Master budget definition

/What is a Master Budget?

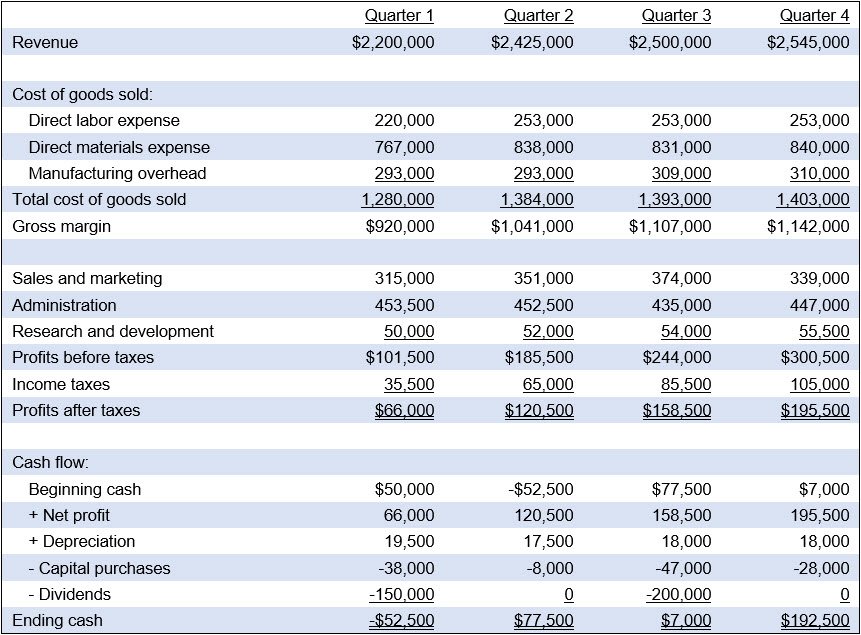

The master budget is the aggregation of all lower-level budgets produced by a company's various functional areas, and also includes budgeted financial statements, a cash forecast, and a financing plan. The master budget is typically presented in either a monthly or quarterly format, and usually covers a company's entire fiscal year. An explanatory text may be included with the master budget, which explains the company's strategic direction, how the master budget will assist in accomplishing specific goals, and the management actions needed to achieve the budget. There may also be a discussion of the headcount changes that are required to achieve the budget. A sample master budget appears in the following exhibit.

A master budget is the central planning tool that a management team uses to direct the activities of a corporation, as well as to judge the performance of its various responsibility centers. It is customary for the senior management team to review a number of iterations of the master budget and incorporate modifications until it arrives at a budget that allocates funds to achieve the desired results. Hopefully, a company uses participative budgeting to arrive at this final budget, but it may also be imposed on the organization by senior management, with little input from other employees.

The budgets that roll up into the master budget include:

Direct labor budget. This contains a calculation of the direct labor costs to be incurred during the budget period, based on estimates of which products will be manufactured and what labor rates will be paid.

Direct materials budget. This contains a calculation of the direct material costs to be incurred during the budget period. This can be a very refined calculation or (more likely) is based on the historical cost of direct materials as a percentage of net sales.

Ending finished goods budget. This contain an estimate of the value of the finished goods inventory, which is derived from estimates of product demand and the number of units that will be produced during the budget period.

Manufacturing overhead budget. This contains an estimate of manufacturing overhead costs during the budget period. Many of these costs are fixed, and so are derived from historical cost information.

Production budget. This contains an estimate of the number of units of the various company products that will be manufactured during the budget period, and is capped at the firm’s production capacity.

Sales budget. This contains an estimate of which products will be sold during the budget period, and in what quantities, as well as the prices at which they will be sold.

Selling and administrative expense budget. This contains the cost of the selling and other administration departments for the budget period, including estimates of salary and bonus payments, rent, utilities, and other ancillary expenditures.

The selling and administrative expense budget may be further subdivided into budgets for individual departments, such as the accounting, engineering, facilities, and marketing departments.

Once the master budget has been finalized, the accounting staff may enter it into the company's accounting software, so that the software can issue financial reports comparing budgeted and actual results.

Smaller organizations usually construct their master budgets using electronic spreadsheets. However, spreadsheets may contain formula errors, and also have a difficult time constructing a budgeted balance sheet. Larger organizations use budget-specific software, which does not have these two problems.

Example of a Master Budget

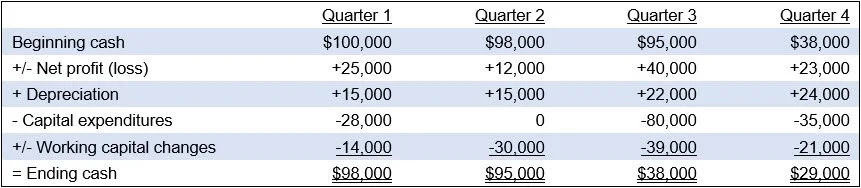

Many lower-level budgets have specific formats that are used to arrive at certain outcomes, such as the fully absorbed cost of the finished goods inventory, or the number of units of products to be manufactured. This is not the case for the master budget, which looks very much like a standard set of financial statements. The income statement and balance sheet will be in the normal format mandated by Generally Accepted Accounting Principles or International Financial Reporting Standards. The primary difference is the cash budget, which does not usually appear in the standard format of the statement of cash flows. Instead, it serves the more practical purpose of identifying specific cash inflows and outflows that will result from the rest of the budget model. Here is an example of the cash budget:

Alpha Intergalactic Corporation

Cash Budget

For the Year Ended December 31, 20XX

The most difficult item to estimate in the cash budget is the net change in working capital from period to period. During periods of rapid growth, working capital can be a strongly negative number, since the company must invest in more accounts receivable than usual. If the amount of working capital appears to be holding steady despite rapid growth, then it is quite likely that management has built an unrealistic expectation into the budget to be able to collect accounts receivable more quickly than has been the case in the past.

A similar problem can arise with inventory, which is another component of working capital. It generally takes more inventory to support more sales, so the portion of working capital comprised of inventory can be expected to increase in conjunction with more sales. Thus, it is extremely likely that a company experiencing any amount of growth will forecast negative cash flows, because of the need to fund additional working capital.

Other Master Budget Issues

Another document sometimes included in the master budget is a set of key performance metrics that are calculated based on the information in the budget. For example, it may show accounts receivable turnover, or inventory turnover, or earnings per share. These metrics are useful for testing the validity of the budget model against actual results in the past. For example, if the accounts receivable turnover metric is much lower than historical results, that could mean that the company is over-estimating its ability to collect accounts receivable promptly, which means that the amount of accounts receivable shown in the balance sheet may be understated and the amount of cash may be overstated.

Problems with the Master Budget

When a company implements a master budget, there is a strong tendency for senior management to force the organization to closely adhere to it by including budget goals in employee compensation plans. Doing so has the following effects:

When compiling the budget, employees tend to estimate low sales and high expenses, so that they can easily meet the budget and achieve their compensation plans.

Forcing the organization to follow the budget requires a group of financial analysts who track down and report on variances from the plan. This adds unnecessary overhead expense to the business.

Managers tend to ignore new business opportunities, because all resources are already allocated toward attaining the budget, and their personal incentives are tied to the budget.

Thus, enforcing a master budget can skew the operational performance of a business. Because of this problem, it may be better to employ the master budget as just a rough guideline for management's near-term expectations for the business.

Master Budget FAQs

How is the master budget used for performance evaluation?

The master budget is used for performance evaluation by comparing actual financial results to budgeted targets. Variances between planned and actual figures help management identify areas of efficiency or underperformance. This analysis supports accountability, motivates managers, and guides corrective actions to improve future operations.

Related Articles

The Difference Between a Budget and a Forecast