Material budgeting | Direct materials budget

/What is the Direct Materials Budget?

The direct materials budget calculates the materials that must be purchased, by time period, in order to fulfill the requirements of the production budget. It is typically presented in either a monthly or quarterly format in the annual budget. In a business that sells products, this budget may contain a majority of all costs incurred by the company, and so should be compiled with considerable care. Otherwise, the result may erroneously indicate excessively high or low cash requirements to fund materials purchases.

How to Calculate the Direct Materials Budget

The basic calculation used by the direct materials budget is as follows:

+ Raw materials required for production

+ Planned ending inventory balance

= Total raw materials required

- Beginning raw materials inventory

= Raw materials to be purchased

It is impossible to calculate the direct materials budget for every component in inventory, since the calculation would be massive. Instead, it is customary to either calculate the approximate amount of inventory required, expressed as a grand total for the entire inventory, or else at a somewhat more detailed level by commodity type. It is possible to create a reasonably accurate direct materials budget by either means, if you have a material requirements planning software package that has a planning module. By entering the production budget into the planning module, the software can generate the expected direct materials budget for future periods. Otherwise, you will have to calculate the budget manually.

A lesser alternative is to calculate the direct materials budget based on the historical percentage of direct materials experienced in recent reporting periods; doing so assumes that the same ratio of direct material costs to revenues will continue, which can be a dangerous assumption. Realistically, the mix of products sold will change over time, so the historical percentage of direct materials to revenues may not match actual results in future periods.

Example of the Direct Materials Budget

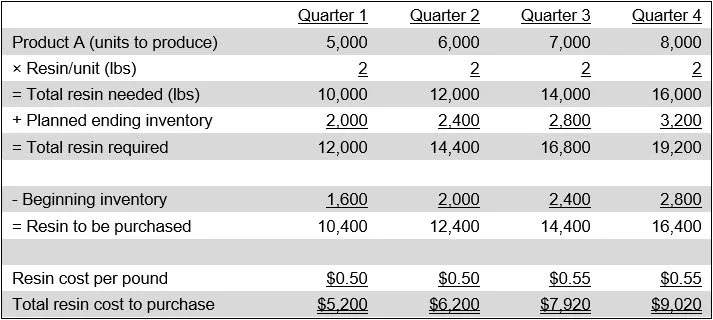

ABC Company plans to produce a variety of plastic goods, and 98 percent of its raw materials involve plastic resin. Thus, there is only one key commodity to be concerned with. Its production needs are outlined as follows:

ABC Company

Direct Materials Budget

For the Year Ended December 31, 20XX

The inventory at the end of each quarter is planned to be 20 percent of the amount of resin used during that month, so the ending inventory varies over time, gradually increasing as production requirements increase. The reason for the planned increase is that ABC has some difficulty receiving resin in a timely manner from its supplier, so it maintains a safety stock of inventory on hand.

The purchasing department expects that global demand will drive up the price of resin, so it incorporates a slight price increase into the third quarter, which carries forward into the fourth quarter.

Best Practices for the Direct Materials Budget

The preparation of the direct materials budget can be so detailed that the preparer becomes lost in the details and does not determine whether the entire result is reasonable. Accordingly, be sure to review the completed budget based on historical percentages, and consult with the purchasing staff to see if cost assumptions are reasonable.

If product life cycles are quite short and margins vary substantially by product, this budget may become highly inaccurate if the forecast period is for a full year. In this case, it may make more sense to budget over a shorter period.

It is not customary to include a cash requirements calculation as part of the direct materials budget. Instead, the cash requirements are calculated for all of the revenues and expenditures of a business as a whole, and are then summarized on a separate page of the budget.

Direct Materials Budget FAQs

How does the direct materials budget relate to the master budget?

The direct materials budget is a supporting component of the master budget. It estimates the quantity and cost of raw materials needed for planned production, based on the production budget. Its output feeds into the cash budget, budgeted income statement, and budgeted balance sheet by projecting material purchases and related costs.

How do standard costs influence the direct materials budget?

Standard costs influence the direct materials budget by providing expected unit prices and usage rates for materials. They simplify budget preparation, support consistency in planning, and create benchmarks for variance analysis. However, if standard costs are outdated or unrealistic, the budget may misstate expected purchases and material cost levels.