Overview of Capital Budgeting

/What is Capital Budgeting?

Capital budgeting is the process of analyzing and ranking proposed projects to determine which ones are deserving of an investment. This process is needed to ensure that funds are targeted at the most critical investments for a business, such as those that will generate the greatest positive cash flow, comply with government regulations, or enact the firm’s strategic plan. This process is especially important when an organization has less available cash than is needed for all possible capital investments.

Types of Capital Budgeting Methods

There are three general methods for deciding which proposed projects should be ranked higher than other projects, which (in declining order of preference) are as follows:

Throughput analysis. Determines the impact of an investment on the throughput of an entire system.

Discounted cash flow analysis. Uses a discount rate to determine the present value of all cash flows related to a proposed project. Tends to create improvements on a localized basis, rather than for the entire system, and is subject to incorrect results if cash flow forecasts are incorrect.

Payback analysis. Calculates how fast you can earn back your investment; is more of a measure of risk reduction than of return on investment.

These capital budgeting decision points are outlined in the following sections.

Related AccountingTools Courses

Throughput Analysis

Under throughput analysis, the key concept is that an entire company acts as a single system, which generates a profit. Under this concept, capital budgeting revolves around the following logic:

Nearly all of the costs of the production system do not vary with individual sales; that is, nearly every cost is an operating expense; therefore,

You need to maximize the throughput of the entire system in order to pay for the operating expense; and

The only way to increase throughput is to maximize the throughput passing through the bottleneck operation.

Consequently, you should give primary consideration to those capital budgeting proposals that favorably impact the throughput passing through the bottleneck operation.

This does not mean that all other capital budgeting proposals will be rejected, since there are a multitude of possible investments that can reduce costs elsewhere in a company, and which are therefore worthy of consideration. However, throughput is more important than cost reduction, since throughput has no theoretical upper limit, whereas costs can only be reduced to zero. Given the greater ultimate impact on profits of throughput over cost reduction, any non-bottleneck proposal is simply not as important.

Discounted Cash Flow Analysis

Any capital investment involves an initial cash outflow to pay for it, followed by a mix of cash inflows in the form of revenue, or a decline in existing cash flows that are caused by expenses incurred. We can lay out this information in a spreadsheet to show all expected cash flows over the useful life of an investment, and then apply a discount rate that reduces the cash flows to what they would be worth at the present date. This calculation is known as net present value. Net present value is the traditional approach to evaluating capital proposals, since it is based on a single factor – cash flows – that can be used to judge any proposal arriving from anywhere in a company.

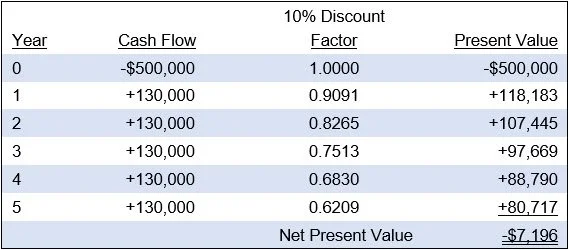

For example, ABC Company is planning to acquire an asset that it expects will yield positive cash flows for the next five years. Its cost of capital is 10%, which it uses as the discount rate to construct the net present value of the project. The following table shows the calculation:

The net present value of the proposed project is negative at the 10% discount rate, so ABC should not invest in the project.

In the “10% Discount Factor” column, the factor becomes smaller for periods further in the future, because the discounted value of cash flows are reduced as they progress further from the present day. The discount factor can be derived from the following formula:

Payback Analysis

The simplest and least accurate evaluation technique is the payback method. This approach is still heavily used, because it provides a very fast calculation of how soon a company will earn back its investment. This means that it provides a rough measure of how long a business will have its investment at risk, before earning back the original amount expended. Thus, it is a rough measure of risk. There are two ways to calculate the payback period, which are noted below.

Simplified Payback Analysis

Divide the total amount of an investment by the average resulting cash flow. This approach can yield an incorrect assessment, because a proposal with cash flows skewed far into the future can yield a payback period that differs substantially from when actual payback occurs.

Manual Payback Analysis

Manually deduct the forecasted positive cash flows from the initial investment amount, from Year 1 forward, until the investment is paid back. This method is slower to calculate, but ensures a higher degree of accuracy.

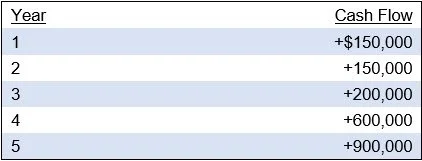

For example, ABC Company has received a proposal from a manager, asking to spend $1,500,000 on equipment that will result in cash inflows in accordance with the following table:

The total cash flows over the five-year period are projected to be $2,000,000, which is an average of $400,000 per year. When divided into the $1,500,000 original investment, this results in a payback period of 3.75 years. However, the briefest perusal of the projected cash flows reveals that the flows are heavily weighted toward the far end of the time period, so the results of this calculation cannot be correct.

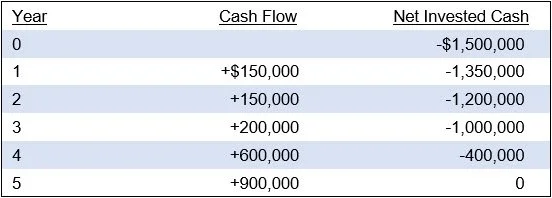

Instead, the cost accountant runs the calculation year by year, deducting the cash flows in each successive year from the remaining investment. The results of this calculation are:

The table indicates that the real payback period is located somewhere between Year 4 and Year 5. There is $400,000 of investment yet to be paid back at the end of Year 4, and there is $900,000 of cash flow projected for Year 5. The cost accountant assumes the same monthly amount of cash flow in Year 5, which means that he can estimate final payback as being just short of 4.5 years.

The payback method is not overly accurate, does not provide any estimate of how profitable a project may be, and does not take account of the time value of money. Nonetheless, its extreme simplicity makes it a perennial favorite in many companies.

Related Articles

Capacity Planning in the Budget