’s current operational situation, and it gradually declines in usefulness as the operational structure changes over time. Management may not authorize funding for additional ABC projects later on, so ABC tends to be “done” once and then discarded. To mitigate this issue, build as much of the ABC data collection structure into the existing accounting system, so that the cost of these projects is reduced; at a lower cost, it is more likely that additional ABC projects will be authorized in the future.

Avoidance of slack time reporting. When a company asks its employees to report on the time spent on various activities, they have a strong tendency to make sure that the reported amounts equal 100% of their time. However, there is a large amount of slack time in anyone’s work day that may involve breaks, administrative meetings, playing games on the Internet, and so forth. Employees usually mask these activities by apportioning more time to other activities. These inflated numbers represent misallocations of costs in the ABC system, sometimes by quite substantial amounts.

Requires additional data. An ABC system rarely can be constructed to pull all of the information it needs directly from the general ledger. Instead, it requires a separate database that pulls in information from several sources, only one of which is existing general ledger accounts. It can be quite difficult to maintain this extra database, since it calls for significant extra staff time for which there may not be an adequate budget. The best work-around is to design the system to require the minimum amount of additional information other than that which is already available in the general ledger.

Only needed in a complex environment. The benefits of ABC are most apparent when cost accounting information is difficult to discern, due to the presence of multiple product lines, machines being used for the production of many products, numerous machine setups, and so forth – in other words, in complex production environments. If a company does not operate in such an environment, then it may spend a great deal of money on an ABC installation, only to find that the resulting information is not overly valuable.

The broad range of issues noted here should make it clear that ABC tends to follow a bumpy path in many organizations, with a tendency for its usefulness to decline over time. Of the problem mitigation suggestions noted here, the key point is to construct a highly targeted ABC system that produces the most critical information at a reasonable cost. If that system takes root in your company, then consider a gradual expansion, during which you only expand further if there is a clear and demonstrable benefit in doing so. The worst thing you can do is to install a large and comprehensive ABC system, since it is expensive, meets with the most resistance, and is the most likely to fail over the long term.

Activity-Based Costing FAQs

What types of businesses benefit from activity-based costing?

Businesses with diverse products, multiple processes, or significant overhead benefit most from activity-based costing. Examples include manufacturers with varied product lines, hospitals, logistics companies, and service firms with complex client work. ABC is most useful when traditional costing spreads overhead too broadly and obscures the true cost of activities.

How does activity-based costing support process improvement?

Activity-based costing supports process improvement by showing which activities consume the most resources and which add little value. It helps managers identify waste, rework, excess handling, and inefficient procedures. This insight supports redesign efforts, better resource allocation, cost reduction, and more efficient operations across the organization.