Fixed asset definition

/What is a Fixed Asset?

A fixed asset is a long-term tangible asset that a business uses in its operations rather than holding for resale. It provides economic benefits over more than one accounting period. Fixed assets include items such as property, plant, and equipment. They are recorded at cost and systematically depreciated over their useful lives. Fixed assets support the ongoing production or administrative activities of an organization.

Characteristics of a Fixed Asset

The key characteristics of a fixed asset are as follows:

Long-term use. Fixed assets are intended for long-term use in business operations, typically for more than one year. They are not acquired for resale but to support the production of goods or services. Examples include buildings, machinery, vehicles, and equipment.

Tangible nature. Most fixed assets are tangible, meaning they have a physical presence that can be seen and touched. This distinguishes them from intangible assets like patents or trademarks. Their tangible nature allows for easier valuation and tracking.

High initial cost. Fixed assets usually involve a significant initial investment compared to current assets like inventory or accounts receivable. Their acquisition often requires careful planning, budgeting, and long-term financing. The substantial cost emphasizes the need for effective management and maintenance of these assets.

Requires depreciation. Fixed assets, except for land, are subject to depreciation, which allocates their cost over their useful life. Depreciation reflects wear and tear, obsolescence, or the passage of time and is recorded as an expense on the income statement. This systematic allocation helps in matching costs with revenues generated from the asset.

Used in operations. Fixed assets are directly used in the day-to-day operations of a business to generate revenue. For example, manufacturing equipment is used to produce goods, while office buildings provide space for employees to work. Their role in operations is essential to achieving business objectives.

Non-liquid nature. Fixed assets are considered non-liquid because they cannot be quickly converted into cash without significant loss of value. Selling fixed assets often requires time, negotiation, and sometimes a reduction in price, making them less useful for meeting short-term financial obligations.

Recorded at historical cost. Fixed assets are recorded on the balance sheet at their historical cost, which includes the purchase price and any costs necessary to prepare them for use, such as installation or shipping fees. This cost basis remains unchanged, with adjustments only for depreciation or impairment.

These characteristics highlight the strategic importance of fixed assets in supporting business operations and ensuring long-term profitability.

Examples of Fixed Assets

There are many types of fixed assets, including buildings, computer equipment, computer software, furniture and fixtures, intangible assets, land, leasehold improvements, machinery, and vehicles.

Accounting for Fixed Assets

Fixed assets are initially recorded as assets, and are then subject to the following general types of accounting transactions:

Periodic depreciation (for tangible assets) or amortization (for intangible assets)

Impairment write-downs (if the value of an asset declines below its net book value)

Disposition (once assets are disposed of)

Presentation of Fixed Assets

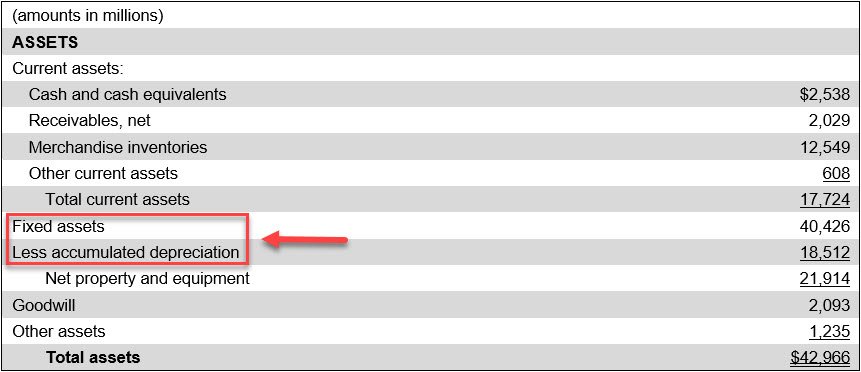

Fixed assets appear on the balance sheet, where they are classified after current assets, as long-term assets. This line item is paired with the accumulated depreciation line item, resulting in a net fixed assets figure. A sample presentation of the assets section of a balance sheet appears in the following exhibit, with the positioning of the fixed assets and accumulated depreciation line items highlighted.

FAQs

Is Inventory a Fixed Asset?

No, inventory is not a fixed asset. Inventory is classified as a current asset because it is held for sale or use in production and is expected to be converted into cash within the operating cycle. Fixed assets, by contrast, are long-term tangible assets used in operations rather than held for resale.

Terms Similar to Fixed Asset

A fixed asset is also known as Property, Plant, and Equipment.

Related Articles

Fixed Asset Disposal Accounting

Fixed Asset Impairment Accounting