Sales budget | Sales budget example

/What is a Sales Budget?

Any business needs some structure to its sales planning, which calls for a sales budget. A sales budget is focused on selling specific unit quantities at targeted price points; this information can be used to estimate the expenditures needed to achieve these goals. With a budget in hand, you can plan for sales expenditures and compensation changes - all with the goal of maximizing your revenue over the planning period.

What is Included in a Sales Budget?

The sales budget contains an itemization of a company's sales expectations for the budget period, in both units and dollars. If a company has a large number of products, it usually aggregates its expected sales into a smaller number of product categories or geographic regions; otherwise, it becomes too difficult to generate sales estimates for this budget.

The projected unit sales information in the sales budget feeds directly into the production budget, from which the direct materials and direct labor budgets are created. The sales budget is also used to give managers a general sense of the scale of operations, for when they create the overhead budget and the selling and administrative expenses budget. The total net sales dollars listed in the sales budget are carried forward into the sales line item in the master budget.

It is extremely important to do the best possible job of forecasting, since the information in the sales budget is used by most of the other budgets. Thus, if the sales budget is inaccurate, then so too will be the other budgets that use it as source material.

Presentation of the Sales Budget

The sales budget is usually presented in either a monthly or quarterly format; presenting only annual sales information is too aggregated, and so provides little actionable information.

Sources of the Sales Budget

The information in the sales budget comes from a variety of sources. Most of the detail for existing products comes from those personnel who deal with them on a day-to-day basis. The marketing manager contributes sales promotion information, which can alter the timing and amount of sales. The engineering and marketing managers may also contribute information about the introduction date of new products, as well as the retirement dates of old products. The chief executive officer may revise these figures for the sales of any subsidiaries or product lines that the company plans to terminate or sell during the budget period.

It is generally best not to include in the sales budget any estimates for sales related to prospective acquisitions of other companies, since the timing and amounts of these sales are too difficult to estimate. Instead, revise the sales budget after an acquisition has been finalized.

Structure of the Sales Budget

The basic calculation in the sales budget is to itemize the number of unit sales expected in one row, and then list the average expected unit price in the next row, with the total sales appearing in a third row. The unit price may be adjusted for marketing promotions. If any sales discounts or sales returns are anticipated, these items are also listed in the sales budget.

Revisions to the Sales Budget

It is quite difficult to derive a sales forecast that proves to be accurate for any period of time, so an alternative is to periodically adjust the sales budget with revised estimates, perhaps on a quarterly basis. If this is done, the rest of the budget that is derived from the sales figures will also have to be revised, which can require a significant amount of staff time.

Example of a Sales Budget

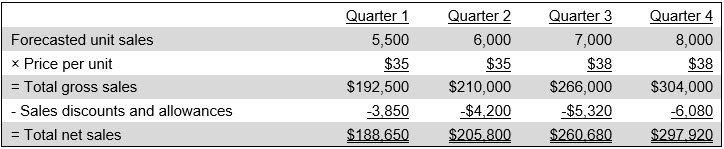

Quest Adventure Gear is a maker of rugged travel gear. One of its equipment lines is a propane-powered camp stove. Its sales forecast is as follows:

Quest’s sales manager expects that increased demand in the second half of the year will allow it to increase its wholesale unit price from $35 to $38. Also, the sales manager expects that the company’s historical sales discounts and allowances percentage of two percent of gross sales will continue through the budget period.

This example of the sales budget is simplistic, since it assumes that the company only sells in one product category. In reality, this example might have been a detail page that rolls up into the main sales budget, where it would occupy a single line item.

Sales Budget Best Practices

Several best practices can be used to improve a sales budget. One is to ensure that you have budgeted for sufficient resources to support your sales goal. So, if you plan to double sales, you might want to double the number of sales staff, too. Another best practice is to focus on the training ramp-up required before each salesperson will be able to sell at full efficiency. Depending on the products being sold, this can take some time, so plan accordingly. Third, focus on the timing of the sales events that will generate the bulk of your revenue. Are you adequately staffed and funded for each one, and are your sales estimates reasonable for each one? If not, you may need to scale back on your expectations. And finally, be aware of the location of your bottleneck in the sales process. For example, if you need a presentation by a sales engineer to close each sale and you only have one sales engineer, then your sales will be capped at the productivity of that one person - unless you plan to add more sales engineers. These best practices are essential for the development of an achievable, realistic sales budget.

Sales Budget FAQs

What tools are used to develop a sales budget?

Tools used to develop a sales budget include spreadsheets like Microsoft Excel, which allow for custom formulas and detailed forecasting. Many organizations also use enterprise resource planning (ERP) systems or budgeting software such as QuickBooks, SAP, or Oracle for more integrated planning. These tools often incorporate historical data, trend analysis, and scenario modeling to improve accuracy.

How should customer concentration risk be addressed in a sales budget?

Customer concentration risk should be addressed by identifying major customers separately in the sales budget, rather than burying them in aggregate revenue. Management should assess contract status, renewal risk, pricing pressure, order timing, and replacement sales if a key customer reduces purchases. Scenario analysis can show the impact of losing significant accounts.

Related Articles

Advantages of a Good Business Plan

The Difference Between a Budget and a Forecast